Yahoo Finance

Yahoo Finance If You Had Bought Quorum Information Technologies (CVE:QIS) Shares Five Years Ago You'd Have Earned 89% Returns

While Quorum Information Technologies Inc. (CVE:QIS) shareholders are probably generally happy, the stock hasn't had particularly good run recently, with the share price falling 17% in the last quarter. But that doesn't change the fact that the returns over the last five years have been pleasing. After all, the share price is up a market-beating 89% in that time.

See our latest analysis for Quorum Information Technologies

Given that Quorum Information Technologies didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. When a company doesn't make profits, we'd generally expect to see good revenue growth. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

For the last half decade, Quorum Information Technologies can boast revenue growth at a rate of 26% per year. Even measured against other revenue-focussed companies, that's a good result. It's good to see that the stock has 14%, but not entirely surprising given revenue shows strong growth. If the strong revenue growth continues, we'd expect the share price to follow, in time. Of course, you'll have to research the business more fully to figure out if this is an attractive opportunity.

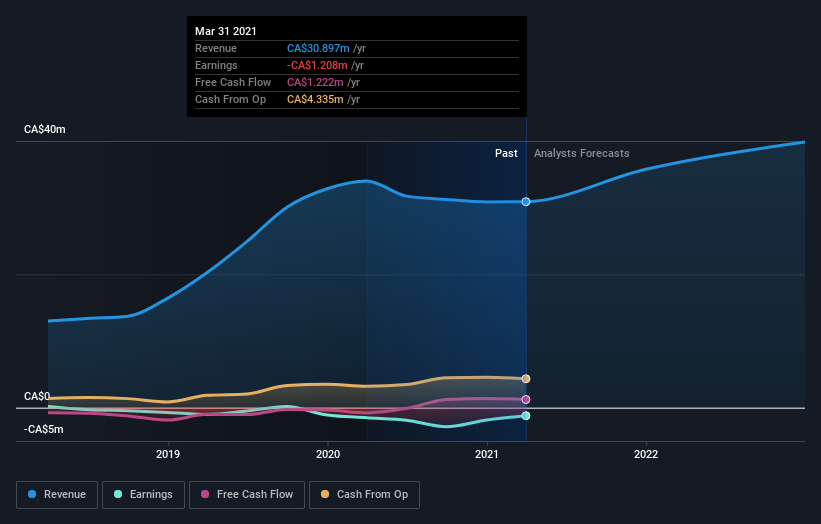

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

This free interactive report on Quorum Information Technologies' balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

Quorum Information Technologies shareholders gained a total return of 16% during the year. But that was short of the market average. The silver lining is that the gain was actually better than the average annual return of 14% per year over five year. This suggests the company might be improving over time. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For example, we've discovered 3 warning signs for Quorum Information Technologies (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on CA exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.