Yahoo Finance

Yahoo Finance Exploring Undervalued TSX Stocks With Intrinsic Discounts Ranging From 25% To 39.5%

Amidst a landscape where both the U.S. and Canadian economies are showing signs of moderated inflation and central banks are adjusting interest rates accordingly, investors might find opportunities in undervalued stocks. These stocks, potentially overlooked in broader market movements, could offer intrinsic value that aligns well with the current economic adjustments.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

Name | Current Price | Fair Value (Est) | Discount (Est) |

Calibre Mining (TSX:CXB) | CA$1.80 | CA$3.15 | 42.8% |

Trisura Group (TSX:TSU) | CA$42.07 | CA$80.18 | 47.5% |

Kinaxis (TSX:KXS) | CA$149.05 | CA$250.87 | 40.6% |

Viemed Healthcare (TSX:VMD) | CA$10.45 | CA$20.08 | 48% |

Aura Minerals (TSX:ORA) | CA$13.00 | CA$21.49 | 39.5% |

Endeavour Mining (TSX:EDV) | CA$28.43 | CA$54.00 | 47.4% |

Green Thumb Industries (CNSX:GTII) | CA$15.45 | CA$27.23 | 43.3% |

Jamieson Wellness (TSX:JWEL) | CA$27.46 | CA$46.80 | 41.3% |

Kits Eyecare (TSX:KITS) | CA$8.35 | CA$14.30 | 41.6% |

Capstone Copper (TSX:CS) | CA$8.93 | CA$16.36 | 45.4% |

Below we spotlight a couple of our favorites from our exclusive screener

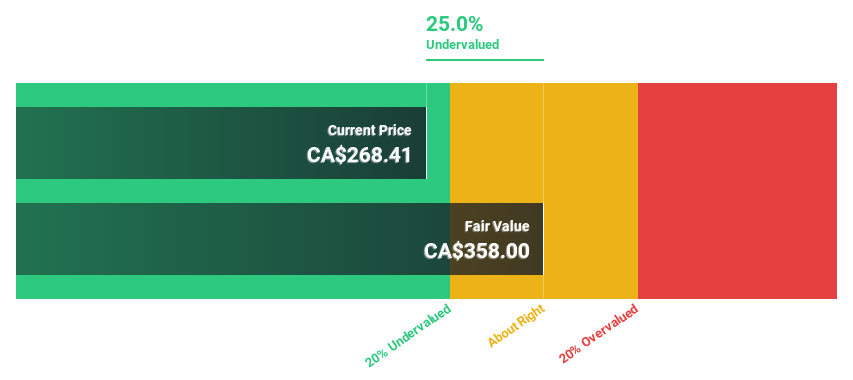

Boyd Group Services

Overview: Boyd Group Services Inc. operates non-franchised collision repair centers across North America, with a market capitalization of approximately CA$5.76 billion.

Operations: The company generates CA$3.02 billion from automotive collision repair and related services.

Estimated Discount To Fair Value: 25%

Boyd Group Services is trading 25% below its estimated fair value of CA$358, signaling potential undervaluation based on discounted cash flows. Despite recent earnings volatility, with a significant drop in Q1 2024 net income to US$8.38 million from US$20.82 million year-over-year, the company's long-term prospects appear robust. Analysts forecast Boyd's earnings to grow by 37.57% annually over the next three years, outpacing the Canadian market projection of 14.7%. However, interest payments are not well-covered by earnings, indicating some financial risk amidst strong growth expectations and market performance forecasts.

