Yahoo Finance

Yahoo Finance Is CF Energy (CVE:CFY) Using Too Much Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that CF Energy Corp. (CVE:CFY) does use debt in its business. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for CF Energy

What Is CF Energy's Net Debt?

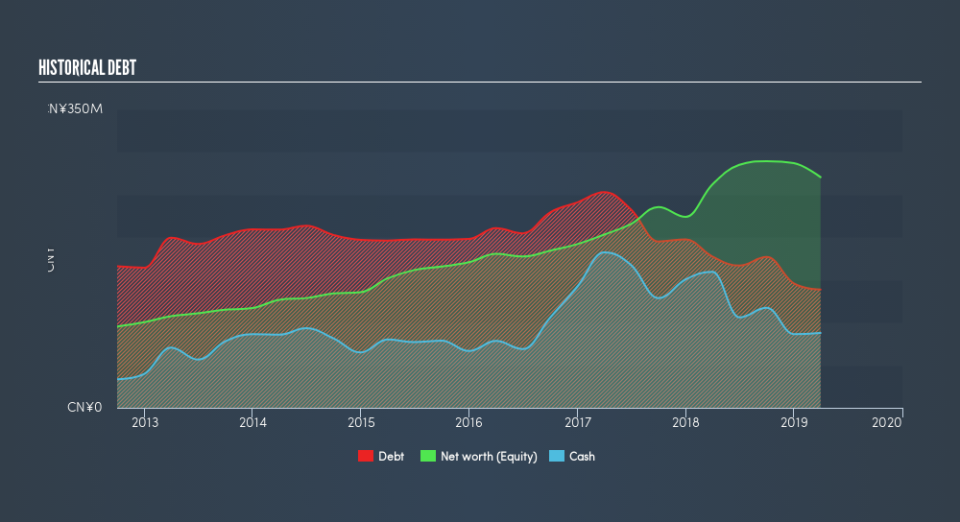

As you can see below, CF Energy had CN¥144.9m of debt at March 2019, down from CN¥177.4m a year prior. However, it also had CN¥87.8m in cash, and so its net debt is CN¥57.1m.

How Healthy Is CF Energy's Balance Sheet?

We can see from the most recent balance sheet that CF Energy had liabilities of CN¥261.2m falling due within a year, and liabilities of CN¥119.4m due beyond that. On the other hand, it had cash of CN¥87.8m and CN¥64.8m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥228.0m.

This deficit is considerable relative to its market capitalization of CN¥232.9m, so it does suggest shareholders should keep an eye on CF Energy's use of debt. This suggests shareholders would heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With net debt sitting at just 0.86 times EBITDA, CF Energy is arguably pretty conservatively geared. And it boasts interest cover of 7.1 times, which is more than adequate. The modesty of its debt load may become crucial for CF Energy if management cannot prevent a repeat of the 25% cut to EBIT over the last year. Falling earnings (if the trend continues) could eventually make even modest debt quite risky. There's no doubt that we learn most about debt from the balance sheet. But it is CF Energy's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Considering the last three years, CF Energy actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for and improvement.

Our View

To be frank both CF Energy's conversion of EBIT to free cash flow and its track record of (not) growing its EBIT make us rather uncomfortable with its debt levels. But on the bright side, its interest cover is a good sign, and makes us more optimistic. We should also note that Gas Utilities industry companies like CF Energy commonly do use debt without problems. Overall, it seems to us that CF Energy's balance sheet is really quite a risk to the business. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. In light of our reservations about the company's balance sheet, it seems sensible to check if insiders have been selling shares recently.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.