Yahoo Finance

Yahoo Finance 4 Consumer Products Stocks to Watch Amid Industry Hurdles

Players in the Zacks Consumer Products – Staples industry are witnessing a margin pressure on account of cost inflation, induced by escalated costs of inputs, transport and labor. Adverse currency movements are also posing a challenge to some companies.

Strategic saving measures, robust e-commerce operations, and a focus on portfolio enhancement and innovation are consistently working well for Chewy, Inc. CHWY, Albertsons Companies, Inc. ACI, Grocery Outlet Holding Corp. GO and Ollie's Bargain Outlet Holdings, Inc. OLLI.

About the Industry

The Zacks Consumer Products – Staples industry consists of companies involved in marketing, producing and distributing a wide range of consumer products. These include personal care items, cleaning equipment, stationery, bed and bath products, and household goods like kitchen appliances, cutlery and food storage. Some of the industry participants also provide batteries and lighting products whereas some offer pet food and treats, pet supplies, pet medications and pet services. Companies in the Consumer Products – Staples universe offer products to supermarkets, drug/grocery stores, department stores, warehouse clubs, mass merchandisers and other retail outlets. Some companies sell products to manufacturers of perfumes and cosmetics, hair and other personal care products. Products are also sold through other distributors and the fast-growing e-commerce channel.

3 Trends Shaping the Future of the Consumer Products - Staples Industry

Cost Woes Persist: A rise in input costs is hurting a number of players in the industry. The companies are also seeing increased labor, transportation and freight costs due to tough market conditions. Several companies are bearing the brunt of supply-chain disruptions. A number of companies had projected the input cost inflation to persist in the near term in their last quarterly release. Besides, higher SG&A costs, costs related to digital development and increased wages are eating into the margins of some companies. The companies’ restructuring plans and pricing actions should offer some respite.

Adverse Currency Movements: A number of companies remain vulnerable to unfavorable currency movements due to their exposure to the international markets. This is because a strengthening U.S. dollar may require a company to either raise prices or contract profit margins in locations outside the United States. Some industry players, such as Kimberly-Clark expect hostile currency fluctuations to affect their performances in 2022.

Revenue-Driving Initiatives: Consumer product players are focused on concerted revenue-boosting initiatives to squeeze out more from their operations. To this end, companies’ solid focus on boosting e-commerce and digital operations has been a major driver to date. Also, innovation in areas witnessing an increasing consumer interest enhanced the portfolio strength of companies. Industry players have been optimizing portfolios through meaningful buyouts and divestitures for a while, enabling them to intensify their focus on areas with higher-growth potential.

Zacks Industry Rank Indicates Dull Prospects

The Zacks Consumer Products – Staples industry is housed within the broader Zacks Consumer Staples sector. It currently carries a Zacks Industry Rank #204, which places it in the bottom 7% of more than 250 Zacks industries.

The group’s Zacks Industry Rank, basically the average of the Zacks Rank of all the member stocks, indicates drab near-term prospects. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

The industry’s position in the bottom 50% of the Zacks-ranked industries is a result of a negative earnings outlook for the constituent companies in aggregate. Looking at the aggregate earnings estimate revisions, it appears that analysts are gradually becoming less confident about this group’s earnings growth potential. Since the beginning of July 2022, the industry’s earnings estimate for 2022 has declined 5.1%.

Let’s look at the industry’s performance and current valuation.

Industry Lags Broader Market & Sector

The Zacks Consumer Products – Staples industry has lagged the S&P 500 Index as well as the broader Zacks Consumer Staples sector over the past year.

The industry has dropped 32.1% over this period compared with the S&P 500 Index’s decline of 9.5%. The broader sector has dipped 3.2%.

One-Year Price Performance

Industry's Current Valuation

On the basis of forward 12-month price-to-earnings (P/E), commonly used for valuing consumer staples stocks, the industry is currently trading at 18.12X compared with the S&P 500’s 17.7X and the sector’s 19.15X.

Over the last five years, the industry has traded as high as 25.76X, as low as 13.8X and at the median of 19.96X, as the chart below shows.

