Yahoo Finance

Yahoo Finance Despite the banking turmoil, it doesn't look like there's a lending crisis

A version of this post first appeared on TKer.co

Stocks closed modestly lower last week with the S&P 500 shedding 0.3%. The index is now up 7.4% year to date, up 15.2% from its October 12 closing low of 3,577.03, and down 14% from its January 3, 2022 record closing high of 4,796.56.

In the wake of the failure of Silicon Valley Bank in March, turmoil in the banking sector persists. And because bank lending is so critical to economic activity, all eyes have been on lending data.

Early data released in April was less than great.

Another month later, the data is arguably not as disastrous as it was feared to be.

Before we get to the new data, let’s remember that the Federal Reserve has been actively working to cool the economy with tighter financial conditions. That means lending activity has already been tightening and further tightening was to be expected.

To an extent, challenges in the banking system help the Fed achieve its goals if it means consumers and businesses have a more difficult time getting financing from banks. Same destination, but a more treacherous path.

The emerging concern was that bank turmoil would cause an extraordinary drop in lending as banks substantially tightened their purse strings beyond what the Fed was aiming for. Fortunately, the data doesn’t yet support this more worrisome outcome.

It doesn’t look like a bank crisis 🤷🏻♂️

As expected, banks reined in lending a bit during the first three months of the year amid the Fed’s crusade against inflation.

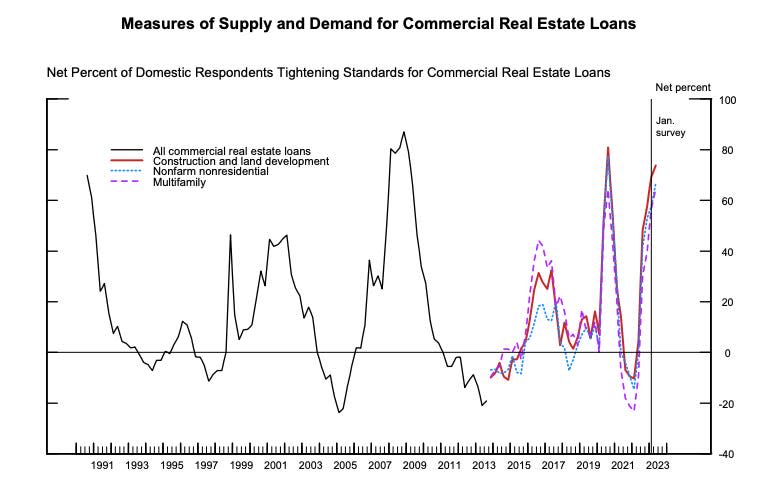

According to the Federal Reserve’s April Senior Loan Officer Opinion Survey (via Notes), lenders tightened standards for commercial and industrial loans…

…commercial real estate loans…

…residential mortgage loans…

…and consumer loans.

Sure, banks continued to tighten since the previous SLOOS report. But the magnitude of the change does not appear to reflect the kind of deterioration you might expect from a banking crisis.

"The April Senior Loan Officer Opinion Survey (SLOOS), in our view, does not suggest bank behavior changed markedly after the emergence of regional bank stress earlier this year," Bank of America economists wrote on Monday.

It won’t be until August that we get the SLOOS report covering the second quarter.

But the New York Fed’s April Survey of Consumer Expectations (via Notes) suggests lending hasn’t yet become a crisis for borrowers. From the report released Monday: “Perceptions of credit access compared to a year ago were mixed in April. Both the share of households reporting it is easier and the share reporting it is harder to obtain credit now than one year ago declined. Similarly, respondents’ views about future credit availability were mixed. Both the share of respondents expecting harder and the share expecting easier credit conditions a year from now declined."

Sure, the New York Fed characterized the results as "mixed." But the bottom line, again, is that it does not look like a banking crisis.

This sentiment was also confirmed in the NFIB’s Small Business Optimism Index (via Notes).

As you can see in the chart below, the net percent of small business owners saying they expect easier credit conditions has been trending unfavorably for a few months, which you’d expect from tighter monetary policy.

But if you look very closely, you’ll see that responses to this question actually improved modestly, ticking up to -9% in April from -8% in March.

