Yahoo Finance

Yahoo Finance Examining ServiceNow's Undervalued Growth Potential

ServiceNow Inc. (NYSE:NOW) has been a great compounder. Its share price has increased from just $24.60 in 2012 to $745 at the time of writing, delivering to shareholders an impressive compounded annual return of 33.80% over the past 11 years. Some investors may be regretting not getting into the stock previously. However, even after the huge share price appreciation, I think it is still quite undervalued currently.

Consistent growth in customer numbers, annual contract value and high retention rate

One of the leaders in providing cloud-based, intelligent workflow automation solutions, the company's main product, the Now Platform, helps corporations streamline workflows across different functions, such as human resources, IT and customer service. ServiceNow empowers its customers to enhance productivity, deliver better experiences to their employees and improve their business results. The company has an impressive client base. Around 85% of the Fortune 500 companies are its customers. This widespread adoption of ServiceNow's products among the largest global corporations highlight its product quality and customer service.

ServiceNow has been able to keep expanding its customer base and increasing the average annual contract value of its clients, especially the high-value customers, with an ACV of more than $1 million. From the fourth quarter of 2021 to the fourth quarter of 2023, the number of customers with high ACV surged from 1,350 to 1,897. Furthermore, during this period, the average ACV for these clients also rose from $3.80 million to $4.50 million. This growth emphasizes the company's ability to not only attract new high-value customers, but also upsell other products and services to existing clients.

Source: ServiceNow's presentation

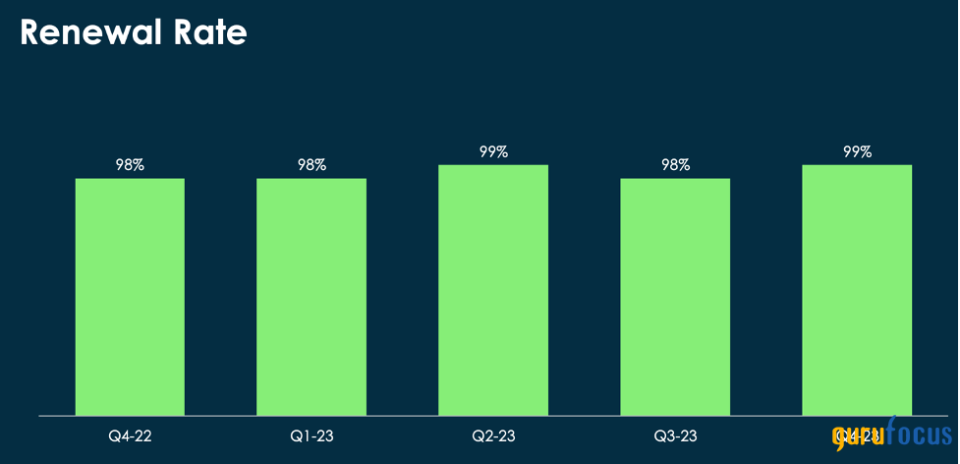

In the past five quarters, ServiceNow has maintained an extremely high renewal rate of 98% to 99%. These consistently impressive renewal rates show that customers find significant value and satisfaction in the company's products. Its ability to retain customers at such a high rate also suggests its products are deeply integrated into its clients' operations and have become essential to their business operations. When a product becomes an indispensable part of a client's operations, the cost of switching to competitors' products becomes extremely expensive. This situation leaves clients with no option but to continue using ServiceNow's products. As a result, I expect the company's renewal rate to be quite sustainable going forward.

