Yahoo Finance

Yahoo Finance FP Answers: The Bank of Canada lost $522 million in three months — here's why

In an increasingly complex world, the Financial Post should be the first place you look for answers. Our FP Answers initiative puts readers in the driver’s seat: you submit questions and our reporters find answers not just for you, but for all our readers. Today, we answer a question about the Bank of Canada‘s balance sheet.

Tiff Macklem‘s “announcement” during testimony at the House finance committee last week that the Bank of Canada, which typically sends about $1 billion to the federal treasury each year, is about to record losses for the first time in its 87-year history was news only because it was the first time the governor described the state of the central bank’s finances himself.

Anyone watching the evolution of the Bank of Canada’s balance sheet could see the value of the central bank’s liabilities were climbing faster than the value of its assets. The Toronto Star was the first to do the math, forcing the central bank to acknowledge in an article published on Sept. 12 that its net interest income was on track “to be negative when our third-quarter results are published on Nov. 29.” The Financial Post followed with a report of its own a few days later. The Globe and Mail published a story on Nov. 15.

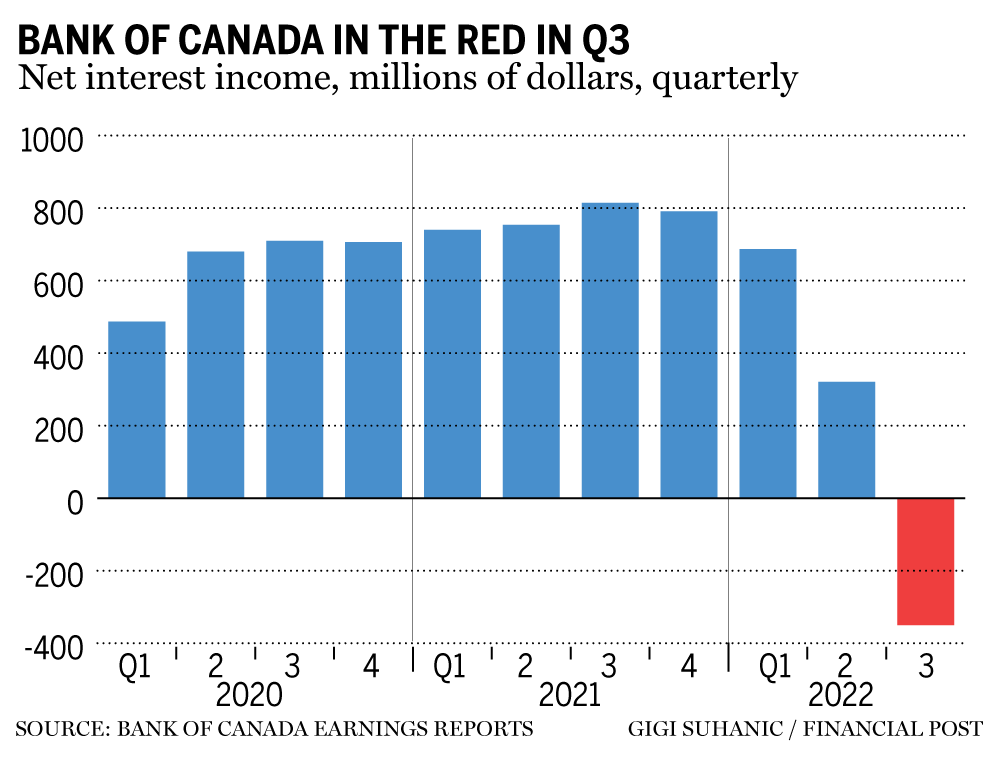

Those math-based prophecies came true on Nov. 29, when the Bank of Canada reported that it lost $522 million in the three-month period ended Sept. 30, as “net interest revenue” came in as a loss of $350 million, compared with a gain of $814 million in the year-earlier period.

Yet at least some members of Parliament appeared surprised and/or befuddled by the state of the Bank of Canada’s balance sheet, and our story on Macklem’s concession that he was about to become the overseer of a money-losing operation was one of the most read articles on the Financial Post’s website. A subject that involves accounting, raises questions about the Bank of Canada’s credibility and independence, and raises even more questions about the long-term implications of the central bank’s ballooning liabilities probably deserves more than a few newspaper articles. Here’s our best attempt at what you need to know.