(Source: NFIB)

To be clear, the sentiment towards credit conditions continues to be pretty sour. BUT again, they do not appear to reflect systemic banking problems.

"While owners are becoming more pessimistic, April's report should help allay concerns that credit is becoming completely unaccessible for small businesses," Wells Fargo economists said on Tuesday.

Furthermore, here’s a fascinating regional stat: BofA (via Notes) found "that San Francisco and New York, the headquarters of the three failed domestic banks, outpaced the other major metros in terms of retail ex-auto spending in both March and April."

So while consumer spending may be cooling, it doesn’t appear any worse in the regions that would be most directly affected by the banking turmoil.

The bottom line 🤔

We still see headlines every once in a while about some regional banking potentially facing problems. But as I wrote back in March, banks fail. This is not new.

And while metrics related to lending don’t look great, there’s not much to suggest financial instability in banking has evolved into a systemic problem.

Even if there is a material impact lending as a result of recent banking turmoil, it may ironically be a development that policymakers embrace.

"Fed officials may actually welcome this news since tighter bank credit should slow the economy and bring inflation down," Ed Yardeni, president of Yardeni Research, wrote on Tuesday.

Reviewing the macro crosscurrents 🔀

There were a few notable data points and macroeconomic developments from last week to consider:

🤷🏻♂️ Perception < Reality. Consumer sentiment fell in May, according to University of Michigan survey data. But the report’s researchers made an interesting observation: "While current incoming macroeconomic data show no sign of recession, consumers’ worries about the economy escalated in May alongside the proliferation of negative news about the economy, including the debt crisis standoff."

In other words, the economy is actually in good shape but the news is giving consumers the perception that things are bad.

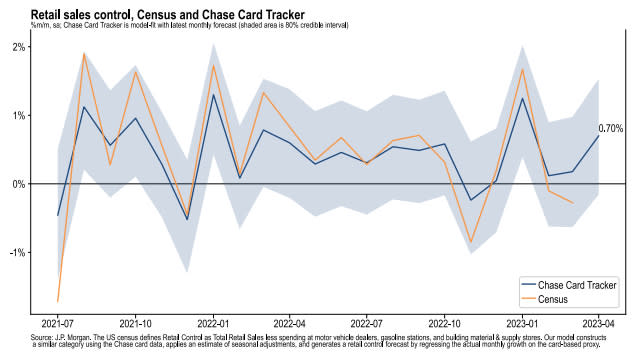

🛍️ Speaking of reality, spending is holding up. Here’s Bob Elliot of Unlimited Funds: "Timely BEA credit card spend data for April still pointing to a recovery from the weakness in March. If folks are betting on recession now because of demand, it doesn't look like it’s playing out in reality."

JPMorgan, citing their internal card spending data, also estimates retail sales are growing. From their May 12 report: "Based on the Chase Consumer Card data through 08 May 2023, our estimate of the U.S. Census April control measure of retail sales m/m is 0.70%."

💵 Consumers still have excess savings. From the San Francisco Fed (via Notes): "We show that households rapidly accumulated unprecedented levels of excess savings—defined as the difference between actual savings and the pre-recession trend—relative to previous recessions.

Moreover, despite a rapid drawdown of savings in recent months, there is still a large stock of aggregate excess savings in the economy—some $500 billion. The distribution and allocation of excess savings and wealth across the income distribution suggest that households on average, including those at the lower end of the distribution, continue to have considerably more liquid funds at their disposal compared with the pre-pandemic period."

