Yahoo Finance

Yahoo Finance Gilead (GILD) Loses 17.6% YTD: How Should You Play the Stock?

Biotech giant Gilead Sciences, Inc. GILD, a leader in HIV drugs, is having a tough run as recent pipeline setbacks disappointed investors and acquisition-related charges adversely impacted the bottom line. The stock has been under pressure owing to these challenges.

While the company’s leading HIV franchise maintains momentum and its efforts to build an oncology franchise to diversify its portfolio are encouraging, the failure of late-stage studies evaluating oncology drug Trodelvy (sacituzumab govitecan) in additional indications was a major setback and dampened investor sentiment.

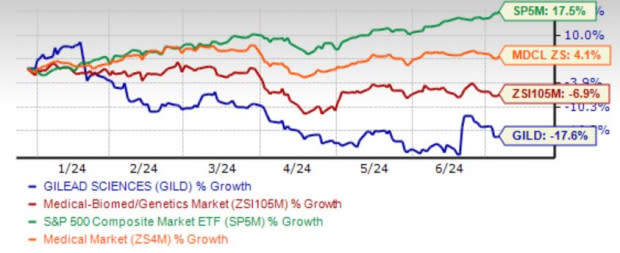

Consequently, GILD’s shares took a beating. Shares of the company have lost 17.6% year to date compared with the industry’s decline of 6.9%. The stock has also grossly underperformed the sector and the S&P 500.

Gilead Underperforms Industry, Sector & S&P 500

Image Source: Zacks Investment Research

Leading HIV Franchise Maintains Momentum

Gilead boasts an industry-leading HIV franchise, having successfully transitioned its portfolio to drugs with improved long-term safety profiles. With a market share of 49% in the United States at the end of the first quarter, flagship HIV therapy, Biktarvy, continues to maintain its strong growth, thereby fueling the top line. Gilead expects HIV drug sales to grow 4% in 2024.

Last month, Gilead’s shares got a boost after it reported upbeat top-line results from an interim analysis of its late-stage study evaluating the safety and efficacy of twice-yearly, subcutaneous lenacapavir for pre-exposure prophylaxis (PrEP) and once-daily oral Descovy in cisgender women and adolescent girls aged 16-25 years across 25 sites in South Africa and three in Uganda. Lenacapavir demonstrated 100% efficacy for the investigational use of HIV prevention in cisgender women.

The development and approval of lenacapavir for PrEP should solidify Gilead’s HIV franchise, as lenacapavir needs to be taken twice yearly, unlike daily oral pills.

Recent Acquisition, Deals to Diversify Portfolio Bode Well

The recent acquisition of clinical-stage biopharmaceutical company, CymaBay Therapeutics, added an investigational lead product candidate, seladelpar, to Gilead’s pipeline. The candidate is under review in the United States with a target action date next month. A potential approval should expand Gilead’s liver disease portfolio.

GILD also recently entered into a research collaboration, option and license agreement with Merus MRUS to discover novel dual tumor-associated antigens targeting trispecific antibodies.

Pipeline Setbacks Weigh

Gilead’s oncology portfolio, comprising the Cell Therapy franchise and breast cancer drug Trodelvy, has diversified the company’s overall business. The Cell Therapy franchise, comprising Yescarta and Tecartus, continues to witness a steady increase in sales, primarily due to higher demand for Yescarta in relapsed or refractory (R/R) large B-Cell lymphoma and Tecartus in R/R acute lymphoblastic leukemia and mantle cell lymphoma.

Breast cancer drug Trodelvy’s performance has been strong since its approval. The drug is driving Gilead's efforts to build a strong oncology franchise, especially given the current focus on ADCs.

However, Gilead’s efforts to expand Trodelvy’s label suffered a setback due to the failure of its late-stage confirmatory TROPiCS-04 study on Trodelvy in locally advanced or metastatic urothelial cancer. In January, the late-stage study evaluating Trodelvy in previously treated metastatic non-small cell lung cancer also failed. These failures have somewhat dented Gilead’s efforts to strengthen its oncology franchise.

Valuation & Estimates

From a price perspective, Gilead is currently trading toward the low end of the 52-week range. It’s worth noting that the annual earnings estimates have taken a hit due to acquisition-related expenses in 2024.

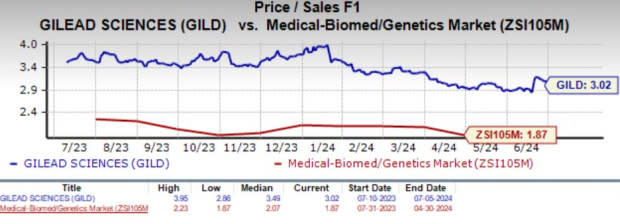

Going by the price/sales ratio, GILD’s shares currently trade at 3.02x forward sales, higher than 1.87 for the industry but lower than its mean of 3.49.

Image Source: Zacks Investment Research

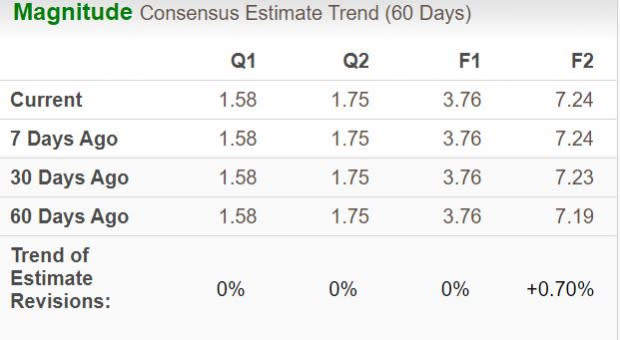

Estimate Movement

The Zacks Consensus Estimate for its 2024 earnings per share (EPS) has remained unchanged at $3.76 over the past 60 days. Nevertheless, the EPS for 2025 has increased from $7.19 to $7.24 during the same time frame.

Image Source: Zacks Investment Research

Conclusion

Gilead’s efforts to constantly innovate its HIV portfolio should enable it to maintain growth amid competition from GSK plc GSK. The company’s strategic deals and acquisitions to diversify its business are encouraging. However, its recent pipeline setbacks are a matter of concern.

At current levels, we would not advise the investors to either buy or sell the stock. For investors already owning the stock, staying invested will be a prudent move as the company transitions its overall portfolio and waddles through expenses. In fact, the long-term estimates show an upward trend, giving a reason to be optimistic.

A key attraction to stay invested is the company’s dividend yield. Gilead has been consistently increasing and paying out dividends. Its strong cash position (as of Mar 31, 2024, Gilead had $4.7 billion of cash, cash equivalents and marketable debt securities) indicates that the current yield of 4.6% is likely to be sustainable.

Gilead currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

GSK PLC Sponsored ADR (GSK) : Free Stock Analysis Report

Gilead Sciences, Inc. (GILD) : Free Stock Analysis Report

Merus N.V. (MRUS) : Free Stock Analysis Report