Yahoo Finance

Yahoo Finance If You Had Bought salesforce.com (NYSE:CRM) Stock Five Years Ago, You Could Pocket A 174% Gain Today

When you buy a stock there is always a possibility that it could drop 100%. But on the bright side, you can make far more than 100% on a really good stock. For example, the salesforce.com, inc. (NYSE:CRM) share price has soared 174% in the last half decade. Most would be very happy with that.

View our latest analysis for salesforce.com

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

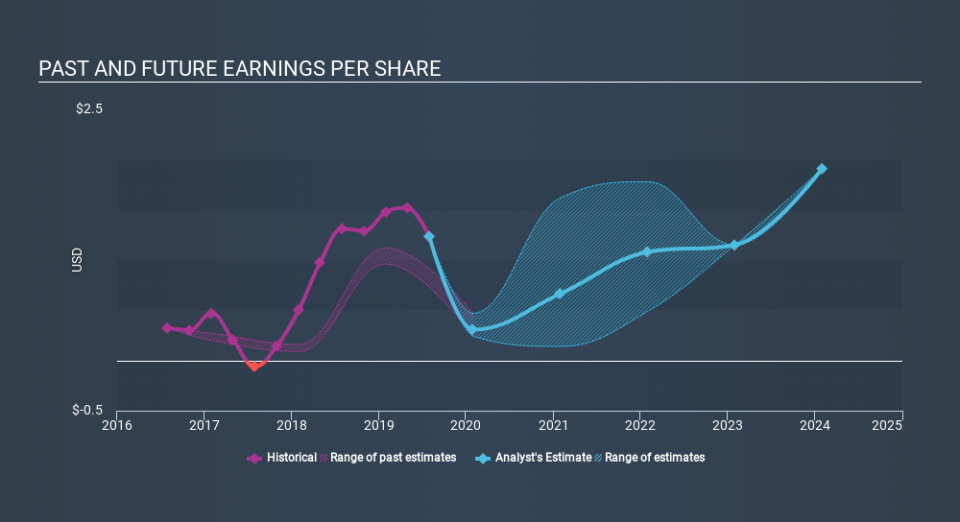

During the last half decade, salesforce.com became profitable. That kind of transition can be an inflection point that justifies a strong share price gain, just as we have seen here. Since the company was unprofitable five years ago, but not three years ago, it's worth taking a look at the returns in the last three years, too. Indeed, the salesforce.com share price has gained 136% in three years. During the same period, EPS grew by 56% each year. This EPS growth is higher than the 33% average annual increase in the share price over the same three years. Therefore, it seems the market has moderated its expectations for growth, somewhat. Having said that, the market is still optimistic, given the P/E ratio of 130.82.

The image below shows how EPS has tracked over time (if you click on the image you can see greater detail).

It is of course excellent to see how salesforce.com has grown profits over the years, but the future is more important for shareholders. If you are thinking of buying or selling salesforce.com stock, you should check out this FREE detailed report on its balance sheet.

A Different Perspective

It's good to see that salesforce.com has rewarded shareholders with a total shareholder return of 13% in the last twelve months. However, that falls short of the 22% TSR per annum it has made for shareholders, each year, over five years. The pessimistic view would be that be that the stock has its best days behind it, but on the other hand the price might simply be moderating while the business itself continues to execute. Most investors take the time to check the data on insider transactions. You can click here to see if insiders have been buying or selling.

We will like salesforce.com better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.