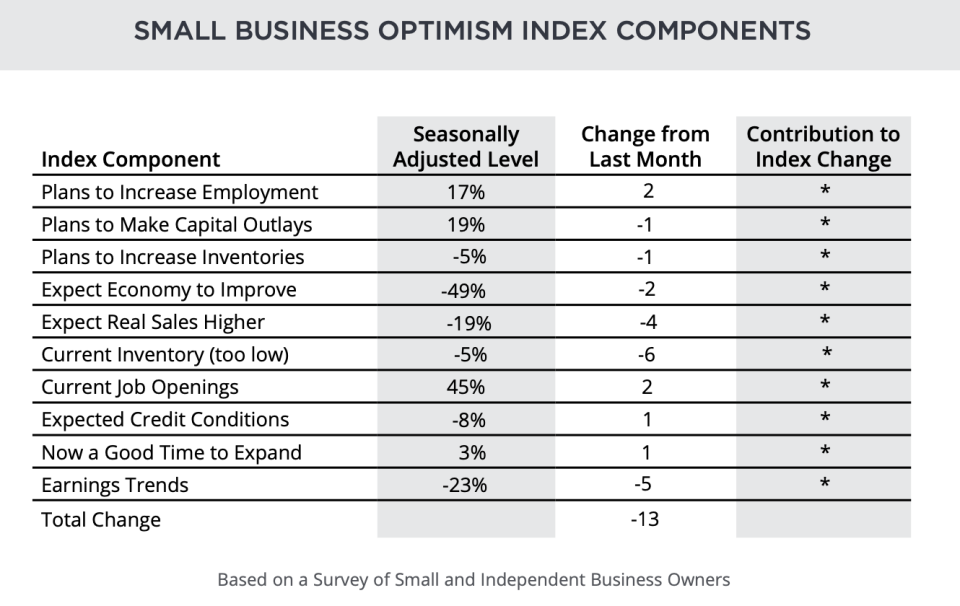

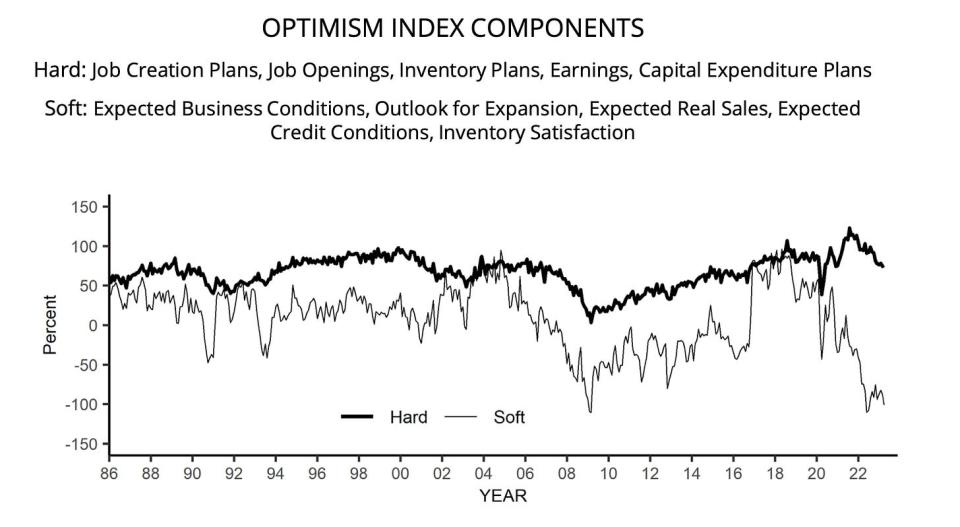

🤨 Small business sentiment deteriorates. The NFIB’s Small Business Optimism Index (via Notes) deteriorated to a 13-year low in April.

(Source: NFIB)

But… Some of the underlying components of the index were encouraging: Plans to increase employment improved, current job openings improved, expected credit conditions were less bad, and more businesses agreed that "now is a good time to expand."

(Source: NFIB)

As the NFIB shows, the more tangible "hard" components of the index have held up much better than the more sentiment-oriented "soft" components.

(Source: NFIB)

Keep in mind that during times of stress, soft data tends to be more exaggerated than actual hard data.

