Yahoo Finance

Yahoo Finance Sheila Bair: The danger of allowing banks to artificially boost capital ratios

Yahoo Finance’s Brian Cheung contributed data to this article.

“Never let a good crisis go to waste,” Rahm Emmanuel famously said in 2009. As President Obama’s Chief of Staff, he was speaking of the opportunity to achieve meaningful financial reforms in the aftermath of the Great Financial Crisis.

Ironically, big bank lobbyists are now using the Covid-19 crisis to undo those very reforms, cynically claiming deregulation will help banks support the real economy. Their primary target is the leverage ratio, a key measure of financial stability which big banks have long despised because it places hard and fast constraints on their ability to use unstable leverage to generate high returns. Weakening the leverage ratio will reduce the capital resiliency of the banking system, while giving banks incentives to actually reduce lending to artificially boost their capital ratios.

It is generally recognized that a main cause of the 2008-2009 financial crisis was excessive reliance on debt, or “leverage,” by large financial institutions. Central to post-GFC reforms was a strengthening of rules that require banks to fund themselves with a minimum amount of equity capital. There are two sets of requirements: “risk-based” rules which set minimum capital based on the perceived riskiness of a bank’s assets and “leverage ratios,” which do not allow such adjustments. A key disadvantage of risk based requirements is that they are subjective. They failed spectacularly prior to the GFC, when US and European regulators wrongly assumed mortgages and sovereign debt were low risk. The disadvantage of leverage ratios is that they are not risk-adjusted, requiring the same amount of capital against a US Treasury security (which we hope is safe) as a loan to Boeing. Each has strengths and weaknesses, which is why regulators use both.

