Yahoo Finance

Yahoo Finance With Dätwyler Holding AG (VTX:DAE) It Looks Like You'll Get What You Pay For

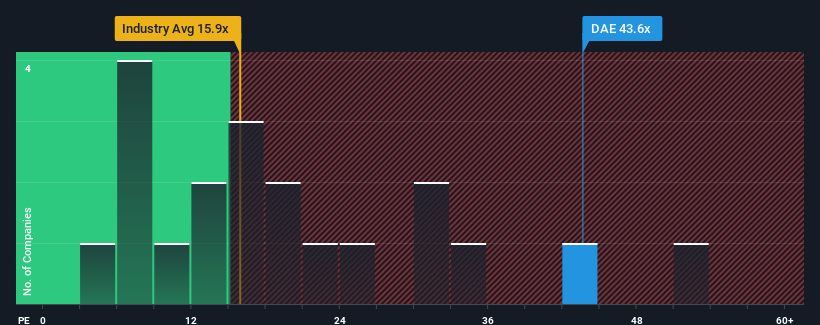

With a price-to-earnings (or "P/E") ratio of 43.6x Dätwyler Holding AG (VTX:DAE) may be sending very bearish signals at the moment, given that almost half of all companies in Switzerland have P/E ratios under 18x and even P/E's lower than 12x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Dätwyler Holding could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be extremely nervous about the viability of the share price.

See our latest analysis for Dätwyler Holding

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Dätwyler Holding.

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Dätwyler Holding's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 31% decrease to the company's bottom line. Regardless, EPS has managed to lift by a handy 11% in aggregate from three years ago, thanks to the earlier period of growth. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 24% per annum during the coming three years according to the seven analysts following the company. With the market only predicted to deliver 8.7% per year, the company is positioned for a stronger earnings result.

In light of this, it's understandable that Dätwyler Holding's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Dätwyler Holding's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 2 warning signs for Dätwyler Holding that you should be aware of.

If you're unsure about the strength of Dätwyler Holding's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.