Yahoo Finance

Yahoo Finance The Year’s $321 Billion EM Bond Spree Looks Set to Slow Down

(Bloomberg) -- After a blockbuster six months, the sale of emerging-market bonds in hard currencies is set to slow down sharply in a second-half that’s littered with political risk.

Most Read from Bloomberg

24-Hour Stock Trading Is Booming – and Wall Street Is Rattled

Trump as President or Private Citizen: Why Supreme Court’s Immunity Ruling Is a Test

France’s Market Rally Falters as Investors See Enduring Risk

Justice Department to Charge Boeing, Seeks Guilty Plea From Planemaker

The amount of debt sold by government and corporate borrowers in developing markets has reached $321 billion in the busiest first-half since 2021, according to data compiled by Bloomberg. Still, forecasts from JPMorgan Chase & Co. and Bank of America Corp. show issuance is poised to slow more than usual after borrowers rushed to meet their funding needs at the beginning of the year.

As governments from France to Bolivia face political upheaval, Thursday’s US debate also brought the White House race into clearer view, with analysts warning of more global volatility that could keep EM issuers at bay. The fear of such turbulence has already partly pushed borrowers to load up on as much debt as they could, leaving less supply for the remainder of 2024.

“In terms of 2024 funding need, probably 80% is already done,” said Alexander Karolev, head of bond syndicate for Central and Eastern Europe, Middle East and Africa at JPMorgan. “The volumes that we’ve seen so far are not going to be sustainable.”

While it’s common for bond auctions to taper off in the second-half, this year saw a particularly fast start as renewed access to markets for many frontier issuers and juicy yields fueled a 32% surge in sales from the first six months of 2023, the biggest increase since 2017.

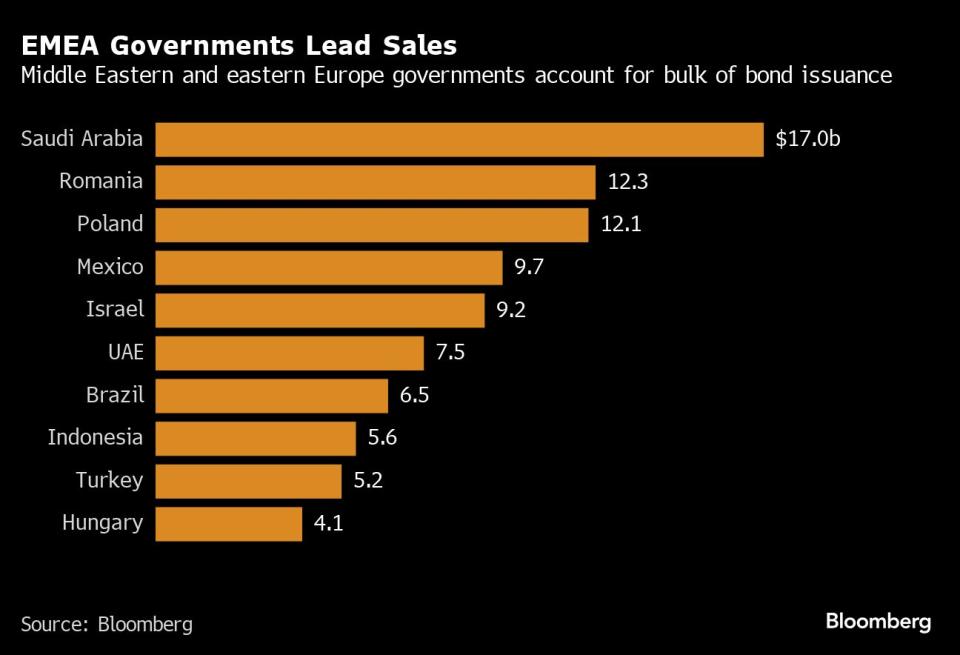

Among borrowers, Saudi Arabia dethroned China as the most prolific seller with around $35 billion in deals. International debt issued by sub-Saharan African nations rose from zero in the second half of 2023 to $11 billion, while Latin America’s biggest economies — Brazil and Mexico — pulled a combined record of $12 billion in dollar notes in January alone.

Corporate deals have bounced back as well, with euro and dollar debt issues of $168 billion, up from $108 billion in 2023.

Even so, the buoyancy of the market hasn’t been matched by a jump in returns.

