Yahoo Finance

Yahoo Finance Here's Why Acacia Research (NASDAQ:ACTG) Can Manage Its Debt Despite Losing Money

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Acacia Research Corporation (NASDAQ:ACTG) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Acacia Research

What Is Acacia Research's Debt?

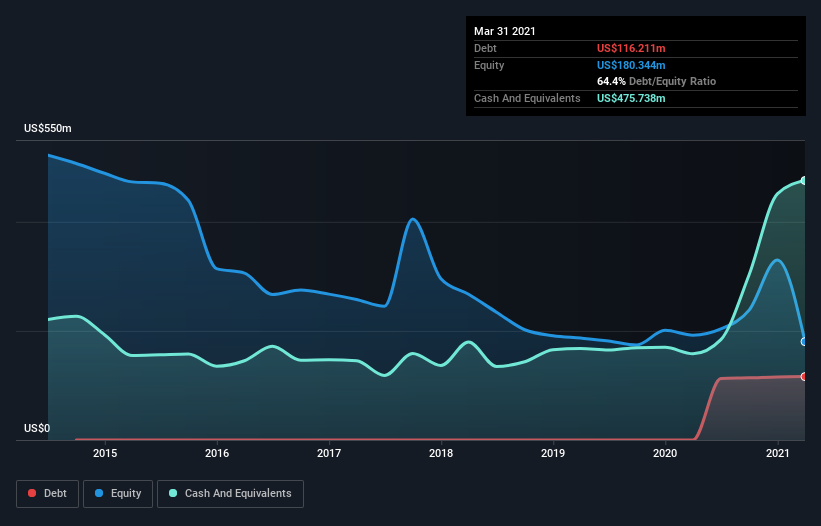

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Acacia Research had US$115.6m of debt, an increase on none, over one year. But on the other hand it also has US$475.7m in cash, leading to a US$360.1m net cash position.

How Strong Is Acacia Research's Balance Sheet?

According to the last reported balance sheet, Acacia Research had liabilities of US$138.0m due within 12 months, and liabilities of US$250.6m due beyond 12 months. Offsetting this, it had US$475.7m in cash and US$4.43m in receivables that were due within 12 months. So it actually has US$91.5m more liquid assets than total liabilities.

This surplus liquidity suggests that Acacia Research's balance sheet could take a hit just as well as Homer Simpson's head can take a punch. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Succinctly put, Acacia Research boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Acacia Research's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Acacia Research wasn't profitable at an EBIT level, but managed to grow its revenue by 172%, to US$32m. So its pretty obvious shareholders are hoping for more growth!

So How Risky Is Acacia Research?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that Acacia Research had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$43m and booked a US$34m accounting loss. But the saving grace is the US$360.1m on the balance sheet. That means it could keep spending at its current rate for more than two years. Importantly, Acacia Research's revenue growth is hot to trot. While unprofitable companies can be risky, they can also grow hard and fast in those pre-profit years. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 1 warning sign for Acacia Research that you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.