Yahoo Finance

Yahoo Finance 3 Canadian Stocks That Could Be Huge Winners in the Next Decade and Beyond

Written by Kay Ng at The Motley Fool Canada

These Canadian stocks could be big winners for patient and strategic investors. Take your pick!

One energy stock that performs well through economic cycles

At today’s still high oil prices, oil stocks like Parex Resources (TSX:PXT) continue to generate substantial free cash flow for dividends and stock buybacks.

The oil producer is headquartered in Calgary, but its operations are in Colombia. So, it enjoys premium Brent oil pricing versus the Western Canadian Select (WCS) pricing. For example, at writing, the Brent oil price is about US$93 per barrel, which is 23% higher than the WCS oil price.

Parex actually had the resources to buy back stock when oil prices turned negative in 2020 during the global pandemic.

PXT Average Diluted Shares Outstanding (Annual) data by YCharts

Funny enough, the energy stock trades at a much cheaper cash flow multiple now due to the jump in cash flow generation. Its trailing 12-month (TTM) free cash flow generation is more than US$424 million, a 145% jump from the 2020 level. At about $21 per share, the undervalued stock trades at dirt-cheap levels of about 2.4 times blended cash flow.

It initiated a quarterly dividend around this time last year. This dividend has already doubled! Its TTM payout ratio is less than 20% of free cash flow, which provides a big buffer to protect its dividend. It’s good for a yield of close to 4.8% right now.

As Parex focuses on growing production per share and continues to repurchase shares and pay out a nice dividend, it can create impressive shareholder value for the decade to come.

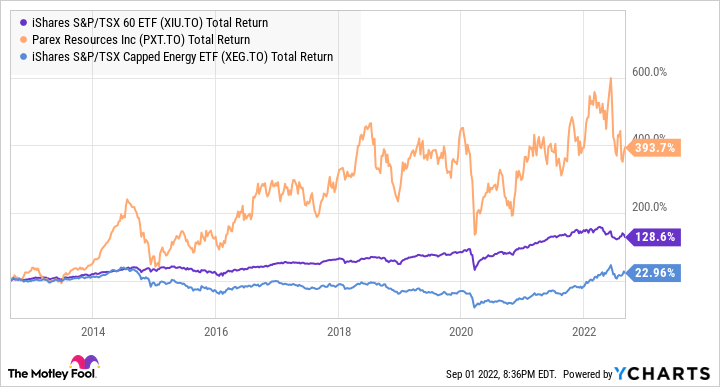

Parex stock outperformed the energy sector and the Canadian stock market in the last decade. And currently, it trades at a similarly cheap valuation as it did 10 years ago!

XIU Total Return Level data by YCharts

A cyclical stock with growth potential

Linamar (TSX:LNR) enjoys a higher net margin than its peers. Additionally, it trades at a low multiple of about 9.1 times blended earnings. The auto parts maker can surface value and unlock growth for its common stockholders over the next few years, as the economy normalizes from macro events. I mean events such as the COVID pandemic and respective economic lockdowns here and there and the semiconductor chip crunch.

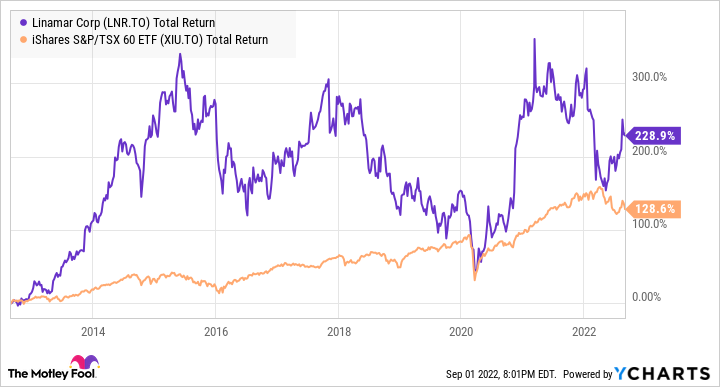

Investors should keep in mind that the consumer discretionary stock is a roller-coaster ride. However, precisely because of this volatility, you may be able to buy it cheap and experience a real winner. To illustrate, here’s how Linamar stock fared in total returns versus the Canadian stock market, using iShares S&P/TSX 60 Index ETF as a proxy, over the last decade.

LNR Total Return Level data by YCharts

Right now, the analyst consensus price targets upside of over 28% over the next 12 months. That would likely beat the market returns in the period.

This tech stock could be a multi-bagger

Now and over the next few months could be a golden opportunity to load up on Converge Technology Solutions (TSX:CTS). The tech stock has been unjustly punished along with the market selloff in today’s wobbly market. It seems investors have lost confidence in the financial market in an economy of rising costs from high inflation and rising interest rate.

Small-cap Converge stock with a market cap of about $1.2 billion now has shaken off many weak hands, as half of its stock value evaporated in the last 12 months. However, the company continues to deliver superb results.

In the first half of the year, it increased revenue by 75% to $1.15 billion versus a year ago. Gross profit jumped 66% to $242.2 million. Adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization), a cash flow proxy, rose 70% to $68.8 million. Adjusted net income doubled to $52.4 million. And adjusted earnings per share improved by 50% to $0.24.

The company is growing its scale quickly with acquisitions, expanding its technology solution offerings and cross-selling its products and services. It’s also good to see organic growth from its integration and optimization of acquired businesses.

The absurd discount in the growth stock coupled with its high-growth profile could make Converge a multi-bagger stock in the next decade, as it expands in North America and Europe.

The post 3 Canadian Stocks That Could Be Huge Winners in the Next Decade and Beyond appeared first on The Motley Fool Canada.

Should You Invest $1,000 In Converge?

Before you consider Converge, you'll want to hear this.

Our market-beating analyst team just revealed what they believe are the 5 best stocks for investors to buy in August 2022 ... and Converge wasn't on the list.

The online investing service they've run for nearly a decade, Motley Fool Stock Advisor Canada, is beating the TSX by 27 percentage points. And right now, they think there are 5 stocks that are better buys.

See the 5 Stocks * Returns as of 8/8/22

More reading

Fool contributor Kay Ng has positions in Converge Technology Solutions and Parex Resources. The Motley Fool recommends LINAMAR CORP.

2022