Yahoo Finance

Yahoo Finance Do Birchcliff Energy's (TSE:BIR) Earnings Warrant Your Attention?

Like a puppy chasing its tail, some new investors often chase 'the next big thing', even if that means buying 'story stocks' without revenue, let alone profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses.

If, on the other hand, you like companies that have revenue, and even earn profits, then you may well be interested in Birchcliff Energy (TSE:BIR). While profit is not necessarily a social good, it's easy to admire a business that can consistently produce it. Conversely, a loss-making company is yet to prove itself with profit, and eventually the sweet milk of external capital may run sour.

Check out our latest analysis for Birchcliff Energy

How Fast Is Birchcliff Energy Growing Its Earnings Per Share?

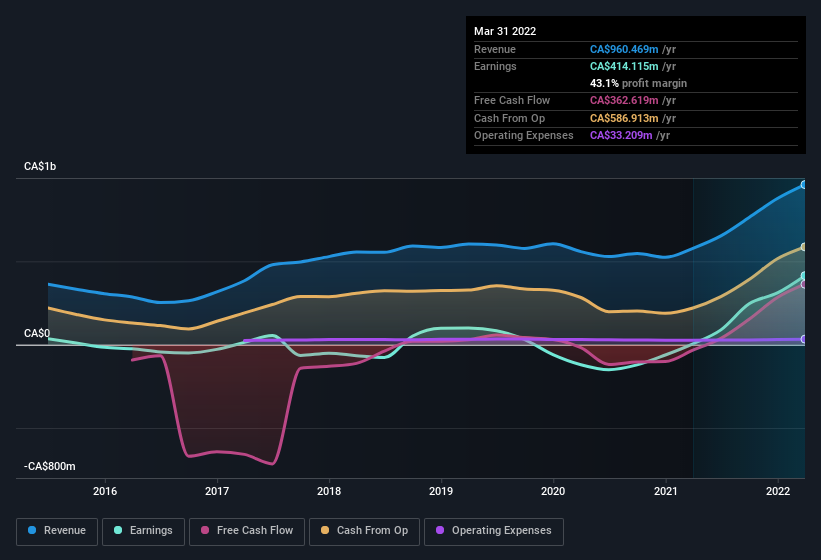

In business, though not in life, profits are a key measure of success; and share prices tend to reflect earnings per share (EPS). So like a ray of sunshine through a gap in the clouds, improving EPS is considered a good sign. You can imagine, then, that it almost knocked my socks off when I realized that Birchcliff Energy grew its EPS from CA$0.02 to CA$1.56, in one short year. Even though that growth rate is unlikely to be repeated, that looks like a breakout improvement. Could this be a sign that the business has reached an inflection point?

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). Birchcliff Energy shareholders can take confidence from the fact that EBIT margins are up from 7.0% to 59%, and revenue is growing. Ticking those two boxes is a good sign of growth, in my book.

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

Fortunately, we've got access to analyst forecasts of Birchcliff Energy's future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Are Birchcliff Energy Insiders Aligned With All Shareholders?

Like the kids in the streets standing up for their beliefs, insider share purchases give me reason to believe in a brighter future. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

In the last year insider at Birchcliff Energy were both selling and buying shares; but happily, as a group they spent CA$248k more on stock, than they netted from selling it. Although I don't particularly like to see selling, the fact that they put more capital in, than they extracted, is a positive in my mind. Zooming in, we can see that the biggest insider purchase was by CFO & Executive VP Bruno Geremia for CA$72k worth of shares, at about CA$6.40 per share.

The good news, alongside the insider buying, for Birchcliff Energy bulls is that insiders (collectively) have a meaningful investment in the stock. Indeed, they hold CA$47m worth of its stock. That's a lot of money, and no small incentive to work hard. Despite being just 1.5% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

While insiders are apparently happy to hold and accumulate shares, that is just part of the pretty picture. The cherry on top is that the CEO, Jeff Tonken is paid comparatively modestly to CEOs at similar sized companies. For companies with market capitalizations between CA$2.5b and CA$8.1b, like Birchcliff Energy, the median CEO pay is around CA$4.4m.

The Birchcliff Energy CEO received total compensation of just CA$1.9m in the year to . That's clearly well below average, so at a glance, that arrangement seems generous to shareholders, and points to a modest remuneration culture. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. It can also be a sign of good governance, more generally.

Does Birchcliff Energy Deserve A Spot On Your Watchlist?

Birchcliff Energy's earnings per share have taken off like a rocket aimed right at the moon. Just as heartening; insiders both own and are buying more stock. Because of the potential that it has reached an inflection point, I'd suggest Birchcliff Energy belongs on the top of your watchlist. What about risks? Every company has them, and we've spotted 1 warning sign for Birchcliff Energy you should know about.

As a growth investor I do like to see insider buying. But Birchcliff Energy isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.