Yahoo Finance

Yahoo Finance These 4 Measures Indicate That GP Strategies (NYSE:GPX) Is Using Debt Extensively

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, GP Strategies Corporation (NYSE:GPX) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for GP Strategies

What Is GP Strategies's Net Debt?

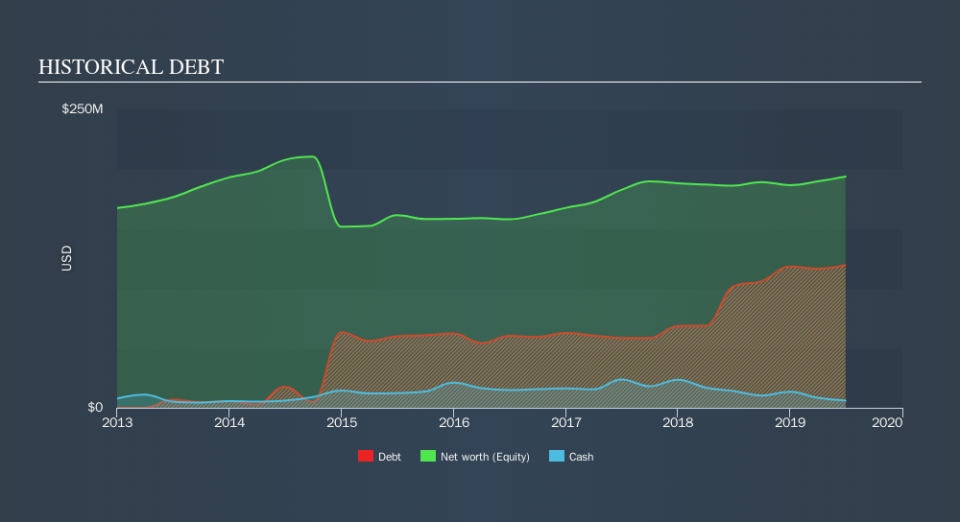

You can click the graphic below for the historical numbers, but it shows that as of June 2019 GP Strategies had US$119.7m of debt, an increase on US$101.8m, over one year. However, it does have US$6.11m in cash offsetting this, leading to net debt of about US$113.5m.

A Look At GP Strategies's Liabilities

The latest balance sheet data shows that GP Strategies had liabilities of US$113.0m due within a year, and liabilities of US$154.5m falling due after that. Offsetting these obligations, it had cash of US$6.11m as well as receivables valued at US$191.4m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$70.0m.

While this might seem like a lot, it is not so bad since GP Strategies has a market capitalization of US$187.0m, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

GP Strategies's debt is 4.5 times its EBITDA, and its EBIT cover its interest expense 3.6 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Another concern for investors might be that GP Strategies's EBIT fell 15% in the last year. If that's the way things keep going handling the debt load will be like delivering hot coffees on a pogo stick. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if GP Strategies can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, GP Strategies's free cash flow amounted to 38% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

To be frank both GP Strategies's net debt to EBITDA and its track record of (not) growing its EBIT make us rather uncomfortable with its debt levels. But at least its level of total liabilities is not so bad. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making GP Strategies stock a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of GP Strategies's earnings per share history for free.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.