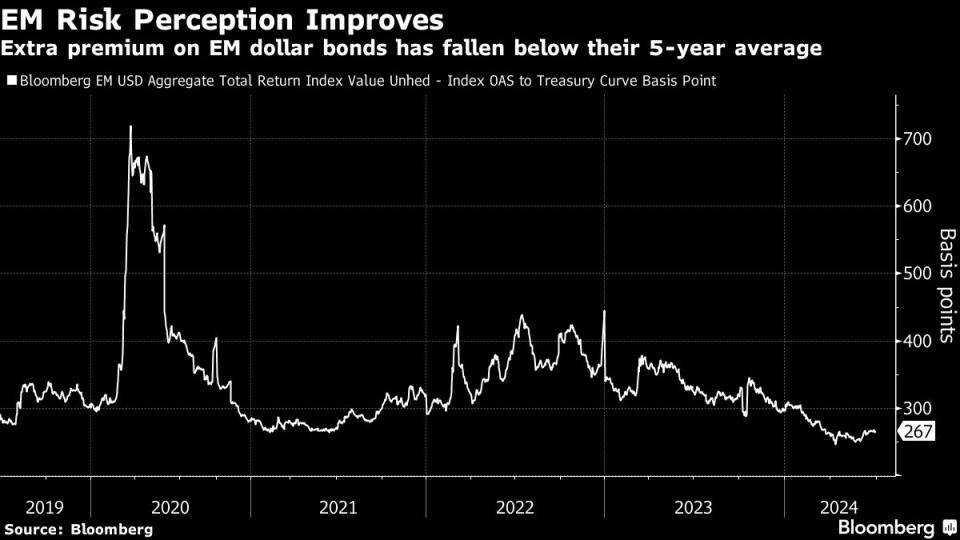

EM dollar bonds have handed holders a 2.2% gain so far this year, down from 3.4% a year ago, due to surging yields on pared-back expectations for US rate cuts and political upheaval in developing economies such as India and Mexico. The performance is roughly in line though with US high-yield corporate bonds, an alternative risk asset, while returns for Treasuries remain negative.

Going forward, fewer sales would support prices as demand outweighs supply and keep issuers’ debt sustainability in check, according to Philip Fielding, co-head of emerging markets at MacKay Shields.

“Less issuance creates scarcity in bond markets,” Fielding said. “In the first six months, we saw net issuance, while in the second half of the year, supply can be less than coupons and redemptions,” boosting bond prices, he said.

JPMorgan, the second-biggest arranger of EM bonds, expects sovereign issuance in hard currencies to total $163 billion this year, while corporate sales could top $300 billion. EM governments have already raised $119 billion and companies borrowed $172 billion, according to data compiled by Bloomberg.

Any upheaval in the build-up toward US elections would impact market appetite and the timing of sales, said Jonathan Marshak, an emerging-market credit strategist at BNP Paribas SA. The vote could weigh on concerns about the US budget deficit and global trade, he said.

“There’s some risk of volatility on the Treasuries that impacts the cost of funding, regardless whether you’re in EM or in US,” said Adrian Guzzoni, head of debt capital markets for Latin America at Citigroup Inc., the biggest arranger of EM debt.

August, usually a quiet month, could see more deals if sellers want to get ahead of election risks, BNP’s Marshak said. If not, issuers may delay until November or December, or even into 2025, he said.

“There will be a better window for issuance after the US election,” said Merveille Paja, a sovereign credit strategist for Eastern Europe, Middle East and Africa at Bank of America. The Fed’s first rate cut, which the bank has penciled in for December, would also be a boon for borrowing costs, she said.

BofA sees sovereign sales of about $60 billion for the rest of the year, with issuance stemming mostly from Mexico, Turkey, China, Indonesia and the United Arab Emirates, according to Paja. BNP expects China to make a strong comeback, with big deals expected in the Philippines, South Africa and Bulgaria as well.

Morgan Stanley sees a further $70 billion in sovereign bond sales, partly due to its forecast for early US monetary policy easing.

“Our expectation of Fed rate cuts in September and some large issuers still needing to issue” will support sales, the bank said in a note on Friday, listing Hungary, Colombia, Angola, Morocco, Nigeria, Oman and Rwanda as potential sellers.

Still, heightened volatility before the US election could impact borrowing costs and increase spreads over safer debt, said BNP’s Marshak.

“Such volatility would likely put issuance on pause, ” he said.

What to Watch:

Investors will monitor the minutes of the Colombian central bank’s latest meeting following its Friday decision

Chile’s economic activity is expected to have risen 2.35% in May from a year earlier, according to Bloomberg Economics

Hungary is taking over the European Union’s rotating presidency as of Monday

Poland’s central bank is expected to leave its key interest rate unchanged at a July 3 meeting

Expect a flurry of CPI reports from nations including Turkey, South Korea, Indonesia, the Philippines, Thailand and Pakistan

(Updates returns figure in the ninth paragraph)

Most Read from Bloomberg Businessweek

The Fried Chicken Sandwich Wars Are More Cutthroat Than Ever Before

Japan’s Tiny Kei-Trucks Have a Cult Following in the US, and Some States Are Pushing Back

RTO Mandates Are Killing the Euphoric Work-Life Balance Some Moms Found

The FBI’s Star Cooperator May Have Been Running New Scams All Along

©2024 Bloomberg L.P.