Yahoo Finance

Yahoo Finance Hancock Whitney's (HWC) Loan, Rates Aid Amid Weak Asset Quality

Hancock Whitney Corporation HWC is well-placed for revenue growth on the back of steady loan demand. High interest rates, strategic investments and a strong balance sheet position will continue to support its financials. However, subdued mortgage banking business and worsening asset quality pose near-term concerns.

Hancock Whitney acquired MidSouth Bancorp in 2019, which continues to support its top line. Over the last five years (2018-2023), revenues (on a tax-equivalent basis or TE) and total loans witnessed a compound annual growth rate (CAGR) of 4% and 3.6%, respectively. High interest rates, decent loan demand and the company’s strategic investments in growth and new markets to support fee income are expected to keep bolstering its top-line growth. We project total revenues (TE) to witness a CAGR of 2.7% over the three years ended 2026 and total loans are projected to see a CAGR of 1.6%.

Driven by higher rates, Hancock Whitney’s net interest margin (NIM) (TE) increased in 2023 to 3.34% from 3.26% in 2022 and 2.95% in 2021. However, the expansion slowed down because of rising funding costs. With the Federal Reserve expected to keep rates high in the near term, increasing funding costs will continue to exert pressure on the metric.

Nonetheless, the company’s bond restructuring and balance sheet deleveraging strategy is expected to boost NIM in upcoming quarters. Management projects NIM to increase modestly in 2024 on the assumptions of three rate cuts, stabilizing deposit cost and a rise in loan yields. We project NIM to be 3.26% in 2024 and 3.28% in both 2025 and 2026.

However, the performance of the bank’s mortgage banking business is worrisome. The company’s secondary mortgage income grew substantially till 2020, driven by low mortgage rates.

Nevertheless, as the secondary mortgage activity slowed down since the second half of 2021, the income from the same declined as well. The company’s secondary mortgage market income witnessed a negative CAGR of 38.9% over the last three years (2020-2023). With mortgage rates expected to remain high in the near term, Hancock Whitney is expected to witness limited improvement in income generated from the same.

Weakening asset quality is another headwind for HWC. While provision for credit losses and net charge-offs declined in 2021 and 2022, both metrics increased in 2023 on expectations of a worsening economic backdrop. Though the near-term recession risks have faded, expectations of an economic slowdown could keep the asset quality under pressure. We project provision for credit losses to rise 24.7% this year.

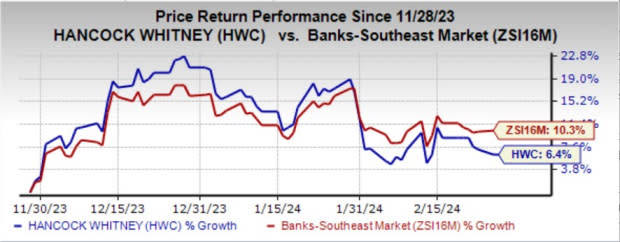

HWC currently carries a Zacks Rank #3 (Hold). Shares of the company have gained 6.4% over the past three months compared with the industry’s growth of 10.3%.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked bank stocks are Bank7 Corp. BSVN and Home Bancshares, Inc. HOMB.

Bank7’s earnings estimates for the current year have moved north by 5.8% in the past 30 days. The company’s shares have gained 11.3% over the past three months. At present, BSVN sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Home Bancshares’ 2024 earnings estimates have been revised slightly upward in the past 30 days. The stock has gained 6.7% over the past three months. Currently, HOMB sports a Zacks Rank #1.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Home BancShares, Inc. (HOMB) : Free Stock Analysis Report

Hancock Whitney Corporation (HWC) : Free Stock Analysis Report

Bank7 Corp. (BSVN) : Free Stock Analysis Report