Yahoo Finance

Yahoo Finance Here's Why Lithium Chile (CVE:LITH) Must Use Its Cash Wisely

Just because a business does not make any money, does not mean that the stock will go down. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So, the natural question for Lithium Chile (CVE:LITH) shareholders is whether they should be concerned by its rate of cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. Let's start with an examination of the business's cash, relative to its cash burn.

View our latest analysis for Lithium Chile

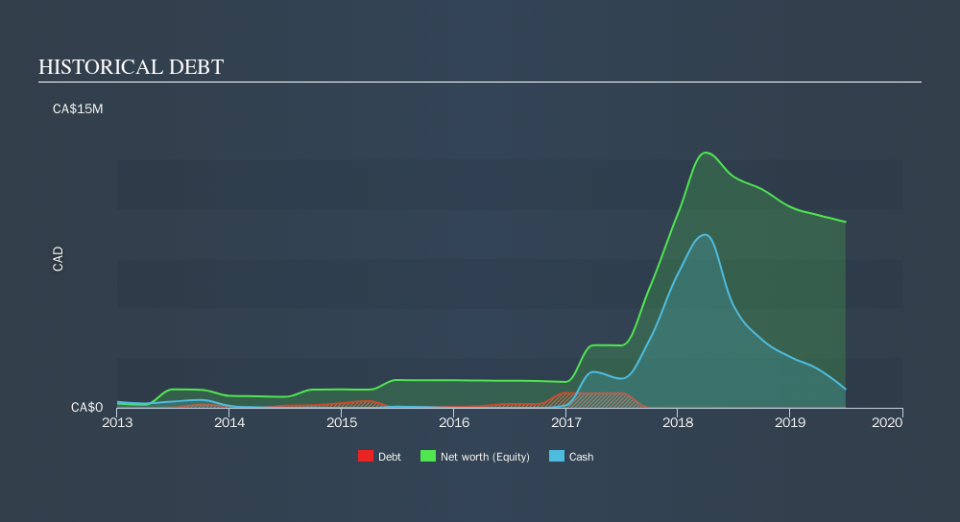

Does Lithium Chile Have A Long Cash Runway?

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. When Lithium Chile last reported its balance sheet in June 2019, it had zero debt and cash worth CA$939k. In the last year, its cash burn was CA$3.9m. So it had a cash runway of approximately 3 months from June 2019. That's a very short cash runway which indicates an imminent need to douse the cash burn or find more funding. The image below shows how its cash balance has been changing over the last few years.

How Is Lithium Chile's Cash Burn Changing Over Time?

Lithium Chile didn't record any revenue over the last year, indicating that it's an early stage company still developing its business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. Given the length of the cash runway, we'd interpret the 24% reduction in cash burn, in twelve months, as prudent if not necessary for capital preservation. Lithium Chile makes us a little nervous due to its lack of substantial operating revenue. We prefer most of the stocks on this list of stocks that analysts expect to grow.

Can Lithium Chile Raise More Cash Easily?

While Lithium Chile is showing a solid reduction in its cash burn, it's still worth considering how easily it could raise more cash, even just to fuel faster growth. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash to fund growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of CA$28m, Lithium Chile's CA$3.9m in cash burn equates to about 14% of its market value. Given that situation, it's fair to say the company wouldn't have much trouble raising more cash for growth, but shareholders would be somewhat diluted.

So, Should We Worry About Lithium Chile's Cash Burn?

On this analysis of Lithium Chile's cash burn, we think its cash burn relative to its market cap was reassuring, while its cash runway has us a bit worried. Considering all the measures mentioned in this report, we reckon that its cash burn is fairly risky, and if we held shares we'd be watching like a hawk for any deterioration. While we always like to monitor cash burn for early stage companies, qualitative factors such as the CEO pay can also shed light on the situation. Click here to see free what the Lithium Chile CEO is paid..

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.