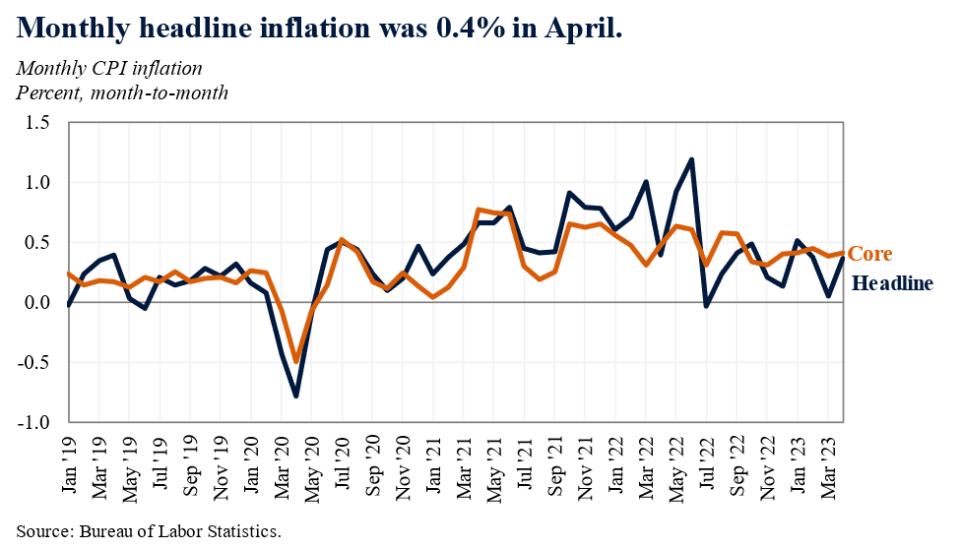

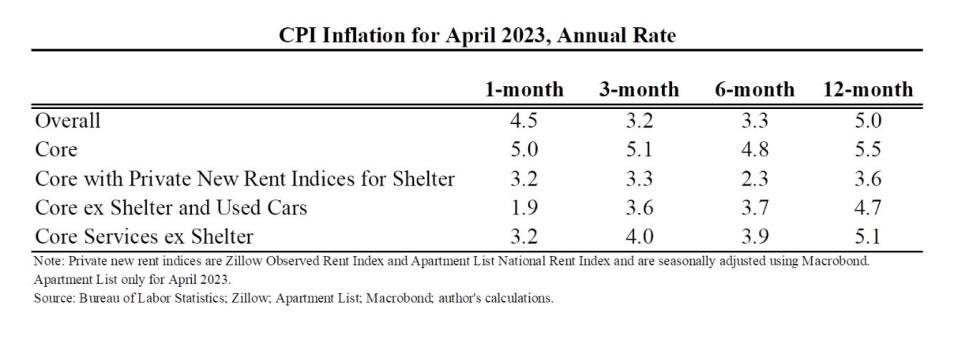

🎈 Inflation continues to cool. The Consumer Price Index (CPI) in April was up 4.9% from a year ago, down from 5.0% in March. It was the 10th straight month of decline, and it was the first reading below 5% since April 2021. Excluding food and energy prices, core CPI was up 5.5% from a year ago.

On a month-over-month basis, CPI was up 0.4% as food prices were flat during the period. Core CPI was up 0.4%, down from 0.5% the month prior.

If you annualize the three-month trend in the monthly figures, CPI is rising at a 3.2% rate and core CPI is climbing at a 5.1% rate.

The bottom line is that while inflation rates have been trending lower, they continue to be above the Federal Reserve’s target rate of 2%.

👍 Relief in key categories. Regarding the details of the CPI report, Renaissance Macro Research noted: "U.S. households are seeing relief in grocery and utility bills. Over the last three months, food at home CPI fell 0.2% while energy services have declined 5.6%. Welcome news. Aggregate real incomes are climbing."

