Yahoo Finance

Yahoo Finance Bed Bath & Beyond (BBBY) Q1 Earnings & Sales Lag, Stock Dips

Shares of Bed Bath & Beyond Inc. BBBY plunged 23.6% at the close of the trading session on Jun 29, following the drab first-quarter fiscal 2022 results. Both top and bottom lines not only missed the Zacks Consensus Estimate but also declined year over year.

Results were affected by the ongoing macro-economic environment, the shift in customer preference, rising inflation, supply-chain challenges, and significant dislocation in sales and inventory.

In a bid to address the headwinds, management announced significant changes in senior leadership. In doing so, the company named Sue Gove, an independent director of its board and chair of the board's strategy committee, as its interim chief executive officer. The move comes after the exit of the earlier president and chief executive officer, Mark Tritton.

Earlier, under Tritton’s leadership, the company undertook a transformation strategy to stay afloat. As part of it, BBBY divested its non-core assets, invested in technology, infrastructure and digital capabilities, and launched Owned Brands.

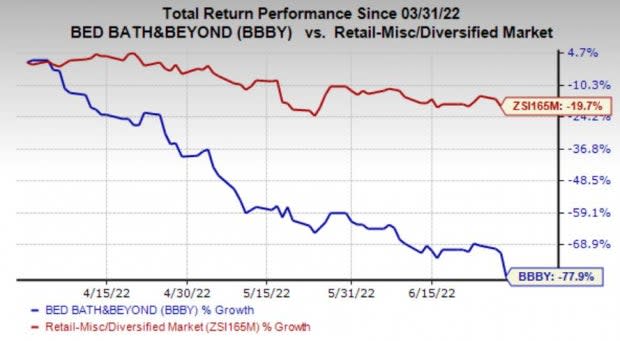

Consequently, shares of BBBY have plunged 77.9% in the past three months compared with the industry’s decline of 19.7%.

Image Source: Zacks Investment Research

That said, this Zacks Rank #3 (Hold) company remains committed to serving as a one-stop destination for home solutions. It is also focused on top-tier execution, cost management efforts, improved supply-chain reliability, better capital spending, robust digital capabilities and a stronger balance sheet.

Currently, it is adjusting its supply-chain infrastructure and cost structure to reflect lower sales. Also, the company halted its new store and remodel programs for the rest of fiscal 2022.

In another development, the company remains on track with evaluating options for the potential sale of buybuy BABY. It has been able to identify certain strategies to increase the synergies and growth potential of the brand.

Q1 in Detail

Bed Bath & Beyond reported an adjusted loss of $2.83 per share in the fiscal first quarter against earnings of 5 cents in the year-ago quarter. The figure was also wider than the Zacks Consensus Estimate of a loss of $1.33.

Net sales of $1,463 million declined 25% year over year and missed the Zacks Consensus Estimate of $1,514 million. This might be due to muted demand for household goods and a challenging macroeconomic environment.

Comparable sales (comps) fell 23% year over year. For stores, comps declined 24% year over year, while the same dropped 21% across the digital channel.

The Bed Bath & Beyond banner’s comparable sales fell 27% year over year, owing to sluggish demand in the Home sector and rapid changes in consumer spending patterns. These include Bedding, Bath, Kitchen Food Prep, Indoor décor, and Home Organization, representing two-thirds of the total Bed Bath & Beyond banner sales. The company’s buybuy BABY banner’s comparable sales declined year over year in the mid-single digits.

The adjusted gross profit slumped 48.9% to $348.1 million in the fiscal first quarter. However, the adjusted gross margin contracted 1110 basis points (bps) to 23.8%, including transient costs related to the 620-bps unfavorable impact of markdown inventory reserves and the 220-bps negative impact of supply chain-related port fees.

Excluding the transient costs, the metric came in at 32.2%. However, the company has been working with suppliers and accelerating markdowns to right-size inventory levels.

SG&A expenses slumped 3.2% to $637.5 million in the reported quarter, driven by reduced costs stemming from lower rent and occupancy expenses. Adjusted SG&A expenses, as a percentage of sales, expanded 990 bps year over year to 43.6% due to lower sales.

Adjusted EBITDA was negative $224 million against $86.1 million reported in the year-ago period. The decline was mainly due to sluggish sales and dismal margins. The adjusted EBITDA margin contracted 1090 bps year over year to 15.3%.

Financial Position

Bed Bath & Beyond ended the fiscal first quarter with cash and investments of $107.5 million. Long-term debt totaled $1,379.9 million and total shareholders' deficit was $220.3 million as of May 28, 2022. It also had strong liquidity of $0.9 billion as of May 28, 2022.

In the fiscal first quarter, cash used in operating activities was $383.6 million and capital expenditure was $104.9 million. For fiscal 2022, capital expenditure is expected to be $300 million, down from the earlier mentioned $400 million.

Bed Bath & Beyond Inc. Price, Consensus and EPS Surprise

Bed Bath & Beyond Inc. price-consensus-eps-surprise-chart | Bed Bath & Beyond Inc. Quote

Store Updates

In the reported quarter, the company opened five buybuy BABY stores, while shutting down two Bed Bath & Beyond stores and one Harmon store.

As of May 28, 2022, the company had 955 stores in operation, comprising 769 namesake stores across 50 states, the District of Columbia, Puerto Rico and Canada; 135 buybuy BABY stores; and 51 stores under Harmon, Harmon Face Values or Face Values names. Additionally, the company’s joint venture operates 12 flagship stores in Mexico.

Looking Ahead

Management issued a fiscal 2022 view. The company expects comparable sales in the second half of fiscal 2022 to improve on a sequential basis, driven by inventory optimization plans, including incremental clearance activity. Adjusted SG&A expenses are predicted to decline year over year on aggressive cost-cutting actions.

Stocks to Consider

Here are three better-ranked stocks to consider — Dillard’s DDS, Boot Barn Holdings BOOT and Canada Goose GOOS.

Dillard’s operates as a departmental store chain, featuring fashion apparel and home furnishings. It presently sports a Zacks Rank #1 (Strong Buy). DDS has a trailing four-quarter earnings surprise of 224.1%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Dillard’s current financial-year sales suggests growth of 6.1%, while the same for EPS indicates a decline of 33.9% from the year-ago period’s reported numbers. DDS has an expected EPS growth rate of 12.6% for three-five years.

Boot Barn, which provides western and work-related footwear, apparel and accessories, currently has a Zacks Rank #2 (Buy). The company has a trailing four-quarter earnings surprise of 25.2%, on average.

The Zacks Consensus Estimate for Boot Barn’s current financial-year sales and EPS suggests growth of 17% and 4.4%, respectively, from the year-ago period’s reported figures. BOOT has an expected EPS growth rate of 20% for three-five years.

Canada Goose is the designer, manufacturer, distributor and retailer of premium outerwear for men, women and children. It currently carries a Zacks Rank #2. GOOS has a trailing four-quarter earnings surprise of 65.9%, on average.

The Zacks Consensus Estimate for Canada Goose’s current financial year’s EPS suggests growth of 64.4% from the year-ago period’s reported figures. GOOS has an expected EPS growth rate of 27.4% for three-five years.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dillard's, Inc. (DDS) : Free Stock Analysis Report

Bed Bath & Beyond Inc. (BBBY) : Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT) : Free Stock Analysis Report

Canada Goose Holdings Inc. (GOOS) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research