Yahoo Finance

Yahoo Finance Here's Why Aritzia (TSE:ATZ) Can Manage Its Debt Responsibly

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Aritzia Inc. (TSE:ATZ) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Aritzia

What Is Aritzia's Debt?

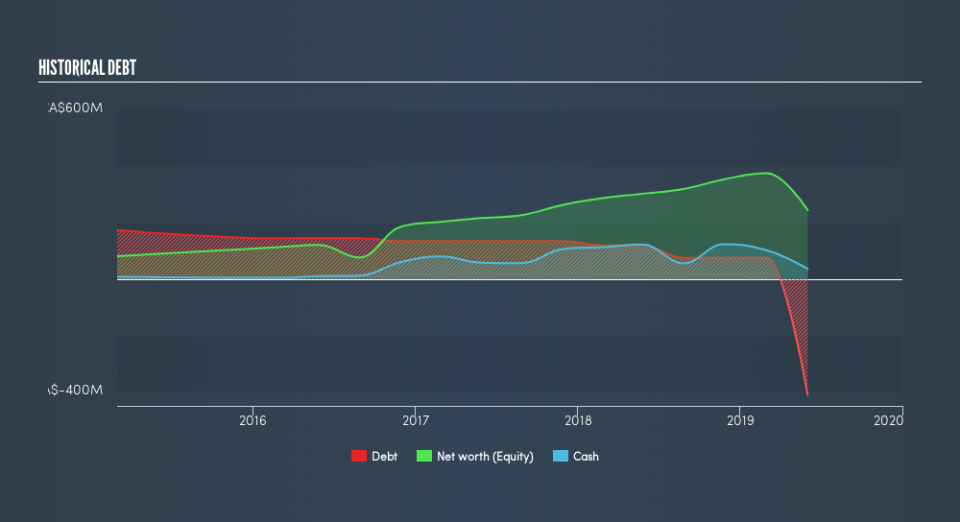

The image below, which you can click on for greater detail, shows that Aritzia had debt of CA$99.4m at the end of June 2019, a reduction from CA$118.6m over a year. However, because it has a cash reserve of CA$35.8m, its net debt is less, at about CA$63.6m.

How Strong Is Aritzia's Balance Sheet?

We can see from the most recent balance sheet that Aritzia had liabilities of CA$157.7m falling due within a year, and liabilities of CA$552.9m due beyond that. Offsetting these obligations, it had cash of CA$35.8m as well as receivables valued at CA$7.77m due within 12 months. So its liabilities total CA$667.1m more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Aritzia has a market capitalization of CA$1.92b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Aritzia's net debt is only 0.41 times its EBITDA. And its EBIT easily covers its interest expense, being 13.9 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Another good sign is that Aritzia has been able to increase its EBIT by 29% in twelve months, making it easier to pay down debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Aritzia can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the most recent two years, Aritzia recorded free cash flow worth 55% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Aritzia's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. And that's just the beginning of the good news since its EBIT growth rate is also very heartening. When we consider the range of factors above, it looks like Aritzia is pretty sensible with its use of debt. While that brings some risk, it can also enhance returns for shareholders. We'd be motivated to research the stock further if we found out that Aritzia insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.