Yahoo Finance

Yahoo Finance Adapting to Higher Rates: 2 TSX Stocks That Can Weather the Storm

Written by Kay Ng at The Motley Fool Canada

Higher interest rates have generally increased the cost of capital, thereby reducing the growth outlook of many companies. Simultaneously, certain stocks have been depressed, providing a potential opportunity to buy on weakness to invest for the long term. Here are a couple of dividend stocks that look interesting with underlying businesses that appear to be adapting well to higher interest rates.

RBC stock is defensive against higher rates

The Bank of Canada raised the policy interest rate through 2022. Since last year, Royal Bank of Canada (TSX:RY) stock has held up better than its big Canadian bank peers. This suggests it has been adapting to higher rates better.

Below is a graph comparing the price action of RBC stock to the BMO Equal Weight Banks Index ETF since the beginning of 2022. The ZEB exchange-traded fund (ETF) maintains a roughly equal-weight holding of the Big Six Canadian bank stocks. Currently, RBC is its smallest holding at a weight of about 16%.

RY and ZEB data by YCharts

One reason for the bank stock’s resilience and defence is its diversified business. Its operations are diversified, in terms of revenue generated in fiscal 2022, as follows: personal and commercial banking (40%), wealth management (30%), capital markets (18%), insurance (7%), and investor and treasury services (4%).

At $126.52 per share at writing, RBC stock is fairly valued at about 11.3 times earnings. It offers a decent dividend yield of almost 4.3%. Its dividend is sustainable, and investors can expect dividend increases in the long run. Though, in recessions, the regulator may request the bank and its peers halt dividend increases, which has occurred in the past.

We just revealed five stocks as “best buys” this month … join Stock Advisor Canada to find out if WELL Health made the list!

Brookfield Infrastructure Partners fares well in a higher-rate market

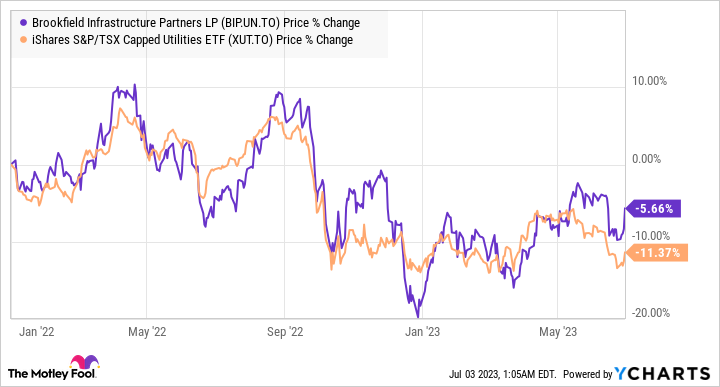

Utilities are innately debt-heavy businesses. Similar to Royal Bank, Brookfield Infrastructure Partners L.P. (TSX:BIP.UN) stock has held up better than its peers in a period of higher interest rates. Below is a chart comparing the price action of Brookfield Infrastructure Partners L.P. stock to the iShares S&P/TSX Capped Utilities Index ETF since the start of 2022. The XUT ETF consists of 10 utilities. Currently, Brookfield Infrastructure Partners is its second-largest holding, weighing roughly 17.2% of the fund.

BIP.UN and XUT data by YCharts

Brookfield Infrastructure Partners is a very well run utility that is comprised of a diversified portfolio of long-life, quality infrastructure assets around the world. It owns and operates utilities, transport, midstream, and data assets. Its assets are primarily funded by non-recourse debt. So, in the worst-case scenario, if an asset turns out to be bad, it can be handed over to the creditor, while the rest of the portfolio will stay intact.

The utility is a steady-eddie business. With a combined strategy of acquiring quality assets on a value basis, enhancing assets through operational expertise, and selling mature assets to reinvest, management targets funds-from-operations-per-unit (FFOPU) growth of north of 10% per year, which would drive cash distribution growth of 5-9%. BIP also maintains a sustainable FFO payout ratio of 60-70%.

At $48.42 per unit at writing, BIP offers a cash distribution yield of about 4.2%. The stock also trades at a discount of about 14%. So, interested investors could pick up some units.

The post Adapting to Higher Rates: 2 TSX Stocks That Can Weather the Storm appeared first on The Motley Fool Canada.

Should You Invest $1,000 In Brookfield Infrastructure Partners?

Before you consider Brookfield Infrastructure Partners, you'll want to hear this.

Our market-beating analyst team just revealed what they believe are the 5 best stocks for investors to buy in June 2023... and Brookfield Infrastructure Partners wasn't on the list.

The online investing service they've run for nearly a decade, Motley Fool Stock Advisor Canada, is beating the TSX by 28 percentage points. And right now, they think there are 5 stocks that are better buys.

See the 5 Stocks * Returns as of 6/28/23

More reading

Fool contributor Kay Ng has positions in Brookfield Infrastructure Partners. The Motley Fool recommends Brookfield Infrastructure Partners. The Motley Fool has a disclosure policy

2023