Price-to-Earnings Ratio (Past 5 Years)

4 Consumer Products Stocks to Keep a Close Eye on

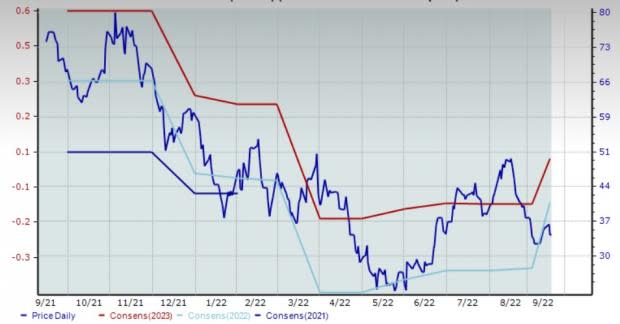

Chewy: The currently Zacks Rank #2 (Buy) player has been gaining for a while from its robust customer value proposition and favorable demand for its food and healthcare categories. This pure-play pet e-tailer continues witnessing an increased market share and an improved leadership position. CHWY’s strong product portfolio, compelling merchandise and a seamless shopping experience are steadily working well for it.

The Zacks Consensus Estimate for CHWY’s current fiscal-year bottom line has improved from a loss of 35 cents to a loss of 11 cents in the last 30 days. Chewy has an estimated long-term earnings growth rate of 20%. Shares of Chewy have plunged 52.1% in the past year.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Price and Consensus: CHWY

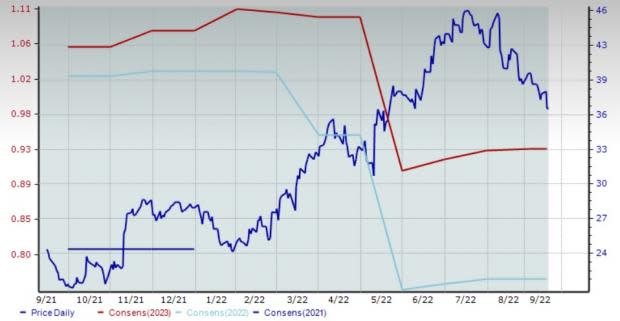

Albertsons Companies: This presently Zacks Rank #3 (Hold) player’s focus on providing efficient in-store services, enhancing digital and omni-channel capabilities, and increasing productivity bodes well. The Zacks Consensus Estimate for ACI’s current fiscal-year earnings per share (EPS) has been unchanged at $2.93 in the past 30 days.

This food and drug store entity constantly gains on its efforts to improve the store and digital operations. Albertsons Companies’ efforts to boost assortments, especially in the fresh and Own Brands categories, continue elevating customers’ experience. Shares of ACI have declined 6.8% in the past year. The stock has an estimated long-term earnings growth rate of 5.8%.

Price and Consensus: ACI

Grocery Outlet Holding: The stock with a Zacks Rank of 3 at present has rallied 50.3% over the past year. GO’s flexible sourcing and distribution business model, which helps offer products at exceptional values, bodes well. Grocery Outlet’s opportunistic purchasing strategy, marketing efforts, store-growth endeavors and e-commerce initiatives to deepen customer reach also appear encouraging.

The Zacks Consensus Estimate for GO’s current fiscal-year EPS has been steady at 99 cents in the past 30 days. Grocery Outlet, a high-growth, extreme value retailer of quality, name-brand consumables and fresh products, has an estimated long-term earnings growth rate of 11.9%.

1.

Price and Consensus: GO

Ollie’s Bargain: This value retailer of brand name merchandise at drastically reduced prices is benefiting from its focus on store productivity and expansion of customer reward program, Ollie's Army. OLLI's business model of “buying cheap and selling cheap” and cost-containment efforts also bode well.

This currently Zacks #3 Ranked player’s shares have declined 22% in a year’s time. The Zacks Consensus Estimate for OLLI’s current fiscal-year EPS has declined from $1.88 to $1.78 over the past 30 days. Ollie’s Bargain currently has an estimated long-term earnings growth rate of 16.1%.

Price and Consensus: OLLI

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Albertsons Companies, Inc. (ACI) : Free Stock Analysis Report

Ollie's Bargain Outlet Holdings, Inc. (OLLI) : Free Stock Analysis Report

Grocery Outlet Holding Corp. (GO) : Free Stock Analysis Report

Chewy (CHWY) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research