Yahoo Finance

Yahoo Finance Some CARBO Ceramics (NYSE:CRR) Shareholders Have Copped A 98% Share Price Wipe Out

Long term investing works well, but it doesn't always work for each individual stock. It hits us in the gut when we see fellow investors suffer a loss. Imagine if you held CARBO Ceramics Inc. (NYSE:CRR) for half a decade as the share price tanked 98%. And some of the more recent buyers are probably worried, too, with the stock falling 83% in the last year. On top of that, the share price has dropped a further 56% in a month. Importantly, this could be a market reaction to the recently released financial results. You can check out the latest numbers in our company report.

While a drop like that is definitely a body blow, money isn't as important as health and happiness.

See our latest analysis for CARBO Ceramics

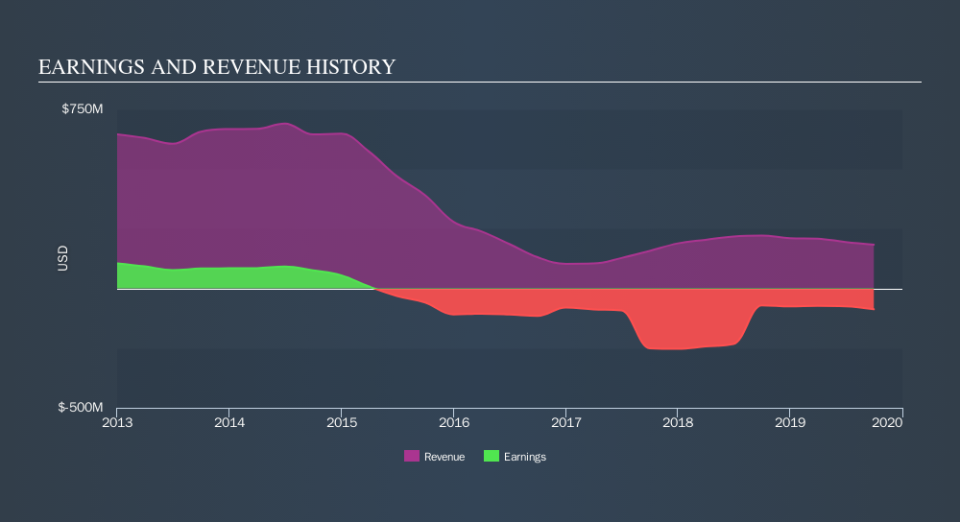

CARBO Ceramics isn't a profitable company, so it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Shareholders of unprofitable companies usually expect strong revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

Over half a decade CARBO Ceramics reduced its trailing twelve month revenue by 28% for each year. That puts it in an unattractive cohort, to put it mildly. So it's not altogether surprising to see the share price down 56% per year in the same time period. We don't think this is a particularly promising picture. Ironically, that behavior could create an opportunity for the contrarian investor - but only if there are good reasons to predict a brighter future.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

We like that insiders have been buying shares in the last twelve months. Even so, future earnings will be far more important to whether current shareholders make money. If you are thinking of buying or selling CARBO Ceramics stock, you should check out this free report showing analyst profit forecasts.

A Different Perspective

Investors in CARBO Ceramics had a tough year, with a total loss of 83%, against a market gain of about 15%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 56% over the last half decade. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. If you want to research this stock further, the data on insider buying is an obvious place to start. You can click here to see who has been buying shares - and the price they paid.

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.