Yahoo Finance

Yahoo Finance Does Posera (TSE:PAY) Have A Healthy Balance Sheet?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Posera Ltd. (TSE:PAY) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Posera

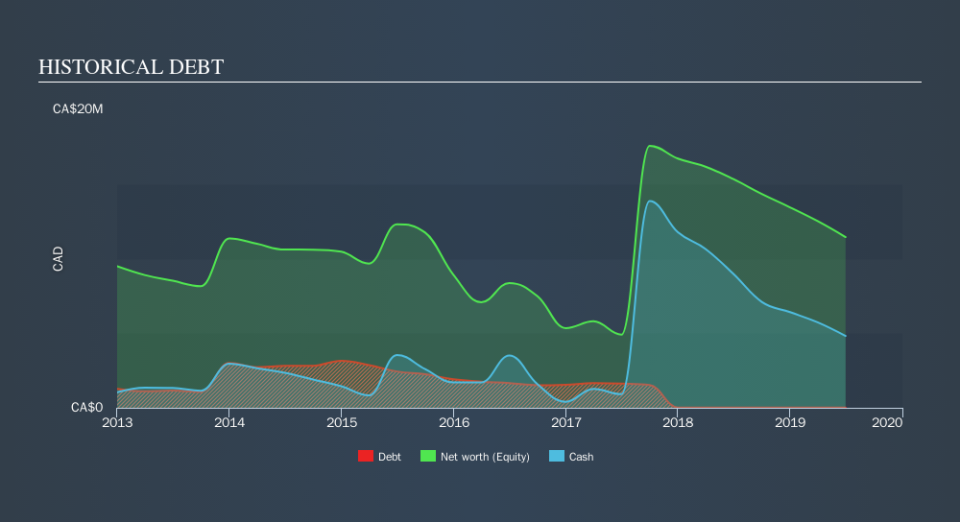

What Is Posera's Net Debt?

As you can see below, Posera had CA$11.1k of debt at June 2019, down from CA$17.9k a year prior. However, it does have CA$4.81m in cash offsetting this, leading to net cash of CA$4.80m.

How Healthy Is Posera's Balance Sheet?

We can see from the most recent balance sheet that Posera had liabilities of CA$2.50m falling due within a year, and liabilities of CA$192.7k due beyond that. Offsetting this, it had CA$4.81m in cash and CA$3.10m in receivables that were due within 12 months. So it actually has CA$5.23m more liquid assets than total liabilities.

This luscious liquidity implies that Posera's balance sheet is sturdy like a giant sequoia tree. With this in mind one could posit that its balance sheet is as strong as beautiful a rare rhino. Simply put, the fact that Posera has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is Posera's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Posera had negative earnings before interest and tax, and actually shrunk its revenue by 17%, to CA$8.9m. That's not what we would hope to see.

So How Risky Is Posera?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months Posera lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of CA$2.8m and booked a CA$3.9m accounting loss. But at least it has CA$4.80m on the balance sheet to spend on growth, near-term. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. For riskier companies like Posera I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.