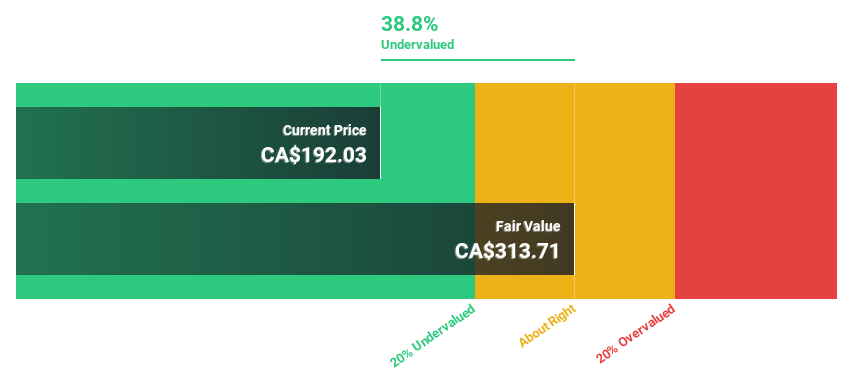

goeasy

Overview: goeasy Ltd., operating under the easyhome, easyfinancial, and LendCare brands, offers non-prime leasing and lending services to Canadian consumers with a market capitalization of approximately CA$3.22 billion.

Operations: The company generates revenue through its easyhome and easyfinancial segments, bringing in CA$153.99 million and CA$1.17 billion respectively.

Estimated Discount To Fair Value: 38.8%

goeasy Ltd. is currently priced at CA$192.03, well below its estimated fair value of CA$313.71, marking a significant undervaluation based on discounted cash flows. The company’s recent financial results show robust growth with revenue up to CA$357.11 million from CA$287.3 million year-over-year and net income rising to CA$58.94 million from CA$51.44 million, indicating strong operational performance despite a slight decline in sales volume for the first quarter of 2024 compared to the previous year's same period (CA$24.74 million versus CA$25.57 million). However, its dividend coverage by cash flow appears weak, suggesting potential sustainability issues for payouts amidst otherwise solid financial health and growth forecasts.

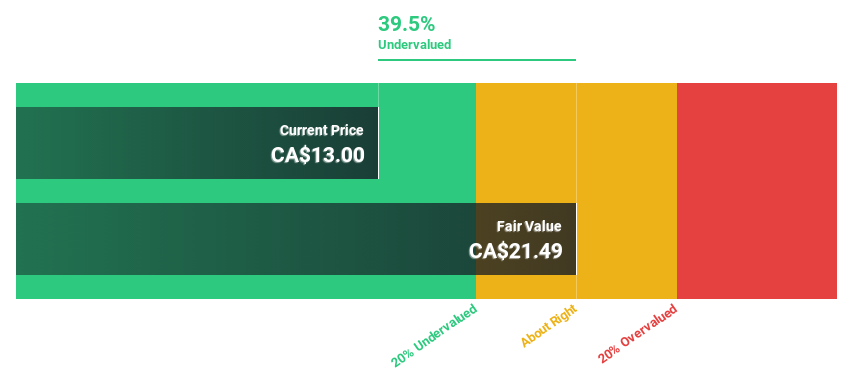

Aura Minerals

Overview: Aura Minerals Inc. is a company engaged in the production of gold and copper, specializing in the development and operation of gold and base metal projects across the Americas, with a market capitalization of approximately CA$941.63 million.

Operations: The revenue segments for the company are generated from Minosa at $134.01 million, Aranzazu at $174.23 million, and Apoena Mine at $85.23 million.

Estimated Discount To Fair Value: 39.5%

Aura Minerals is trading at CA$13, significantly below its estimated fair value of CA$21.49, suggesting deep undervaluation based on discounted cash flows. Despite a challenging quarter with a net loss of US$9.22 million and low profit margins, Aura's earnings are expected to grow by 44.48% annually over the next three years, outpacing the Canadian market's forecasted growth. However, its dividends appear unsustainable due to poor coverage by earnings and cash flows. Recent strategic acquisitions and expansion into new projects in Brazil indicate potential for future revenue growth and resource expansion.

Key Takeaways

Access the full spectrum of 23 Undervalued TSX Stocks Based On Cash Flows by clicking on this link.

Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Looking For Alternative Opportunities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include TSX:BYD TSX:GSYTSX:ORA and

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com