Source: ServiceNow's presentation

Robust cash flow generation

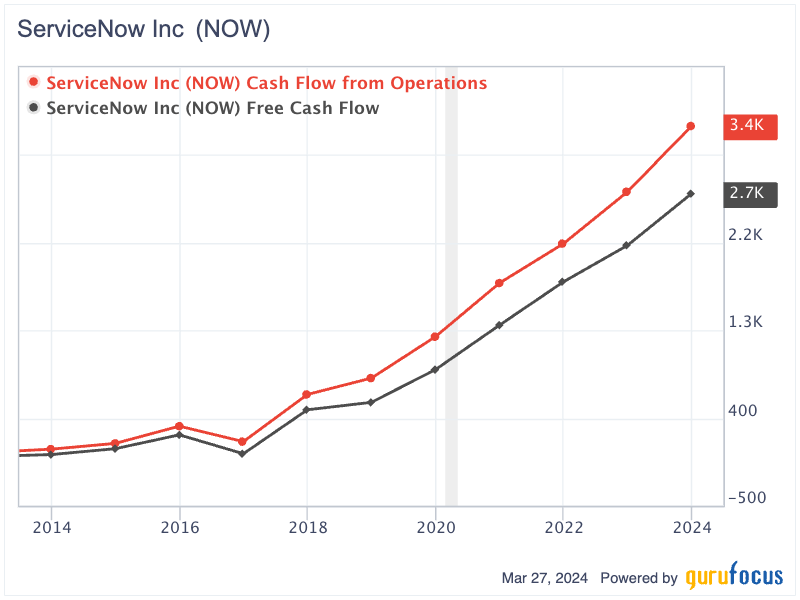

Over the past decade, ServiceNow has achieved significant growth in both operating cash flow and free cash flow. Its operating cash flow increased from $81.75 million in 2013 to $3.40 billion in 2023. The free cash flow followed a similar trend, growing from $26.43 million to $2.70 billion over the same period, translating to an annual compounded growth rate of 58.80%.

In 2023, the company generated $8.97 billion in sales and $2.70 billion in free cash flow, resulting in a robust free cash flow margin of 30%. The high free cash flow margin indicates the company could convert a substantial portion of revenue into cash, which can then be used for reinvestment in the business or distribution to shareholders.

Conservative balance sheet with strong cash position

ServiceNow has a strong balance sheet with a significant cash balance and minimal debt. As of December 2023, its shareholder's equity was $7.63 billion, while its cash and cash equivalents, along with short-term and long-term investments, amounted to $8.10 billion.

In contrast, the long-term debt was relatively low at $1.49 billion. Thus, the net cash position came in at around $6.61 billion. The debt-to-equity ratio was quite low at only 0.20. ServiceNow's solid balance sheet strength provides considerable financial flexibility, enabling it to seize growth opportunities and effectively deal with potential challenges.

Potential upside

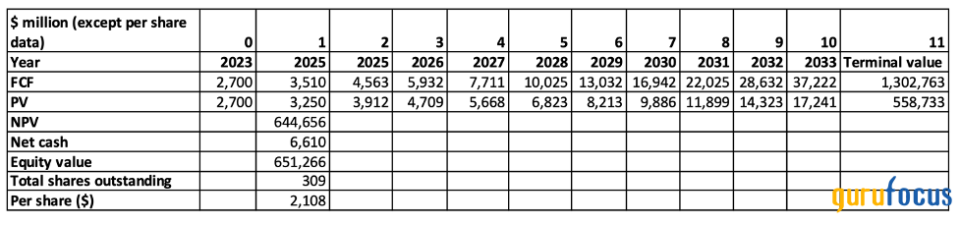

To calculate ServiceNow's intrinsic value using the discounted free cash flow model, we will assume free cash flow will grow by 30% annually for the next 10 years. After this period, the terminal growth rate will drop to 5%. Applying an 8% discount rate, the company's enterprise value is estimated to be around $644.70 billion. Accounting for the current net cash of $6.61 billion, its equity value is projected to be around $651.30 billion. Assuming the number of total shares outstanding increases by 50% to 309 million, ServiceNow's equity value per share will be approximately $2,100, which is 180% higher than its current share price.

Key takeaway

ServiceNow has been an exceptional stock, delivering high compounded annual returns for shareholders over the past 11 years. The company's success has been built on strong revenue growth, significant customer retention, a solid balance sheet and robust cash flow generation.

My discounted free cash flow analysis indicates the company still has significant upside potential, offering great opportunities to long-term growth investors. Although its share price might experience volatility in the short run, ServiceNow could keep delivering decent returns to its shareholders over the long term.

This article first appeared on GuruFocus.