Yahoo Finance

Yahoo Finance Does Peyto Exploration & Development (TSE:PEY) Have A Healthy Balance Sheet?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Peyto Exploration & Development Corp. (TSE:PEY) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Peyto Exploration & Development

What Is Peyto Exploration & Development's Debt?

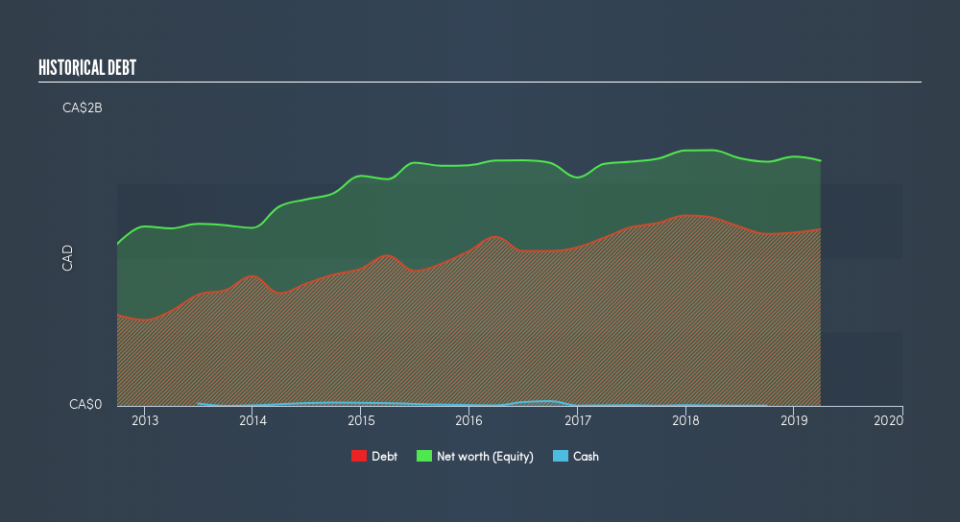

The image below, which you can click on for greater detail, shows that Peyto Exploration & Development had debt of CA$1.19b at the end of March 2019, a reduction from CA$1.27b over a year. Net debt is about the same, since the it doesn't have much cash.

How Strong Is Peyto Exploration & Development's Balance Sheet?

According to the last reported balance sheet, Peyto Exploration & Development had liabilities of CA$77.1m due within 12 months, and liabilities of CA$1.92b due beyond 12 months. On the other hand, it had cash of CA$998.0k and CA$68.1m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CA$1.93b.

This deficit casts a shadow over the CA$659.5m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt After all, Peyto Exploration & Development would likely require a major re-capitalisation if it had to pay its creditors today.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Peyto Exploration & Development's debt is 2.5 times its EBITDA, and its EBIT cover its interest expense 3.8 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Shareholders should be aware that Peyto Exploration & Development's EBIT was down 34% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Peyto Exploration & Development's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Looking at the most recent three years, Peyto Exploration & Development recorded free cash flow of 49% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

On the face of it, Peyto Exploration & Development's EBIT growth rate left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability to convert EBIT to free cash flow isn't such a worry. After considering the datapoints discussed, we think Peyto Exploration & Development has too much debt. While some investors love that sort of risky play, it's certainly not our cup of tea. Given our concerns about Peyto Exploration & Development's debt levels, it seems only prudent to check if insiders have been ditching the stock.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.