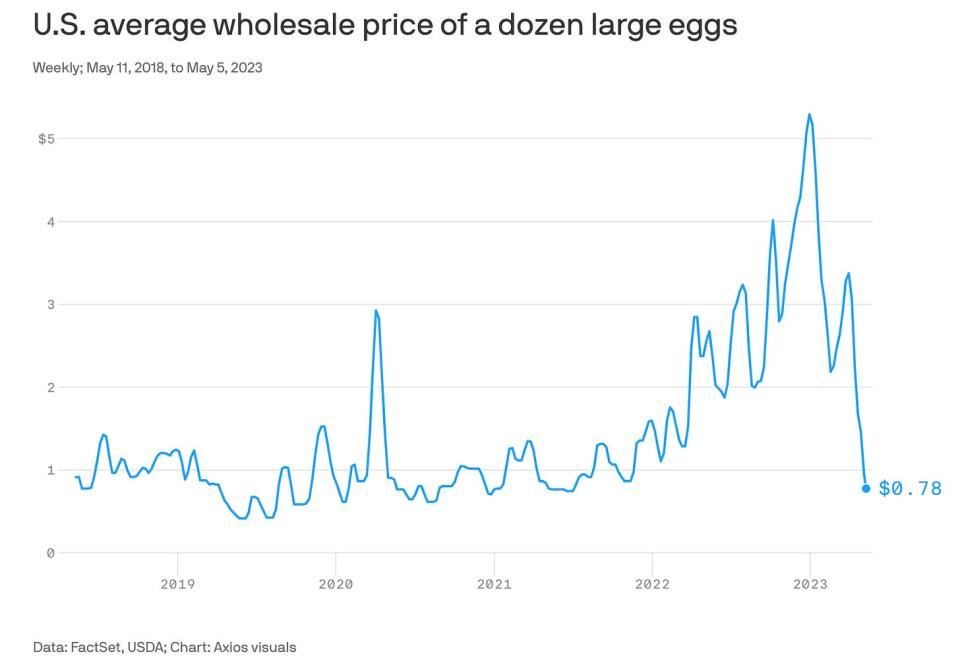

In case you were wondering about egg prices, which spiked late last year, they’re down. From Axios: "The latest weekly egg report from the U.S. Department of Agriculture shows a sharp drop in the wholesale prices retailers are paying for eggs. They fell to roughly 78 cents per dozen in the first week of May, from a peak of about $5.30 at the end of last year."

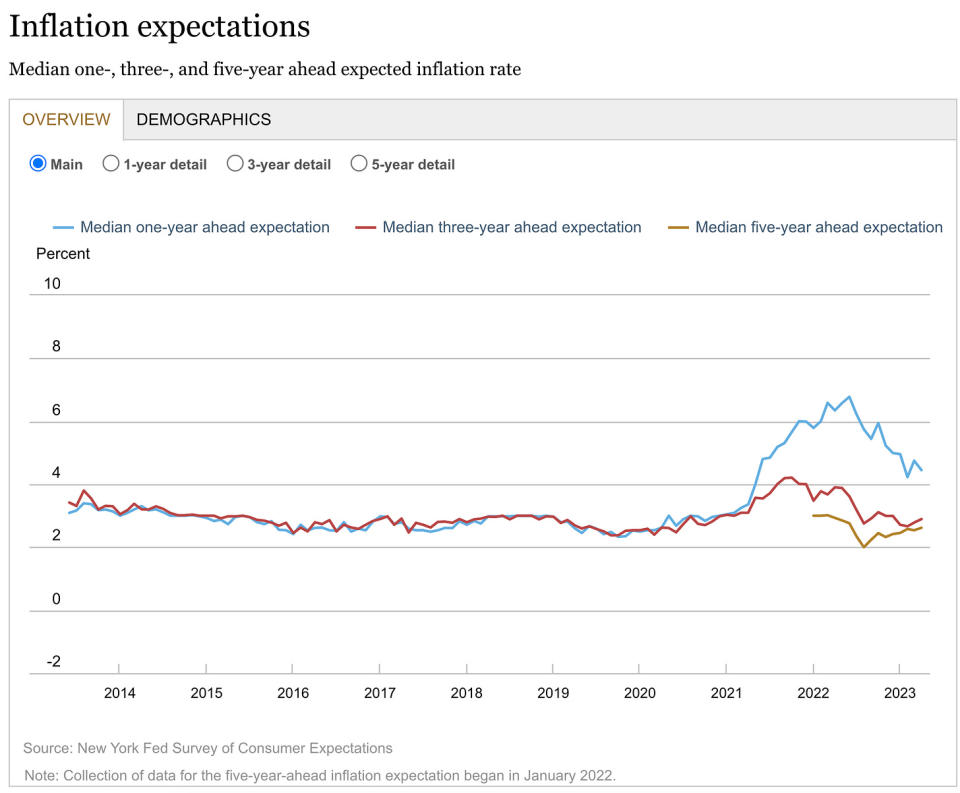

🤷🏻♂️ Consumers’ outlook for inflation is mixed. From the New York Fed’s April Survey of Consumer Expectations: "Median inflation expectations declined by 0.3 percentage point at the one-year-ahead horizon to 4.4%, but increased by 0.1 percentage point at the three- and five-year-ahead horizons to 2.9% and 2.6%, respectively."

