Yahoo Finance

Yahoo Finance First Quantum Minerals (TSE:FM) Has A Somewhat Strained Balance Sheet

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies First Quantum Minerals Ltd. (TSE:FM) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for First Quantum Minerals

What Is First Quantum Minerals's Debt?

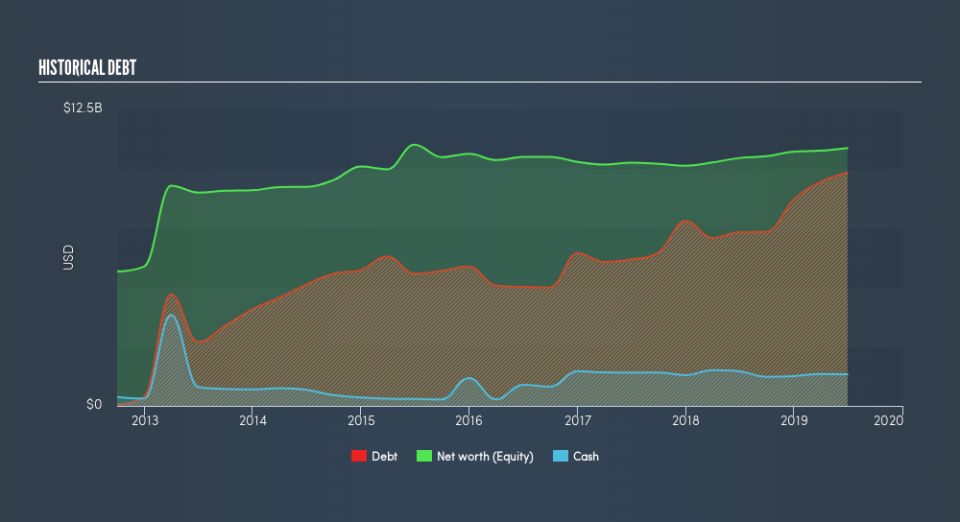

The image below, which you can click on for greater detail, shows that at June 2019 First Quantum Minerals had debt of US$9.83b, up from US$7.32b in one year. However, it also had US$1.33b in cash, and so its net debt is US$8.50b.

A Look At First Quantum Minerals's Liabilities

We can see from the most recent balance sheet that First Quantum Minerals had liabilities of US$2.07b falling due within a year, and liabilities of US$11.9b due beyond that. Offsetting this, it had US$1.33b in cash and US$720.0m in receivables that were due within 12 months. So it has liabilities totalling US$11.9b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$4.22b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, First Quantum Minerals would probably need a major re-capitalization if its creditors were to demand repayment.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

As it happens First Quantum Minerals has a fairly concerning net debt to EBITDA ratio of 5.3 but very strong interest coverage of 1k. So either it has access to very cheap long term debt or that interest expense is going to grow! It is well worth noting that First Quantum Minerals's EBIT shot up like bamboo after rain, gaining 49% in the last twelve months. That'll make it easier to manage its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if First Quantum Minerals can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, First Quantum Minerals saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

To be frank both First Quantum Minerals's conversion of EBIT to free cash flow and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But at least it's pretty decent at covering its interest expense with its EBIT; that's encouraging. Looking at the bigger picture, it seems clear to us that First Quantum Minerals's use of debt is creating risks for the company. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of First Quantum Minerals's earnings per share history for free.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.