Yahoo Finance

Yahoo Finance Service Corporation (SCI) Gains From Cemetery Unit & Expansion

Service Corporation International SCI benefits from its growth strategies, such as expansion through acquisitions. Fairly stable demand for the company’s services and products has also been working well. The company’s Cemetery unit has been performing well. However, high general and administrative (G&A) expenses and soft Funeral segment revenues are deterrents.

Cemetery Revenues Rise

The deathcare products and services provider has been seeing a rise in Cemetery segment revenues for a while now. In the fourth quarter of 2023, consolidated Cemetery revenues came in at $482.6 million, up from $447.5 million reported in the year-ago quarter. Comparable cemetery revenues increased 7.7%. The upside was mainly caused by increased core revenues to the tune of $31.5.

Core revenues increased due to growth in total recognized preneed revenues, partially hurt by reduced atneed revenues. Comparable preneed cemetery sales production rose 9.4% due to continued strength in large sales activity, along with a higher core production sales average.

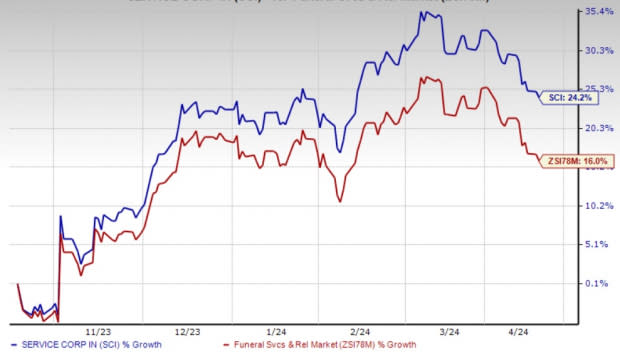

Image Source: Zacks Investment Research

Focus on Expansion

Service Corporation remains focused on making capital investments to strengthen its network. The company is investing in its current funeral locations, renovating and updating its venues to establish a more contemporary setup. Management is also elevating its cemetery inventory options with casketed as well as cremation consumers to house a diverse customer base.

During 2023, the company incurred capital expenditures of $631.8 million, which included increased cemetery development expenditures and digital investments, among others. On its fourth-quarter earnings call, management stated that its acquisition pipeline is solid. The company continues to increase market share opportunities through the construction of new funeral home facilities and the creation of new cemeteries in its existing high-growth areas.

Management expects total maintenance capital expenditures of $325 million for 2024, which includes investments in funeral and cemetery facilities, cemetery development projects, digital strategies and other corporate investments. Other than this, management intends to spend $75-$125 million on acquisitions during 2024.

Will Hurdles be Offset?

In the fourth quarter of 2023, G&A expenses amounted to nearly $45 million, exceeding the company’s expected range of $38-$40 million. The upside mainly resulted from increased incentive compensation expenses related to the company’s long-term compensation plans. The persistence of this factor could hurt margins.

Also, in the fourth quarter, consolidated Funeral revenues came in at $573.2 million, down from the $580.2 million reported in the year-ago period. This could be attributed to lower core revenues stemming from a decline in atneed revenues. Total comparable funeral revenues fell 2.2%, mainly due to a fall in core funeral revenues. Core funeral revenues decreased 2.1% due to a decline in core funeral services performed (resulting from lower pandemic-related activity). This was somewhat countered by growth in the core average revenue per service.

However, strong market strategies and the abovementioned upsides keep this Zacks Rank #3 (Hold) company well-placed for growth. In 2024, Service Corporation expects EPS, excluding special items, in the range of $3.50-$3.80 compared with $3.47 reported in 2023. That said, management anticipates a restoration to its typical earnings per share growth range of 8%-12% in 2025.

Shares of SCI have risen 24.2% in the past three months compared with the industry’s growth of 16%.

3 Solid Staple Bets

Vital Farms Inc. VITL offers a range of produced pasture-raised foods. It currently carries a Zacks Rank #2 (Buy). VITL has a trailing four-quarter average earnings surprise of 155.4%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Vital Farms’ current financial-year sales and earnings suggests growth of 18.7% and 30.5%, respectively, from the year-ago reported numbers.

Utz Brands Inc. UTZ manufactures a diverse portfolio of salty snacks and currently carries a Zacks Rank #2. UTZ has a trailing four-quarter earnings surprise of 2.6%, on average.

The Zacks Consensus Estimate for Utz Brands’ current financial-year earnings suggests growth of 19.3% from the year-ago reported numbers.

Celsius Holdings CELH, which offers functional drinks and liquid supplements, currently carries a Zacks Rank #2. CELH has a trailing four-quarter earnings surprise of 67.4%, on average.

The Zacks Consensus Estimate for Celsius Holdings’ current financial-year sales and earnings suggests growth of 41.6% each from the year-ago reported figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Service Corporation International (SCI) : Free Stock Analysis Report

Celsius Holdings Inc. (CELH) : Free Stock Analysis Report

Vital Farms, Inc. (VITL) : Free Stock Analysis Report

Utz Brands, Inc. (UTZ) : Free Stock Analysis Report