Yahoo Finance

Yahoo Finance Here's Why Hemisphere Energy (CVE:HME) Is Weighed Down By Its Debt Load

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Hemisphere Energy Corporation (CVE:HME) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Hemisphere Energy

How Much Debt Does Hemisphere Energy Carry?

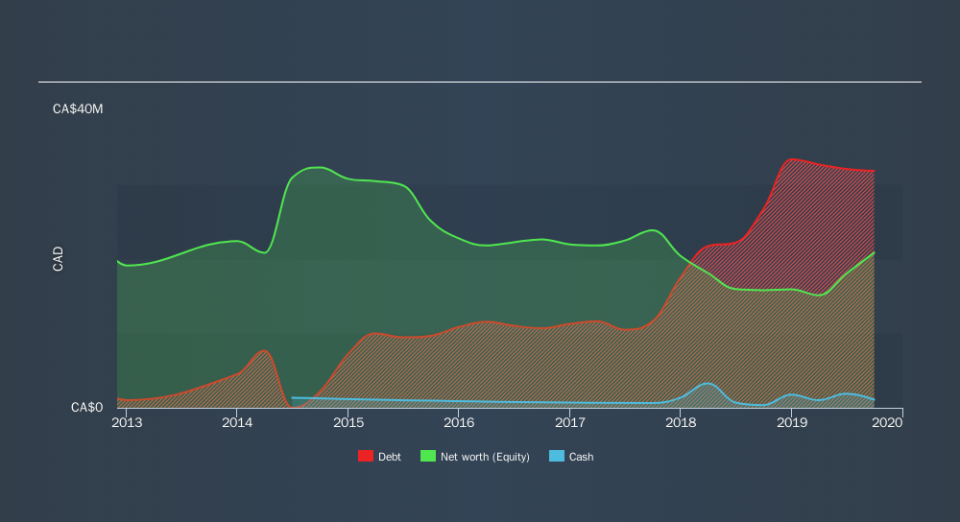

As you can see below, at the end of September 2019, Hemisphere Energy had CA$31.8m of debt, up from CA$26.6m a year ago. Click the image for more detail. However, it also had CA$1.09m in cash, and so its net debt is CA$30.7m.

How Strong Is Hemisphere Energy's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Hemisphere Energy had liabilities of CA$6.14m due within 12 months and liabilities of CA$40.6m due beyond that. On the other hand, it had cash of CA$1.09m and CA$3.37m worth of receivables due within a year. So it has liabilities totalling CA$42.3m more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the CA$13.8m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet." So we'd watch its balance sheet closely, without a doubt After all, Hemisphere Energy would likely require a major re-capitalisation if it had to pay its creditors today.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While Hemisphere Energy has a quite reasonable net debt to EBITDA multiple of 1.8, its interest cover seems weak, at 2.2. This does have us wondering if the company pays high interest because it is considered risky. In any case, it's safe to say the company has meaningful debt. We also note that Hemisphere Energy improved its EBIT from a last year's loss to a positive CA$8.9m. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Hemisphere Energy will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. During the last year, Hemisphere Energy burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

On the face of it, Hemisphere Energy's conversion of EBIT to free cash flow left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But at least its net debt to EBITDA is not so bad. Taking into account all the aforementioned factors, it looks like Hemisphere Energy has too much debt. That sort of riskiness is ok for some, but it certainly doesn't float our boat. Given the risks around Hemisphere Energy's use of debt, the sensible thing to do is to check if insiders have been unloading the stock.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.