The University of Michigan’s consumer sentiment survey showed similar results: "Year-ahead inflation expectations receded slightly to 4.5% in May after spiking to 4.6% in April. After two years of relative stability, long-run inflation expectations rose to their highest reading since 2011, lifting from 3.0% last month to 3.2% this month."

📈 Inventory levels are up. According to Census Bureau data released Monday, wholesale inventories stood at $918.5 billion in March. The inventories/sales ratio was 1.40, up significantly from 1.25 the previous year.

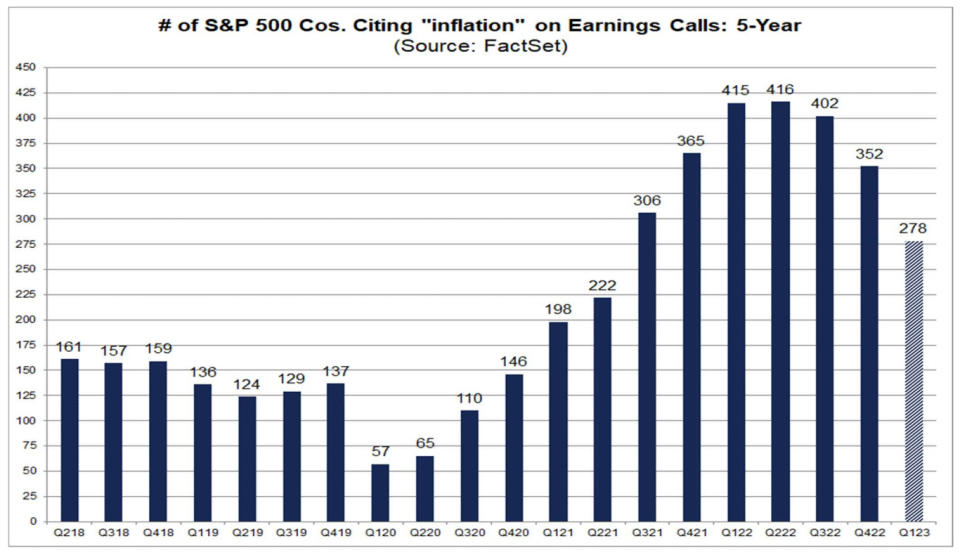

🤷🏻♂️ Fewer are talking about inflation. From FactSet: "FactSet searched for the term ‘inflation’ in the conference call transcripts of all the S&P 500 companies that conducted earnings conference calls from March 15 through May 11. Of these companies, 278 have cited the term ‘inflation’ during their earnings calls for the first quarter. This number is above the 5-year average of 211 and above the 10-year average of 163.

However, it should be noted that this is the lowest number of S&P 500 companies citing ‘inflation’ on earnings calls going back to Q2 2021 at 222 (using current constituents and going back in time). It also marks the third consecutive quarter in which the number of S&P 500 companies citing the term 'inflation' has declined quarter-over-quarter. There are still about 40 S&P 500 companies that have not reported actual earnings for the first quarter. So while the final number will likely finish higher than 278, it will fall short of the 352 from the previous quarter."

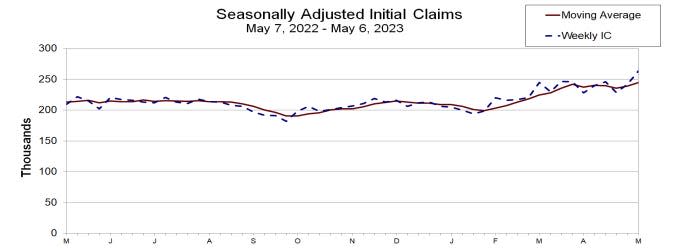

⚠️ Ignore this week’s unemployment claims. Initial claims for unemployment benefits climbed to 264,000 during the week ending May 6, up from 242,000 the week prior. While the number remains near levels seen during periods of economic expansion, it has been creeping higher.

