Yahoo Finance

Yahoo Finance Bank of Nova Scotia: Emerging Markets and Dividend Growth Combined

Written by Kay Ng at The Motley Fool Canada

Bank of Nova Scotia (TSX:BNS) is known for its international exposure. Its core business segments are Canadian Banking, International Banking, Global Wealth Management, and Global Banking & Markets. Could emerging markets and dividend growth combined lead to higher returns for BNS shareholders?

Not necessarily.

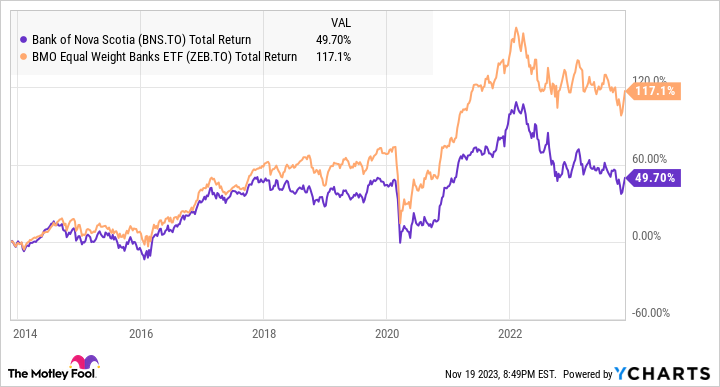

In the last three-, five-, and 10-year periods, the total returns of Scotiabank stock have underperformed the industry, using BMO Equal Weight Banks Index ETF (TSX:ZEB) as a proxy. The exchange-traded fund has roughly an equal weight in the Big Six Canadian bank stocks, including BNS stock.

BNS and ZEB 10-Year Total Return Level data by YCharts

The international bank is exposed to emerging markets, which were intended for higher growth potential. However, they also expose the bank to higher risk, which typically results in higher credit losses. For example, in the pandemic-hit fiscal year of 2020, Bank of Nova Scotia’s provision for credit losses (PCL) as a percentage of average net loans and acceptances was 0.98% versus a more normal level of PCL at 0.51% in the prior fiscal year.

Royal Bank of Canada, which is a more defensive bank and has core businesses in Personal & Commercial Banking and Wealth Management, had lower PCL ratios of 0.63% in fiscal 2020 and 0.31% in fiscal 2019. Similarly, BNS’s PCL ratio on impaired loans was 0.56% in fiscal 2020 and 0.49% in fiscal 2019, which were higher than RBC’s PCL ratios of 0.24% and 0.27%, respectively.

Bank of Nova Scotia’s return on equity (ROE), which is a measure of financial performance (calculated by net income divided by shareholders’ equity), ended up being 10.4% in fiscal 2020 and 13.1% in fiscal 2019, whereas RBC’s were 14.2% and 16.8%, respectively.

In a higher interest rate environment, BNS’s fiscal year-to-date PCL ratio on impaired loans is 0.33% versus RBC’s 0.20%. In this period, Scotiabank’s ROE was 11.5% versus RBC’s 13.9%.

BNS stock could still be a good investment

Despite the underperformance, Bank of Nova Scotia has remained profitable, even during challenging economic periods. So, the stock could still be a good investment, especially if you are an income investor and target to buy at depressed stock prices for a high dividend yield.

Over the years, the international bank has exited a number of international markets that didn’t work well, which has dragged on the bank’s performance as there had been write-downs, for example. However, it still managed to deliver a dividend-growth rate of 5.8% over the past 10 fiscal years.

Currently, the bank makes more than 50% of its revenues and earnings from Canada, and for its international operations, it is primarily focused on Latin America in geographies like Mexico, Peru, and Chile. Hopefully, these changes would allow BNS stock to experience above-average growth, leading to price-to-earnings ratio (P/E) expansion in a more favourable macro environment down the road.

At $61.09 per share, BNS stock offers a safe, juicy dividend yield of about 6.9%. It also trades at a discount to its historical trading level. At a P/E of about 8.7, it trades at a discount of approximately 22% from its long-term normal P/E. Scott Thompson came into the chief executive officer role only in February.

At these depressed levels, BNS stock has the potential to be a turnaround play over the next five years. One possibility is a 20% rate of return based on the big dividend, P/E expansion, and a 5% earnings-per-share growth rate.

The post Bank of Nova Scotia: Emerging Markets and Dividend Growth Combined appeared first on The Motley Fool Canada.

Should You Invest $1,000 In Bank of Nova Scotia?

Before you consider Bank of Nova Scotia, you'll want to hear this.

Our market-beating analyst team just revealed what they believe are the 5 best stocks for investors to buy in November 2023... and Bank of Nova Scotia wasn't on the list.

The online investing service they've run for nearly a decade, Motley Fool Stock Advisor Canada, is beating the TSX by 24 percentage points. And right now, they think there are 5 stocks that are better buys.

See the 5 Stocks * Returns as of 11/14/23

More reading

Fool contributor Kay Ng has positions in Bank Of Nova Scotia and Royal Bank Of Canada. The Motley Fool recommends Bank Of Nova Scotia. The Motley Fool has a disclosure policy.

2023