Yahoo Finance

Yahoo Finance Barnwell Industries (NYSEMKT:BRN) Will Have To Spend Its Cash Wisely

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But while history lauds those rare successes, those that fail are often forgotten; who remembers Pets.com?

So, the natural question for Barnwell Industries (NYSEMKT:BRN) shareholders is whether they should be concerned by its rate of cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

Check out our latest analysis for Barnwell Industries

How Long Is Barnwell Industries's Cash Runway?

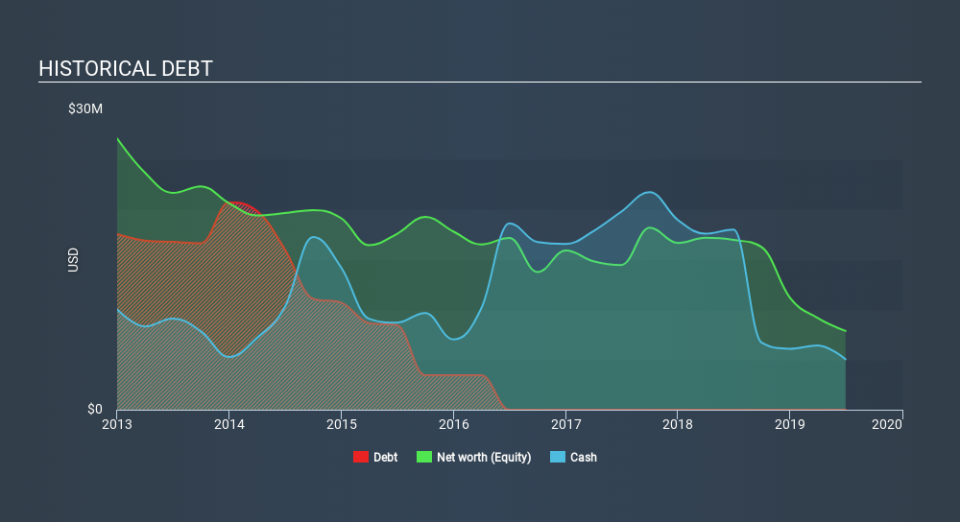

A company's cash runway is calculated by dividing its cash hoard by its cash burn. When Barnwell Industries last reported its balance sheet in June 2019, it had zero debt and cash worth US$5.0m. In the last year, its cash burn was US$15m. Therefore, from June 2019 it had roughly 4 months of cash runway. With a cash runway that short, we strongly believe that the company must raise cash or else douse its cash burn promptly. Importantly, if we extrapolate recent cash burn trends, the cash runway would be noticeably longer. The image below shows how its cash balance has been changing over the last few years.

How Well Is Barnwell Industries Growing?

Notably, Barnwell Industries actually ramped up its cash burn very hard and fast in the last year, by 152%, signifying heavy investment in the business. But the silver lining is that operating revenue increased by 50% in that time. Considering the factors above, the company doesn’t fare badly when it comes to assessing how it is changing over time. In reality, this article only makes a short study of the company's growth data. You can take a look at how Barnwell Industries is growing revenue over time by checking this visualization of past revenue growth.

How Easily Can Barnwell Industries Raise Cash?

Since Barnwell Industries has been boosting its cash burn, the market will likely be considering how it can raise more cash if need be. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash to drive growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of US$4.4m, Barnwell Industries's US$15m in cash burn equates to about 331% of its market value. Given just how high that expenditure is, relative to the company's market value, we think there's an elevated risk of funding distress, and we would be very nervous about holding the stock.

So, Should We Worry About Barnwell Industries's Cash Burn?

There are no prizes for guessing that we think Barnwell Industries's cash burn is a bit of a worry. In particular, we think its cash burn relative to its market cap suggests it isn't in a good position to keep funding growth. On the other hand at least it could boast rather strong revenue growth, which no doubt gives shareholders some comfort. Once we consider the metrics mentioned in this article together, we're left with very little confidence in the company's ability to manage its cash burn, and we think it will probably need more money. While it's important to consider hard data like the metrics discussed above, many investors would also be interested to note that Barnwell Industries insiders have been trading shares in the company. Click here to find out if they have been buying or selling.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.