However, an extraordinary spike in Massachusetts accounted for much of the increase. And Bloomberg reports that this was due largely to fraudulent attempts at gaining unemployment benefits.

No one’s really refuting the claim that the labor market has been cooling. But there’s little evidence to suggest that it’s deteriorating at the pace last week’s unemployment claims figure would suggest.

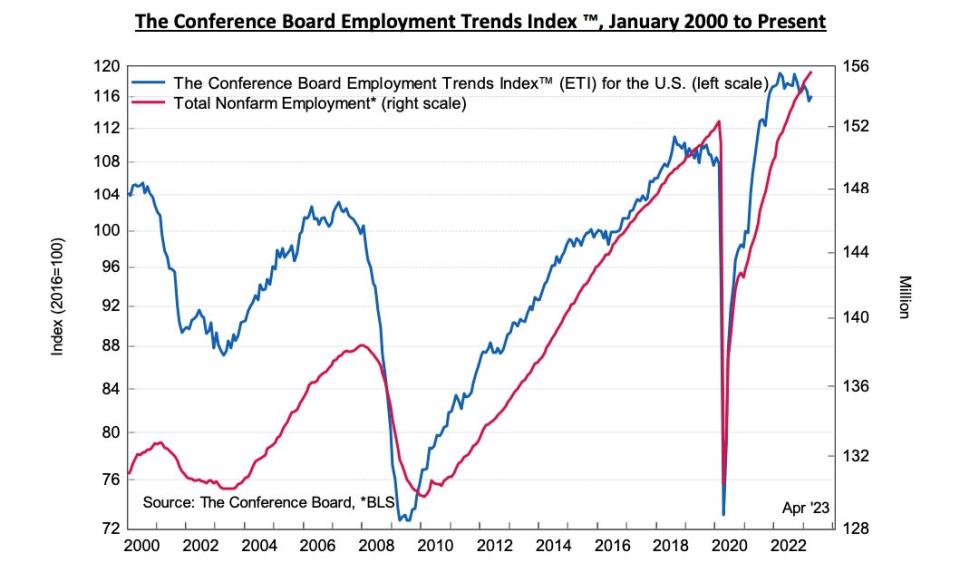

👍 Signs point to more job gains. According to The Conference Board (via TKer), the firm’s Employment Trends Index improved in April and continues to trend at levels showing "job gains will likely continue, albeit somewhat slower, over the next few months."