Why is the Bank of Canada losing money?

The Bank of Canada isn’t a bank like Royal Bank of Canada or Bank of Nova Scotia. True, it’s a Crown corporation, but profits and losses are merely a byproduct of its legislative mission to “regulate credit and currency in the best interests of the economic life of the nation, to control and protect the external value of the national monetary unit and to mitigate by its influence fluctuations in the general level of production, trade, prices and employment, so far as may be possible within the scope of monetary action, and generally to promote the economic and financial welfare of Canada.”

Now, the absence of a profit motive doesn’t mean the central bank’s founders were indifferent to losses. The institution is set up in such a way that its assets — mostly seigniorage, or the difference between the value of currency that the central bank issues on behalf of the government and the cost of producing it — should typically exceed its liabilities, mostly deposits from the country’s biggest financial institutions.

Private lenders need to keep enough money at the central bank to clear large payments, but they typically have little incentive to stash any more money with the Bank of Canada than necessary because they can usually find more profitable uses for it elsewhere. (This is how the Bank of Canada reinforces its benchmark interest rate. The amount that the central bank is willing to pay on deposits becomes the effective floor for the rest of the financial system, as the big banks base the rates they charge customers on what they could earn on ultra-safe deposits at the central bank.)

The COVID crisis forced the Bank of Canada’s leaders to blow up this comfortable equilibrium. They dropped the benchmark interest rate to 0.25 per cent, but sensed that wouldn’t be enough to keep fear from spreading through financial markets and causing serious harm to the “economic life of the nation.” Stephen Poloz, who was nearing the end of his term as governor at the onset of the pandemic in early 2020, decided to exercise the central bank’s unique power to create money and began buying government bonds from private lenders by adding to their deposit accounts at the central bank.

Economists call the strategy “quantitative easing,” or QE. It allows central banks to stabilize financial markets during panics by providing lenders with a source of liquidity at a moment when financial institutions are fearful of letting go of their cash. QE also helps put downward pressure on interest rates by increasing the demand for safe assets, forcing investors who are crowded out by the central bank’s purchases to seek out riskier assets. The U.S. Federal Reserve successfully deployed QE to reverse the Great Recession, although with the benefit of hindsight, most mainstream experts had determined that the damage would have been less severe if the Fed had acted sooner and with greater force. With this knowledge in mind, the Bank of Canada moved aggressively, at one point creating $5-billion worth of “settlement balances” per week to purchase government debt from the big financial institutions that are approved to deposit funds at the central bank.

The asset side of its balance sheet peaked at $575 billion, compared with about $120 billion in March 2020. For a while, it looked like a profitable venture, as the value of assets it purchased at depressed prices during a panic rose in value as the economy got back to normal. But then, inflation spiked, threatening the “economic life of the nation” anew. For much of this year, Macklem has been raising interest rates as aggressively as he was buying bonds during the recession, lifting the benchmark interest rate to 3.75 per cent through October from 0.25 per cent in March, while stating repeatedly in the weeks since his most recent increase that he isn’t finished.

Higher interest rates will eventually take the heat out of inflation: the consumer price index increased 6.9 per cent in October from a year earlier, down from 8.1 per cent this summer, suggesting price pressures are starting to recede.

However, a side effect of ratcheting up interest rates so quickly is that the cost of holding all those bank deposits now exceeds the value of the central bank’s assets. It’s not exactly an unintended consequence of QE, since the central bank knew it was exposing itself to greater financial risk by loading up its balance sheet with bonds. But it’s a reminder that monetary policy isn’t magic, or at least not magic enough to defy the very real-world power of accounting principles.

Why does it matter?

The answer depends on how much you trust your government and the technocrats who have been hired to manage the affairs of the nation.

Macklem told lawmakers that the Bank of Canada’s losses are “largely accounting issues” that have no bearing on the central bank’s efforts to contain inflation, which the institution and the government determined three decades ago was the best way to execute the mission set for it in the Bank of Canada Act.

“Low inflation is a public good,” Macklem told the finance committee. “We run monetary policy to deliver low and stable inflation,” not to make a profit, he said.

