Yahoo Finance

Yahoo Finance What’s the difference between a defined benefit and defined contribution pension plan?

By Julie Cazzin with Allan Norman

Q: I know that a lot of workers who change jobs go from defined-benefit (DB) pension plans to defined-contribution (DC) pension plans at their place of work. How can I figure out how much money I’ll really end up with in retirement? And what are the pros and cons of each of these plans? — Antonio

FP Answers: No question, Antonio, changing jobs and switching between defined-benefit and defined-contribution plans make it challenging to determine future retirement income. Both plans are good, but quite different, and each plan has its own variations. Knowing the pros and cons of each, and how to use them in conjunction with each other, will help better prepare you for retirement.

The main differences between the plans relate to investment management, control and retirement-income delivery. DB investment management is done without any input from pension members. As a result, it is the pension sponsor, the employer, that assumes all the investment risk.

At retirement, the pension sponsor is required to pay pensioners a fixed income for life, based on a published formula, no matter the investment performance. There is little to no investment risk or longevity risk (outliving your money) to the pensioner, assuming the pension sponsor remains solvent throughout a pensioner’s life.

With a DC plan, the employee makes investment decisions based on a fixed set of investment options within the plan. This is very similar to registered retirement savings plan (RRSP) investing, but with less investment choice. A pensioner’s retirement income is based on expected life expectancy and investment performance leading up to and in retirement.

If you have both a DB and a DC plan, the combination may impact your DC plan asset allocation decisions. Some may consider their DB plan as the fixed-income portion of their portfolio and hold a higher-than-normal equity portion in their DC plan than if they only had a DC plan.

When it comes to control, a pensioner with a DB plan has none. You can’t go to the pension board when it’s time for a new car and ask for more money. You’re not going to get it. With a DC plan, additional income can be drawn from the plan once it is converted to a life income fund (LIF), like the way a RRSP is converted to a registered retirement income fund (RRIF).

Unlike a RRIF, a LIF is subject to maximum withdrawals and the total amount that can be withdrawn from a DC plan converted to a LIF will depend on the provincial or federal unlocking rules the plan is registered in.

Having a fixed DB and flexible DC plan provides income options. For example, if the DB plan combined with Canada Pension Plan (CPP) and Old Age Security (OAS) is enough to cover basic needs, an option is available to draw down on the DC plan earlier in retirement. In this way, you create an income stream following the go-go, slow-go and no-go retirement years.

Upon the death of a pensioner, the surviving partner or spouse will receive a reduced pension if the option was not waived. In most cases, children will not inherit money from a DB plan. The total value of a DC plan will transfer to the named beneficiary and the estate of the pensioner will pay the tax owing if the beneficiary is not a spouse or partner.

An overlooked consideration of DB and DC plans is retirement-income delivery.

DB plans deposit a fixed income into a pensioner’s bank account as long as they live. Knowing they have an endless income stream means they can comfortably spend and enjoy their money. Pensioners with a DC plan often worry about running out of money and poor investment returns. From my observations, they spend less than they would if the money was coming from a DB plan.

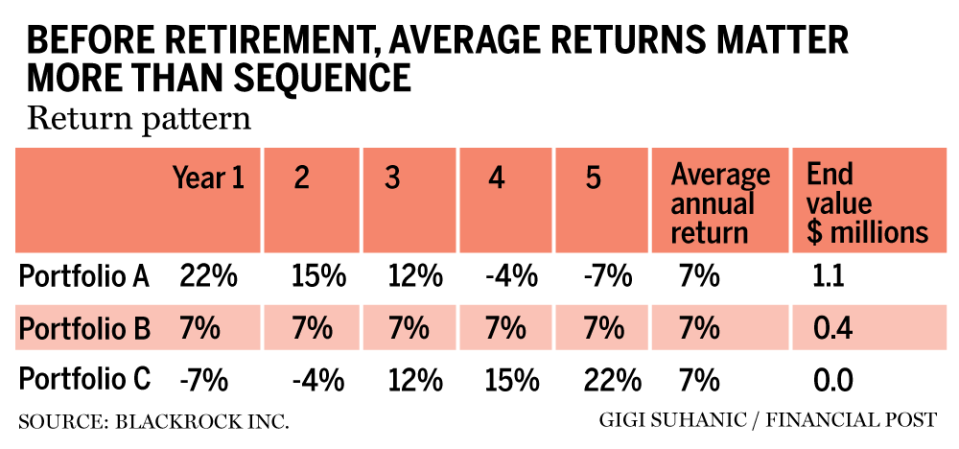

The bigger risk with a DC plan is sequence-of-return risk, which is illustrated in the accompanying table using BlackRock Inc. data.

Over the course of 25 years, the average annual return of each investment portfolio was seven per cent, not considering withdrawals. Many people have told me, ‘If I can earn seven per cent, I can draw $70,000 per year and still have $1 million.’ It doesn’t work that way. Safely drawing money from an investment portfolio is a lot more difficult than investing and accumulating money. The DB plan has the advantage here.

There are several more differences and pros and cons with DB and DC plans. I believe the ones I’ve covered are the big ones. In the end, both plans will help you prepare for retirement, but note the type of pension offered when you switch jobs since you may prefer one type over the other.

Allan Norman provides fee-only certified financial planning services through Atlantis Financial Inc. and provides investment advisory services through Aligned Capital Partners Inc. (ACPI). ACPI is regulated by the Canadian Investment Regulatory Organization ciro.ca Allan can be reached at alnorman@atlantisfinancial.ca