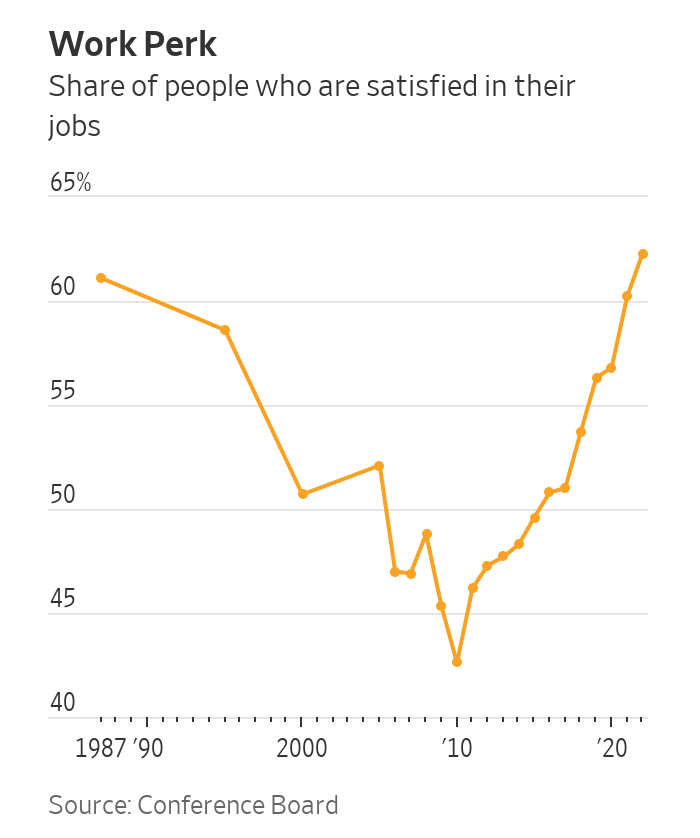

👍 People are happy with their jobs. From the Wall Street Journal: "Job satisfaction hit a 36-year high in 2022, reflecting two effects of the tight pandemic labor market: The quality of jobs improved as wages and work flexibility increased, and workers moved into positions that were a better fit. Last year, 62.3% of U.S. workers said they were satisfied with their jobs, according to new data from the Conference Board, up from 60.2% in 2021 and 56.8% in 2020. The business-research organization polled workers on 26 aspects of work, and found that people were most content with their commutes, their co-workers, the physical environment of their workplace and job security."

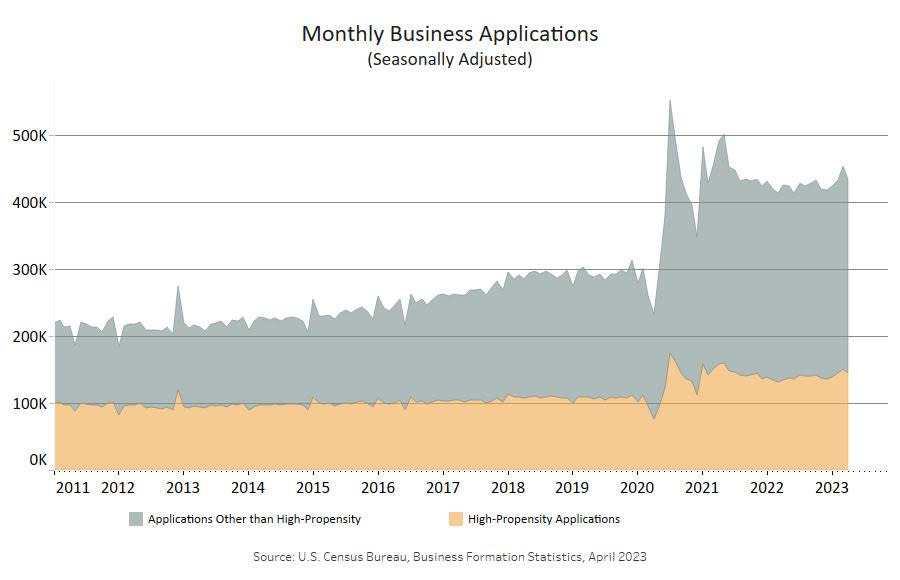

🍾 The entrepreneurial spirit is alive. From the Census Bureau: "Total Business Applications in April 2023 were 433,894, down 4.2% (seasonally adjusted) from March 2023." Even with the decline, business applications are trending well above pre-pandemic levels.

👍 Executives see growth through 2023. From the ISM (via Notes): "The U.S. economy will continue to softly expand for the rest of 2023, say the nation's purchasing and supply executives in the Spring 2023 Semiannual Economic Forecast."

Putting it all together 🤔

Despite recent banking tumult, we continue to get evidence that we could see a bullish "Goldilocks" soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession.

The Federal Reserve recently adopted a less hawkish tone, acknowledging on February 1 that "for the first time that the disinflationary process has started." And on May 3, the Fed signaled that the end of interest rate hikes may be here.

In any case, inflation still has to come down more before the Fed is comfortable with price levels. So we should expect the central bank to keep monetary policy tight, which means we should be prepared for tight financial conditions (e.g. higher interest rates, tighter lending standards, and lower stock valuations) to linger.

All of this means the market beatings may continue for the time being, and the risk the economy sinks into a recession will be relatively elevated.

At the same time, it’s important to remember that while recession risks are elevated, consumers are coming from a very strong financial position. Unemployed people are getting jobs. Those with jobs are getting raises. And many still have excess savings to tap into. Indeed, strong spending data confirms this financial resilience. So it’s too early to sound the alarm from a consumption perspective.

At this point, any downturn is unlikely to turn into economic calamity given that the financial health of consumers and businesses remains very strong.

And as always, long-term investors should remember that recessions and bear markets are just part of the deal when you enter the stock market with the aim of generating long-term returns. While markets have had a pretty rough couple of years, the long-run outlook for stocks remains positive.