Yahoo Finance

Yahoo Finance Flowers Foods (FLO) Down More Than 15% in a Year: Here's Why

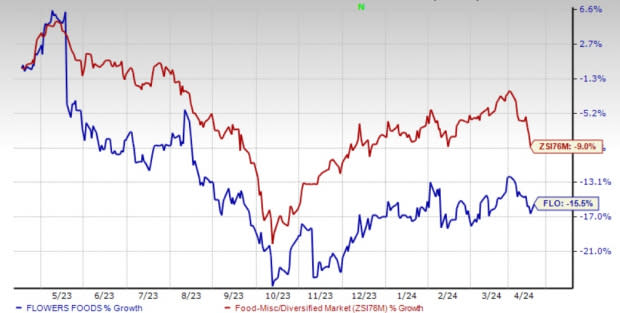

Flowers Foods, Inc. FLO appears troubled, with its shares down 15.5% in a year compared with the industry’s decline of 9%. The company has been battling a volatile consumer landscape, which remains a threat to demand.

Also, high selling, distribution and administrative (SD&A) expenses have been a concern for Flowers Foods. Apart from this, this Zacks Rank #4 (Sell) company anticipates business exits to have an impact, particularly in the first half of 2024. While these exits may be part of strategic adjustments, they could lead to short-term disruptions and revenue loss if not managed effectively.

The Zacks Consensus Estimate for the current fiscal year earnings per share has decreased by a penny to $1.25 over the past 60 days.

Image Source: Zacks Investment Research

Factors Acting as Deterrents

Flowers Foods is battling hurdles due to cost inflation. In the fourth quarter of fiscal 2023, materials, supplies, labor and other production costs (excluding depreciation and amortization) were partly impacted by elevated labor and maintenance costs. The inflationary environment may continue to pose challenges for the company, potentially impacting consumer purchasing power and input costs, which could affect profitability.

Flowers Foods’ SD&A expenses came in at 39.7% of sales in the fourth quarter, up 180 bps. Adjusted SD&A expenses expanded 150 bps to 39.4% of sales. This can be mainly attributed to higher labor, insurance, marketing and technology expenses. The adjusted EBITDA margin was 8.5%, contracting 40 bps due to inflated labor, repair and maintenance costs, along with digital and marketing investments. While FLO expects growth initiatives to drive additional volume and fill capacity with higher-margin business over time, the short-term impact of overhead costs may affect profitability.

Apart from this, on its fourth-quarter 2023 earnings call, Flowers Foods stated that consumer response to promotions reverted somewhat toward more historic levels in 2023. If promotional effectiveness diminishes or promotional activity becomes less impactful, the company may face challenges in driving sales growth and maintaining market share.

Flowers Foods remains cautious about the back half of 2024 due to the uncertain consumer and promotional environment. This uncertainty could affect consumer behavior, promotional effectiveness and overall demand for the company's products, potentially impacting financial performance. The company’s sales forecast for 2024 considers slight volume degradation from continuing category declines and selected business exits, with most of the impact concentrated in the first half of the year.

Looking Ahead

Flowers Foods has been on track with its core priorities, which include developing its team, concentrating on brands, prioritizing margins and looking out for prudent mergers and acquisitions. Effective pricing efforts have also been an upside. However, the abovementioned hurdles pose concerns for the near term.

For fiscal 2024, management expects sales in the range of $5.091-5.172 billion, suggesting flat to a 1.6% increase year over year. Adjusted EBITDA is likely to be in the range of $524-$553 million compared with the $501.7 million recorded in fiscal 2023. For fiscal 2024, the adjusted EPS is envisioned in the range of $1.20-$1.30 compared with $1.20 delivered in fiscal 2023.

3 Appetizing Bets

Vital Farms Inc. VITL offers a range of produced pasture-raised foods. It currently carries a Zacks Rank #2 (Buy). VITL has a trailing four-quarter average earnings surprise of 155.4%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Vital Farms’ current financial-year sales and earnings suggests growth of 18.7% and 30.5%, respectively, from the year-ago reported numbers.

Utz Brands Inc. UTZ manufactures a diverse portfolio of salty snacks and currently carries a Zacks Rank #2. UTZ has a trailing four-quarter earnings surprise of 2.6%, on average.

The Zacks Consensus Estimate for Utz Brands’ current financial-year earnings suggests growth of 19.3% from the year-ago reported numbers.

Celsius Holdings CELH, which offers functional drinks and liquid supplements, currently carries a Zacks Rank #2. CELH has a trailing four-quarter earnings surprise of 67.4%, on average.

The Zacks Consensus Estimate for Celsius Holdings’ current financial-year sales and earnings suggests growth of 41.6% each from the year-ago reported figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Flowers Foods, Inc. (FLO) : Free Stock Analysis Report

Celsius Holdings Inc. (CELH) : Free Stock Analysis Report

Vital Farms, Inc. (VITL) : Free Stock Analysis Report

Utz Brands, Inc. (UTZ) : Free Stock Analysis Report