Yahoo Finance

Yahoo Finance Here's Why You Should Retain Elevance (ELV) in Your Portfolio

Elevance Health, Inc’s ELV growing premiums, higher consumers served, the pursuit of buyouts, numerous contract wins and continued payment innovation make it worth retaining in one’s portfolio. Also, its favorable growth estimates are confidence boosters for investors.

The company is one of the largest health insurers in the United States in terms of medical membership, catering to 47.5 million medical members as of 2022-end. ELV is positioned to provide innovative and affordable products to customers.

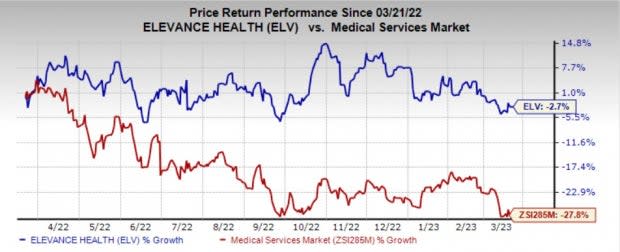

Zacks Rank & Price Performance

ELV currently carries a Zacks Rank #3 (Hold). In the past year, the stock has shed less value than its industry. While ELV shares have declined 2.7% the industry fell 27.8% during this period.

Image Source: Zacks Investment Research

Optimistic Growth Projections

The Zacks Consensus Estimate for ELV’s 2023 earnings is pegged at $32.73 per share, indicating a 12.6% increase from the year-ago reported figure of $29.07. The same for ELV’s 2023 sales is pegged at $164.8 billion, indicating a 5.9% increase from the year-ago reported figure of $155.7 billion.

Growth Drivers

Elevance’s strong local presence will help it meet local demand for any type of product the customers are enrolled in. Its local presence and national expertise have resulted in collaborative programs, rewarding hospitals and physicians for providing quality services. This sheds light on its focus on bringing about improvement in the quality of healthcare.

ELV develops its products, placing special emphasis on the different needs of customers. It seeks to price its products and establish designs to provide utility and value to its customers while achieving profitability and growing market share. This will support growth in the long term.

Elevance’s numerous acquisitions have helped the company boost its inorganic growth. It acquired Blue Cross and Blue Shield early this year, which aligns with its mission and purpose of improving the health and lives of people. While the acquired will provide their local roots in a new market, ELV will contribute its national scale and access to its portfolio of innovative solutions, positively impacting the lives of 1.9 million individuals.

ELV’s exclusive right under Blue Cross and Blue Shield association of companies, the most recognized brand in the industry, to market its product results in greater brand recognition and value than its counterparts. As the managed care industry remains highly competitive, ELV’s customer retention acts as a moat and differentiates it from competitors.

ELV’s improving business segment, CarelonRx, will further benefit from its acquisition of BioPlus, which closed this February. Adding BioPlus is expected to enhance ELV’s ability to deliver on its whole health mission and expand Carelon’s scope of services. It will further help in scaling healthcare services.

Elevance’s pricing strategy based on proprietary research, predictive modeling and other data-driven processes has positioned it well to benefit from opportunities such as entering new markets and expanding in existing markets. In addition, good relationships with qualified agents and brokers, quality service, better products, and commission structure compare favorably with their competitors.

ELV’s consistent dividend payouts and stock repurchases boost shareholders' value. It had a leftover capacity to repurchase shares worth $1.9 billion as of Dec 31, 2022. Its dividend yield of 1.3% remains higher than the industry’s 0.9% average. It also increased quarterly dividends by 16%, marking the 12th consecutive annual increase, making it an attractive potential investment for yield-seeking investors.

Key Concerns

There are a few factors that are impeding the stock’s growth lately.

ELV’s total expenses rose 13.9% in 2022 mainly due to higher benefit expenses and the cost of products sold. Rising costs can affect its margins.

The company’s growing debt level requires attention. Long-term debt, less current portion, was $22,349 million at 2022-end, up 5.6% from the 2021-end level, while cash and cash equivalents amounted to only $7,387 million. Nevertheless, we believe that a systematic and strategic plan of action will drive growth in the long term.

Stocks to Consider

Some better-ranked stocks from the broader medical space are ICON ICLR, AlconALC and Embecta Corp. EMBC. ICON sports a Zacks Rank #1 (Strong Buy), and Alcon and Embecta Corp carry a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for ICON 2023 earnings indicates 7.4% year-over-year growth. The Zacks Consensus Estimate for ICLR’s 2023 earnings has moved 0.6% north in the past 30 days.

The Zacks Consensus Estimate for Alcon 2023 earnings indicates 15.2% year-over-year growth. The Zacks Consensus Estimate for ALC’s 2023 earnings has moved 0.8% north in the past 7 days.

The Zacks Consensus Estimate for Embecta Corp's 2024 earnings indicates 10.1% year-over-year growth.The Zacks Consensus Estimate for EMBC’s 2023 earnings has moved 8.4% north in the past 30 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Alcon (ALC) : Free Stock Analysis Report

ICON PLC (ICLR) : Free Stock Analysis Report

Embecta Corp. (EMBC) : Free Stock Analysis Report

Elevance Health, Inc. (ELV) : Free Stock Analysis Report