Yahoo Finance

Yahoo Finance Here's Why Investors Should Retain Williams-Sonoma (WSM) Stock

Williams-Sonoma, Inc. WSM is benefiting from its solid operating model, e-commerce business and B2B initiative. The focus on digital initiatives and global expansion plans bode well. The company is expanding globally, with a particular emphasis on the Indian market, where brand momentum surpassed expectations.

However, ongoing macroeconomic uncertainty and global geopolitical tensions are concerns for the company’s growth prospects.

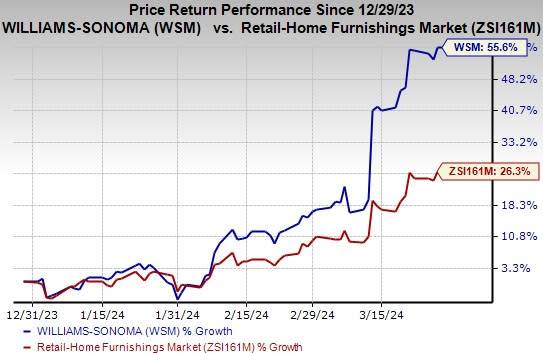

This multi-channel specialty retailer of premium quality home products has gained 55.6% in the past three months compared with the Zacks Retail - Home Furnishings industry’s 26.3% growth. The Zacks Consensus Estimate for this currently Zacks Rank #3 (Hold) company's fiscal 2025 earnings has increased to $15.37 per share from $14.69 in the past 30 days, solidifying the growth trend.

Image Source: Zacks Investment Research

The upside is supported by its solid VGM Score of A, contributed by a Momentum and Growth Score of A and a Value Score of B. The positive trend signifies bullish analysts’ sentiments, robust fundamentals and the continuation of an outperformance in the near term.

Factors Driving Growth

Focus on E-commerce Channel: Williams-Sonoma is one of the largest e-commerce retailers in the United States. Its innovative efforts have helped the company to drive e-commerce growth. E-commerce penetration has been increasing, buoyed by its in-house tech platform, rapid experimentation program, content-rich online experience and marketing strategies.

The company is focused on its best-in-class retail business. It continues to enhance in-store experiences with inspirational products and next-level design services. Its ongoing retail optimization efforts have transformed its fleet to be positioned in the most profitable, inspiring and strategic locations.

For 2024, WSM's capital allocation plans prioritize funding its business operations and investing in long-term growth. The company expects to spend 225 million in capital expenditures to invest in the long-term growth of its business, with 75% of this investment being dedicated to driving its e-commerce leadership and supply chain efficiency.

Digitalization Efforts: On the digital front, WSM maintains tight control over ad expenses, optimizing spending with a focus on the most productive channels while retaining some flexibility for experimenting with formats that engage new audiences. As one of the largest e-commerce players, the company continues to enhance its proprietary e-commerce technology stack, positioning itself as a leader in the retail industry through the utilization of AI in its tech capabilities.

During fourth-quarter fiscal 2023, WSM's Canada business saw continued momentum, driven by its focus on improving the customer experience online and in retail. The company's digital initiatives in the Canadian market are attracting new customers and driving results for its brands. WSM is pleased with the initial positive response to the recent launches of Rejuvenation, Mark and Graham and Williams-Sonoma Home in Canada. As WSM expands its omnichannel presence globally, India, Mexico and Canada remain key strategic growth markets.

B2B Strategy to Drive Growth: B2B continues to be one of the WSM's key initiatives. The B2B operates in two formats, trade and contract. With 1% year-over-year growth in overall business, the company witnessed a 31% rise in its contract business in the fiscal 2023. The upside was driven by WSM's strength in the hospitality and residential sectors. Early traction in developing segments like health care, gaming and senior living contributed to the upside. WSM is focused on accelerating its contract business, showing positive momentum.

Concerns

Williams-Sonoma’s performance is being impacted by an increase in occupancy costs, along with employment and general expenses. Also, geopolitical uncertainties are a concern.

During the fiscal 2023, selling, general and administrative expenses, as a percentage of net revenues, increased to 26.6% compared with 25.1% in the fiscal 2022. The uptick can be attributed to the deleverage of employment costs from higher performance-based incentive compensation in the fiscal 2023 compared with the fiscal 2022 commensurate with business performance.

Macroeconomic pressures continue to impact WSM's global business. For 2024, the company foresees ongoing macroeconomic uncertainty. Lower interest rates could stimulate the housing market and redirect consumer spending back to home, but the timing remains unpredictable. Factors such as the election and global geopolitical tensions contribute to this uncertainty.

Key Picks

Some better-ranked stocks in the Retail-Wholesale sector have been discussed below.

Brinker International, Inc. EAT sports a Zacks Rank #1 (Strong Buy). The company has a trailing four-quarter earnings surprise of 212.7% on average. Shares of EAT have surged 36.6% in the past year. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for EAT’s 2024 sales and EPS indicates 4.9% and 30.7% growth, respectively, from the year-ago period’s levels.

Texas Roadhouse, Inc. TXRH carries a Zacks Rank #2 (Buy). It has a trailing four-quarter negative earnings surprise of 3.9%, on average. The stock has gained 42.9% in the past year.

The Zacks Consensus Estimate for TXRH’s 2024 sales and EPS suggests rises of 14% and 25.1%, respectively, from the year-ago period’s levels.

Shake Shack Inc. SHAK carries a Zacks Rank #2. It has a trailing four-quarter earnings surprise of 92.6%, on average. SHAK’s shares have surged 93.8% in the past year.

The Zacks Consensus Estimate for SHAK’s 2024 sales and EPS indicates 14.6% and 91.9% growth, respectively, from the year-ago period’s levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Brinker International, Inc. (EAT) : Free Stock Analysis Report

Texas Roadhouse, Inc. (TXRH) : Free Stock Analysis Report

Williams-Sonoma, Inc. (WSM) : Free Stock Analysis Report

Shake Shack, Inc. (SHAK) : Free Stock Analysis Report