Yahoo Finance

Yahoo Finance Diana Shipping (NYSE:DSX) Is Due To Pay A Dividend Of $0.075

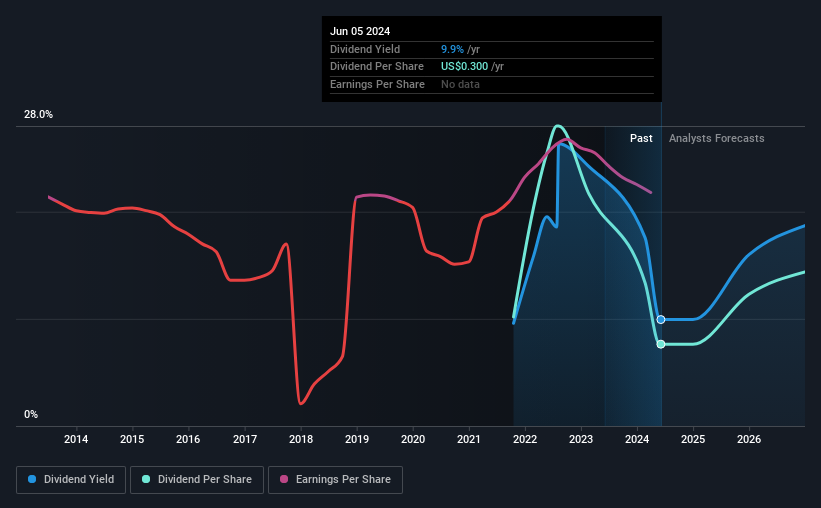

The board of Diana Shipping Inc. (NYSE:DSX) has announced that it will pay a dividend on the 18th of June, with investors receiving $0.075 per share. However, the dividend yield of 9.9% still remains in a typical range for the industry.

View our latest analysis for Diana Shipping

Diana Shipping's Payment Has Solid Earnings Coverage

We like a dividend to be consistent over the long term, so checking whether it is sustainable is important. Based on the last payment, the dividend made up 88% of cash flows, but a higher proportion of net income. While the cash payout ratio isn't necessarily a cause for concern, the company is probably focusing more on returning cash to shareholders than growing the business.

Looking forward, earnings per share is forecast to rise exponentially over the next year. Assuming the dividend continues along recent trends, we estimate that the payout ratio could reach 70%, which is in a comfortable range for us.

Diana Shipping's Dividend Has Lacked Consistency

Even in its short history, we have seen the dividend cut. Since 2021, the annual payment back then was $0.40, compared to the most recent full-year payment of $0.30. Doing the maths, this is a decline of about 9.1% per year. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

The Dividend's Growth Prospects Are Limited

Dividends have been going in the wrong direction, so we definitely want to see a different trend in the earnings per share. Earnings per share has been crawling upwards at 4.9% per year. The company is paying out a lot of its profits, even though it is growing those profits pretty slowly. As they say in finance, 'past performance is not indicative of future performance', but we are not confident a company with limited earnings growth and a high payout ratio will be a star dividend-payer over the next decade.

An additional note is that the company has been raising capital by issuing stock equal to 15% of shares outstanding in the last 12 months. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

The Dividend Could Prove To Be Unreliable

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. The track record isn't great, and the payments are a bit high to be considered sustainable. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. To that end, Diana Shipping has 5 warning signs (and 1 which can't be ignored) we think you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.