Gaming the supplementary leverage ratio

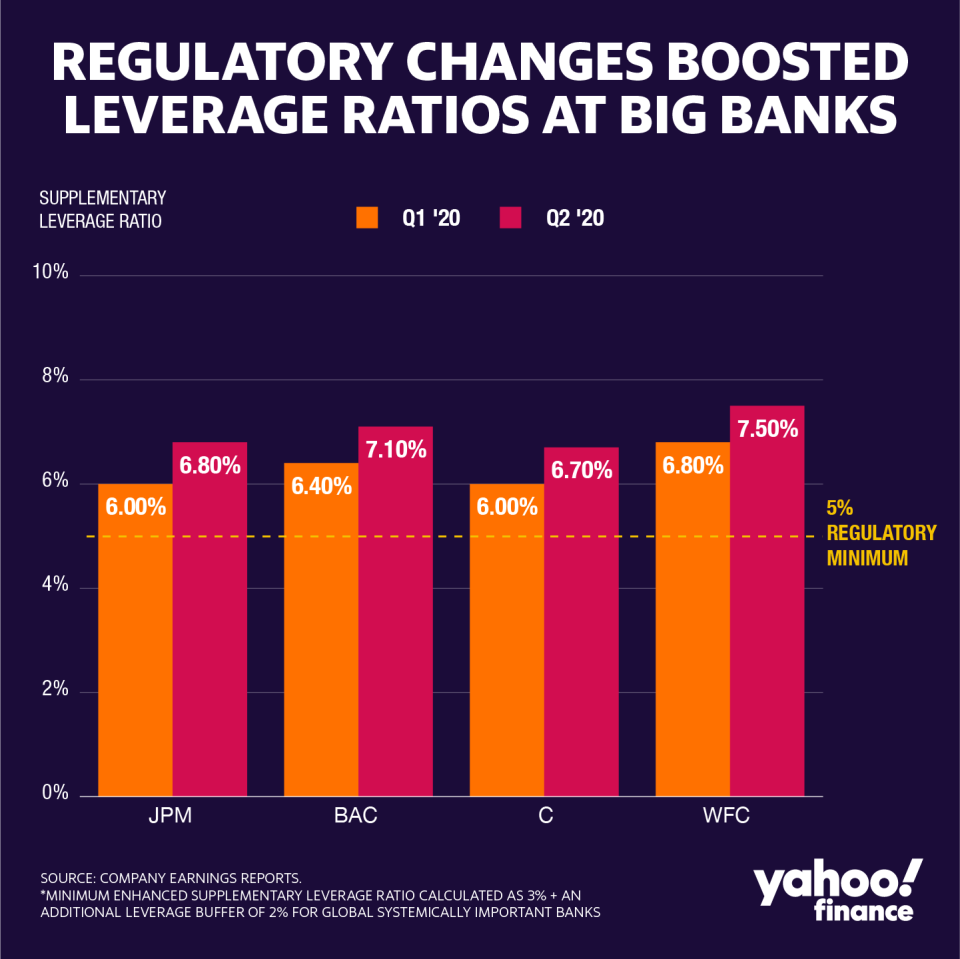

The whole idea behind leverage ratios is that they are not risk-adjusted. They apply to all assets, including presumably safe ones, which is one of the reasons why they are set significantly lower than risk-based requirements. For the largest banking organizations, the main leverage constraint (called the Enhanced Supplementary Leverage Ratio or ESLR) is set at a minimum of 5%, but their risk-based ratios are roughly double that. Leverage ratios (calculated for the largest banks as Tier 1 capital divided by total leverage exposure) set rails around risk-based ratios, and banks’ ability to inflate them simply by manipulating the denominator. A bank can significantly increase its risk-based ratios by changing its asset mix, reducing its exposure to assets treated as high-risk under the rules, and then moving to assets treated as low-risk. Indeed, the largest banks typically risk-weight their assets at less than half of total assets. But the denominator of the leverage ratio cannot be so gamed.

