Yahoo Finance

Yahoo Finance China’s deflationary spiral is now entering dangerous new stage

(Bloomberg) — Deflation stalking China since last year is now showing signs of spiraling, threatening to worsen the outlook for the world’s second-largest economy and raising calls for immediate policy action.

Most Read from Bloomberg

Chicago Halts Hiring as Deficit Tops $1 Billion Through 2025

World's Second Tallest Tower Spurs Debate About Who Needs It

UC Berkeley Gives Transfer Students a Purpose-Built Home on Campus

The Plan for the World’s Most Ambitious Skyscraper Renovation

Data released Monday confirmed that apart from food costs, consumer price growth barely registered in large swathes of the economy at a time when incomes are sagging.

A broader measure of economy-wide prices known as the gross domestic product deflator will likely extend its current five-quarter drop into 2025, according to Bloomberg Economics and analysts at banks including BNP Paribas SA. That would amount to China’s longest streak of deflation since data began in 1993.

“We are definitely in deflation and probably going through the second stage of deflation,” said Robin Xing, chief China economist at Morgan Stanley, citing evidence from wage decreases. “Experience from Japan suggests that the longer deflation drags on, the more stimulus China will eventually need to break the debt-deflation challenge.”

The danger for China is deflation could snowball by encouraging households reeling from falling paychecks to cut back on spending, or delay purchases because they expect prices to fall further. Corporate revenues will suffer, stifling investment and leading to further salary cuts and layoffs, bankrupting families and firms.

Private surveys show that’s already starting to happen. In sectors of the economy favored by the government — such as electric vehicle-manufacturing and renewables — entry-level salaries declined by almost 10% in August from a peak in 2022, according to findings by Caixin Insight Group and Business Big Data Co.

A survey of 300 company executives by the Cheung Kong Graduate School of Business showed growth in labor costs last month was the weakest since April 2020, when China’s initial Covid lockdowns began to ease.

Separate data from Zhaopin Ltd. shows average hiring salaries in 38 major cities barely changed in the second quarter, in contrast to the 5% growth seen in the two years before the pandemic.

It’s a cycle the world has seen before in Japan starting in the 1990s during a period that came to be known as its “lost decades” — when a grinding stagnation followed a burst bubble in real estate and financial markets.

While Chinese officials have sought to stifle discussion about deflation, warning analysts to avoid using the term, it’s beginning to enter public dialogue. Former central bank Governor Yi Gang last week said rooting out deflation has to take priority for policymakers, a rare admission by a prominent figure in China that falling prices are threatening the outlook.

Yi called for “proactive fiscal policy and accommodative monetary policy” and said officials “should focus on fighting deflationary pressure,” at a panel discussion at the Bund Summit in Shanghai on Friday. China’s immediate goal should be to turn its GDP deflator positive in the coming quarters, he said.

So far, officials have given no sign of any significant shift from their cure-all of encouraging production rather than addressing weak demand with steps such as greater government spending on public services and consumer subsidies.

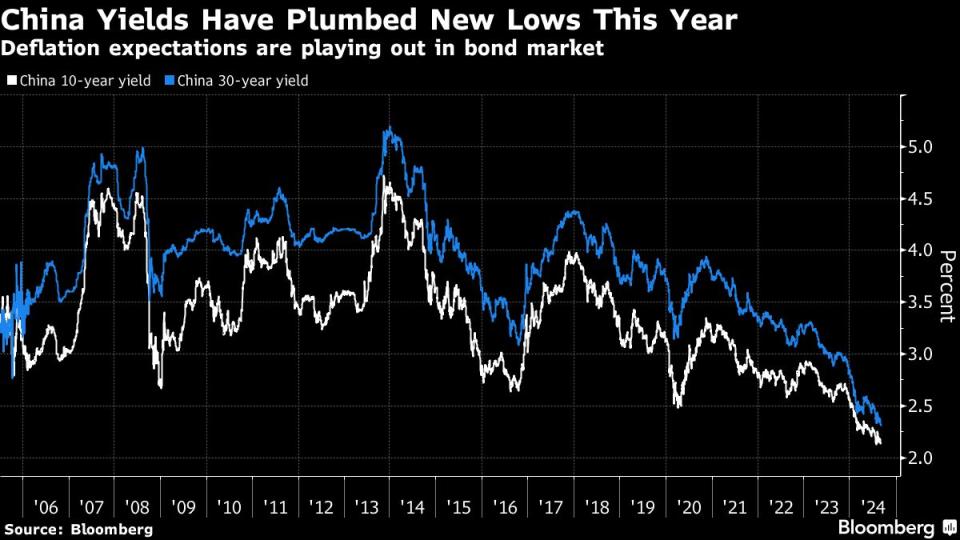

In a sign price pressures are becoming even more subdued, China’s core inflation — which strips out volatile items such as food and energy — cooled in August to the weakest in more than three years. Expectations for deflation are spilling into markets, stoking a bond rally that’s sent yields to record lows and stoked official concerns that banks have become too exposed to interest-rate risks.

The weak price pressures are evident in the growth pace of China’s nominal GDP, which expanded just 4% in the second quarter — well under the nation’s real economic growth goal of around 5% this year.

At times of weak price gains, nominal expansion is a more useful indicator because it better reflects changes in wages, profits and government revenue, Luo Zhiheng, chief economist at Yuekai Securities Co., wrote in a note earlier this month.

For Jack Liu, a 37-year-old sales engineer of aluminum products in southern China, the impact hit home after realizing he no longer ordered extra eggs at breakfasts.

Plummeting market demand forced his company to cut prices and sell at a loss last year. That slashed his income to less than a 10th of what once exceeded 1 million yuan ($141,000), making mortgage payments a struggle.

“The country doesn’t admit there’s deflation,” said Liu, who lives in Foshan in Guangdong province. He has a modest following of 1,100 people on the Instagram-like Xiaohongshu, where he warns regularly about the danger of deflation.

The speed of the deterioration in China’s price outlook has taken the market by surprise.

Inflation was weaker than forecast in three of the past four months, growing just 0.6% in August — an increase due largely to a 2.8% pickup in food prices. Core inflation last month rose just 0.3% to remain below 1% for an 18th month.

Underscoring the drag on inflation, producer prices have been falling since late 2022. Manufacturers’ raw material and selling prices both contracted for the second month in August, official data shows, while charges by services and construction companies shrank at the fastest pace since April 2020.

The dilemma is that even monetary expansion in China could be deflationary by being mainly directed at the supply side of the economy, Michael Pettis, a senior fellow at the Carnegie Endowment for International Peace, wrote in an article last month.

Meanwhile, the deflationary mindset is starting to take hold. Consumer confidence is hovering at a record low, and households report a growing willingness to save instead of spending or buying homes.

For Liu, the aluminum industry worker, as the pain deepens, the solution lies with policymakers in Beijing. “The government needs to at least take some concrete measures,” he said, “to lift consumption and improve people’s expectations.”

—With assistance from Fran Wang.

Most Read from Bloomberg Businessweek

Putting Olive Oil in a Squeeze Bottle Earned This Startup a Cult Following

‘They Have Stolen Our Business’: When You Leave Russia, Putin Sets the Terms

The Average American Eats 42 Pounds of Cheese a Year, and That Number Could Go Up

How Local Governments Got Hooked on One Company’s Janky Software

©2024 Bloomberg L.P.