But as anyone who has read the comment sections of our stories on this subject knows, not everyone trusts the government and the technocrats who have been hired to manage the affairs of the nation. Pierre Poilievre politicized this distrust during his successful campaign to take over as leader of the Opposition, pledging to fire Macklem if he wins the next election. His move into Stornaway has done nothing to soften his rhetoric, as the central bank remains a foil in his attacks on Prime Minister Justin Trudeau and the Ottawa establishment.

“What happened was the government was running deficits that they could not borrow from the marketplace because there was not enough lenders on planet Earth that would have lent the half-trillion dollars that Trudeau was borrowing,” Poilievre told the Empire Club in Toronto earlier this month. “He also wanted to be able to say he was doing it at record low rates — something that wouldn’t have happened if the market mechanism would have allowed supply and demand to move the bond yields up as you would normally expect if the government were borrowing that quantity of cash out of the economy in such a short period of time.”

The size of losses that will ultimately be the responsibility of taxpayers to cover could raise concerns about the Bank of Canada’s independence, since it will need some kind of bailout from Trudeau’s government. Macklem assured the finance committee that the losses would be temporary, but red ink could also make for an easy way for critics to cast doubt on the central bank’s credibility and competence. Macklem and the Bank of Canada already have been absorbing blows from both Conservative and New Democratic politicians for months.

Conservatives demonstrated how far they are willing to go in their criticism of Macklem at the finance committee. Former leader Andrew Scheer, who isn’t a member of the committee, nonetheless used most of the time allotted to his party for questions. At one point, Scheer asked Macklem if he thought the bonuses earned by Bank of Canada staff were inflationary, an absurd suggestion that was a naked attempt to stir resentment.

Less absurd, although probably still unfair, was Scheer’s question about whether QE had the effect of enriching the country’s already (very) profitable banks. The Bank of Canada purchased the debt in the secondary bond market, rather than directly from the government, so there was a spread. Still, buying from the source would have meant buying from itself, since the Bank of Canada acts as the government’s debt agent.

“I don’t know if the banks do anything for free,” said Scheer, a barely disguised shot at the Bank of Canada’s credibility as an institution focused on households, rather than the needs of the corporate elite.

What is to be done?

The Bank of Canada Act prevents governor Tiff Macklem from reserving net income when there’s a surplus, so there is no fix without government intervention. Finance Minister Chrystia Freeland so far has said nothing about what she intends to do, and she received no questions on the matter when she testified at the finance committee on Nov. 28.

One fix would be to change the law and allow the Bank of Canada to retain its earnings. That would allow officials to book losses on the understanding that it would pay for them later, like any other going concern in similar circumstances.

The U.S. Federal Reserve used GAAP accounting standards, which allow the Fed to turn negative equity into a deferred asset, which it will then run down over time as earnings turn positive.

Other central banks have been extended an indemnity by their governments, which shifts the losses to taxpayers. The Bank of Canada actually has an indemnity from the Trudeau government, but, as senior deputy Carolyn Rogers told the finance committee, it only covers “market losses” on the assets purchased during QE that are then sold at a loss. “We are not planning to do that,” she said, so another option would be to “extend the range” of the existing indemnity to cover operating losses.

The Bank of Canada is losing money for the first time ever on rising rates

Tiff Macklem acknowledges the Bank of Canada is losing money for first time

FP Answers: Should I commute my pension and take $1.1 million to retire now?

FP Answers: Is paying down my mortgage or investing in RESPs the better choice?

“This is a decision for government,” Rogers said. “They are actively working on it right now. We expect in the coming future that they will make a final decision.”

The C.D. Howe Institute, a think-tank that follows the Bank of Canada and monetary policy closely, published a report last week that recommends changing the law to allow the central bank to book deferred assets. The study noted that changes to the financial system, including the potential adoption of a central bank digital currency, could force the central bank to carry more assets on its balance sheet than in the past. That would mean a greater risk of losses in the future.

Macklem demurred when asked how the problem should be solved, although he indicated he would like to use the Bank of Canada’s “profits in some way to fill in the deficits.” He also said that when all of this over, and inflation is back at the central bank’s two per cent target, “we are going to have to have a thorough review of how all our tools worked” through the pandemic.

“We didn’t get everything right,” he said. “We got a lot of things right. We have some lessons to learn.”

• Email: kcarmichael@postmedia.com | Twitter: CarmichaelKevin

• Email: shughes@postmedia.com | Twitter: StephHughes95