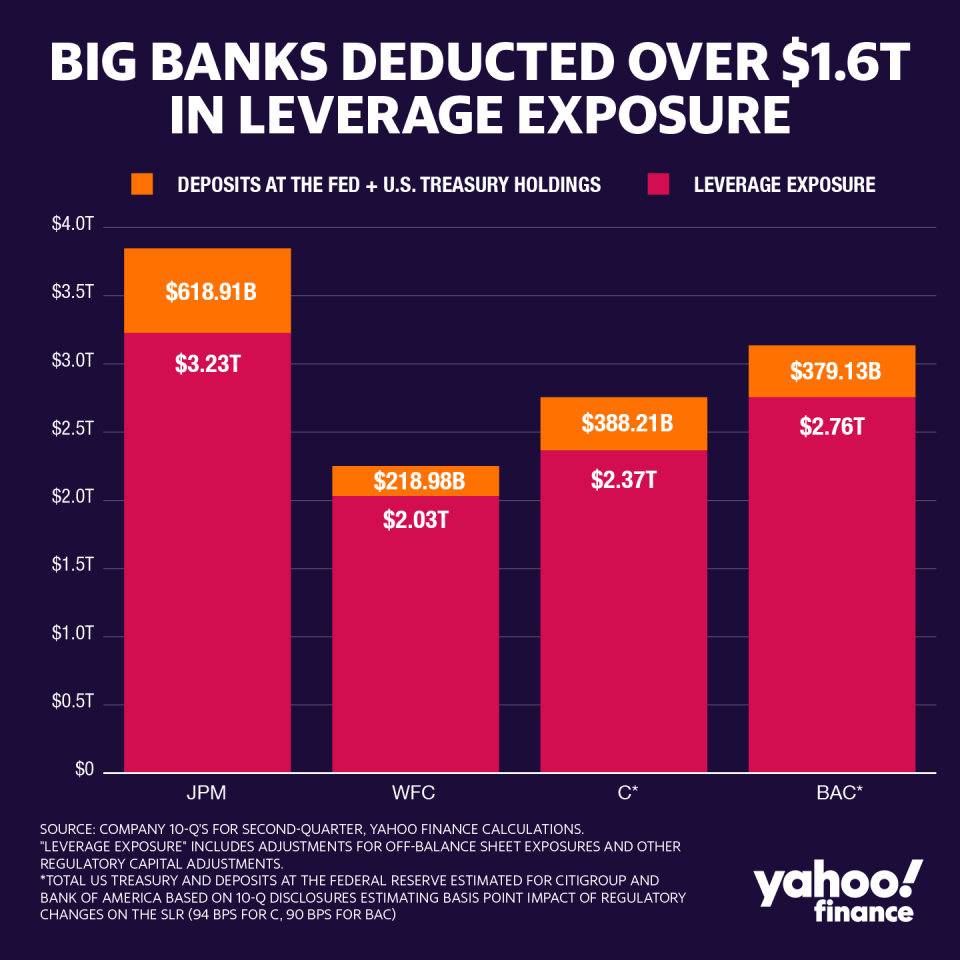

At least until now. The Federal Reserve and other bank regulators have temporarily allowed “risk-free” assets (US Treasuries and deposits at the Federal Reserve) to be removed from the denominator of the ESLR. With this simple adjustment, banks can report significantly stronger leverage ratios. As the chart below shows, this change allowed the biggest banks to remove over $1.6T in the second quarter from their leverage ratio denominators.

Those are assets to which the ESLR’s 5% equity capital requirement will no longer apply. The big four banks were able to reduce their reported leverage by between 10% to 16%, while raising minuscule new capital.

Perversely, while this change has been touted by its advocates as increasing lending, it will create incentives to do just the opposite. Banks will now have greater opportunities to dress up their risk based ratios as well. They can do this by reducing lending – as private sector loans typically have capital requirements of 8% or more--and move funds into Treasuries and Reserve deposits which now have zero capital requirements under both the risk-based rules and ESLR.

The ESLR used to get in the way of such games with its pesky 5% capital requirement. By reducing lending and buying more government debt, banks can improve their risk-based ratios which are used by regulators to decide whether they can pay dividends. This could help them ride out the crisis by playing it safe, but won’t do much for the credit needs of the private sector.

Why not target dividends?

There is one legitimate policy reason for making this change: it will increase banks’ capacity to buy US Treasuries. The government certainly needs buyers of its debt - it is issuing a lot of it! And those funds are providing fiscal support for households and small businesses. But if this is the problem regulators are trying to solve, they could easily tailor a leverage ratio adjustment confined to government securities operations above their pre-pandemic levels.

Even better, the Fed could stop bank dividend payments. Based on current rules, which permit leverage of 16 to 1 for FDIC-insured banks, retaining $30 billion in the first quarter would have provided nearly a half trillion in expanded capacity.

The Fed has suggested that other jurisdictions have made similar adjustments. That is not quite accurate. Except for Canada, other jurisdictions have only excluded Reserve deposits. And unlike the Fed, the Bank of England and European Central Bank have halted dividends to make sure capital relief stays on banks’ balance sheets and is not distributed to shareholders. To its credit, the Bank of England also increased its leverage ratio to prevent depletion of the overall level of capital in its banking system.

The Fed, backed by industry, is seeking statutory changes as part of its next stimulus bill to give the Fed more authority to further weaken leverage constraints. The Fed’s discretion is currently limited by a provision of Dodd-Frank that sets a floor against capital reductions based on their 2010 levels. Sadly, in the Senate, the GOP, which used to celebrate leverage ratios — they were a centerpiece of the Republican alternative to Dodd-Frank — are championing this change, saying it will boost lending. Ironic for fiscal conservatives to support this, thinking it will promote lending, when in fact it will encourage banks to reduce private sector lending in favor of buying the U.S. government securities to finance those skyrocketing Federal deficits they decry.

Will the lobbyists win? The Democrats are fighting back but they have other priorities in the stimulus bills, and it is not beyond bank lobbyists to hold up much-needed relief until they get what they want. This is reminiscent of the years leading up to the GFC, when bank lobbying pressure led to destabilizing deregulation. Bank lobbyists will not want to let this crisis go to waste. But the Fed could stop them by reversing its ill-advised position.

-

Sheila Bair is the former Chair of the FDIC and has held senior appointments in both Republican and Democrat Administrations. She currently serves as a board member or advisor to several companies and is a founding board member of the Volcker Alliance, a nonprofit established to rebuild trust in government.

Read more:

Low interest rates widen the gap between Main Street and Wall Street

The mystery behind the Fed’s refusal to suspend bank dividends

Why student loan forgiveness should target graduates who need it the most

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.