Yahoo Finance

Yahoo Finance These 4 Measures Indicate That CVR Energy (NYSE:CVI) Is Using Debt Reasonably Well

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, CVR Energy, Inc. (NYSE:CVI) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

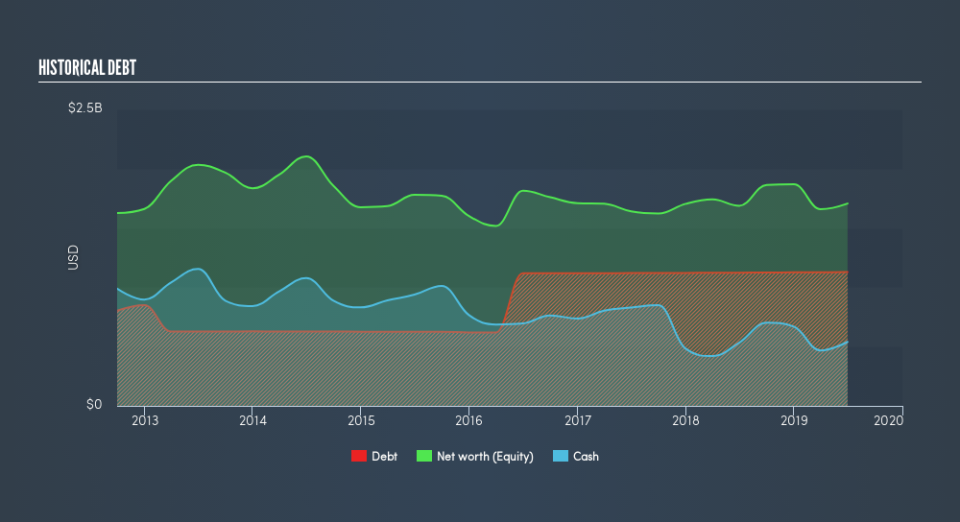

See our latest analysis for CVR Energy

What Is CVR Energy's Net Debt?

As you can see below, CVR Energy had US$1.13b of debt, at June 2019, which is about the same the year before. You can click the chart for greater detail. However, it does have US$540.0m in cash offsetting this, leading to net debt of about US$588.0m.

How Strong Is CVR Energy's Balance Sheet?

We can see from the most recent balance sheet that CVR Energy had liabilities of US$482.0m falling due within a year, and liabilities of US$1.64b due beyond that. On the other hand, it had cash of US$540.0m and US$168.0m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.42b.

CVR Energy has a market capitalization of US$4.31b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Looking at its net debt to EBITDA of 0.65 and interest cover of 6.8 times, it seems to us that CVR Energy is probably using debt in a pretty reasonable way. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Better yet, CVR Energy grew its EBIT by 149% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine CVR Energy's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. During the last three years, CVR Energy generated free cash flow amounting to a very robust 97% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Our View

Happily, CVR Energy's impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. And that's just the beginning of the good news since its EBIT growth rate is also very heartening. Looking at the bigger picture, we think CVR Energy's use of debt seems quite reasonable and we're not concerned about it. While debt does bring risk, when used wisely it can also bring a higher return on equity. Given CVR Energy has a strong balance sheet is profitable and pays a dividend, it would be good to know how fast its dividends are growing, if at all. You can find out instantly by clicking this link.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.