Yahoo Finance

Yahoo Finance eBay Earnings After The Bell: Can The Rally Continue?

America’s second-favorite online shopping site is reporting earnings after the bell today. eBay EBAY analysts are estimating robust growth for Q2, an earnings seasons that is expected to see year-over-year EPS depreciation. EBAY has displayed a sharp rally so far in 2019, surging 42.5% since January 1st, far outperforming the e-commerce sector. Analysts have been increasing long term earnings estimates over the past 60, propelling EBAY into a Zacks Rank #1 (Strong Buy).

Earnings Expectations

eBay analysts are estimating an EPS of $0.49 and sales of $2.67 billion, which would represent 17% and 1.3% year-over-year growth respectively. EBAY is a big mover on earnings with an average change of 7.5% over the past 6 earnings reports. The average EPS surprise is an 8.9% beat.

Company Performance

International sales are eBay’s primary driver, making up 60% of their top-line. Global revenue is the fastest-growing side of the business and is expected to be the company’s key growth driver moving forward. Having a hefty amount of international exposure is a double edged-sword for eBay.

80% of the world’s e-commerce sales are abroad, with strong growth expectations. An expanding number of people gaining access to internet and becoming comfortable with online shopping will grow the total accessible market. eBay has mounting access to this fast-growing market, but this exposure also makes it susceptible to slowing global economies.

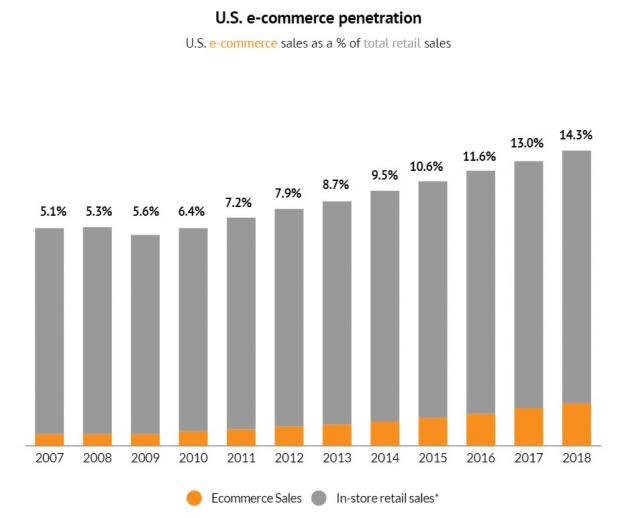

E-commerce has been swallowing a progressively larger share of the US’s total retail every year. This space has grown stable double-digit percentages for almost a decade now making up 14.3% of the retail market in the US, according to Digital Commerce 360 (providing the graphic below).

If eBay is able to maintain its market share (currently 6.1% of US market), it should be able to ride this momentous e-commerce wave and reap the benefits of its prolific retail takeover. This overly competitive space is making it difficult for eBay to experience the same growth as top competitors Amazon AMZN and Walmart WMT who have both been able to grow their e-com segments faster than the category.

eBay has been unable to keep up with the rest of the e-commerce market in recent year. The firm has been running into issues with Google’s GOOGL new search algorithm, which has had a significant negative impact on the site’s traffic. eBay also lost some consumer faith after a devastating cyberattack in 2014. They have been able regained most of their core customers and have been growing the number of active buyers by 4% year-over-year for the past 5 quarters.

eBay currently has 180 million active buyers and are expected to add 1 million in Q2, with these figures being reported this afternoon in the earnings report.

Activist Investors

Elliot Management, an activist investment group, recently took a 4% position in EBAY and are attempting to make systemic changes from within that investors appear to be pleased with. At the end of January, Elliot management sent a letter to management expressing their conviction that eBay would benefit from selling StubHub and its Classifieds group to focusing on core competencies. This news of potential reform sent the stock soaring.

Take Away

EBAY is trading at a 17.7x 12-month forward P/E, right in the middle of its 5-year range (10.2x – 25.4x) and far below the e-commerce P/E average of 41x. This is primarily due to its low growth expectations. When factoring growth into the valuation using PEG, EBAY’s multiple falls right in line with the rest of the industry.

Expect this stock to move one way or the other on this earnings report. Management guidance and sentiment on future performance is going to be a vital driver of a potential move, along with any significant variance from EPS or sales estimates.

The e-com category is slowly taking over consumer spending. The question is, can eBay keep up with the pack? Earnings this afternoon will give us a glimpse.

Today's Best Stocks from Zacks

Would you like to see the updated picks from our best market-beating strategies? From 2017 through 2018, while the S&P 500 gained +15.8%, five of our screens returned +38.0%, +61.3%, +61.6%, +68.1%, and +98.3%.

This outperformance has not just been a recent phenomenon. From 2000 – 2018, while the S&P averaged +4.8% per year, our top strategies averaged up to +56.2% per year.

See their latest picks free >>

Click to get this free report eBay Inc. (EBAY) : Free Stock Analysis Report Amazon.com, Inc. (AMZN) : Free Stock Analysis Report Alphabet Inc. (GOOGL) : Free Stock Analysis Report Walmart Inc. (WMT) : Free Stock Analysis Report To read this article on Zacks.com click here. Zacks Investment Research