Yahoo Finance

Yahoo Finance 2 Undervalued Canadian Stocks Worth a Buy Right Now

Written by Kay Ng at The Motley Fool Canada

So, you want to buy Canadian stocks that are on sale? It may not be as simple as you think. Why might a stock be undervalued in the first place? There must be something going on. If stocks appear to be undervalued and in time things improve for their underlying businesses, then the undervalued stocks could make you outsized returns.

Here are a couple of Canadian stocks that are curiously undervalued for different reasons.

Why TC Energy stock is depressed

It was bad news after bad news that triggered investors to sell off TC Energy (TSX:TRP) stock. First, in December, its Keystone Pipeline spilled oil in a creek in Kansas. The spill is estimated to cost US$480 million to clean up.

Then this month, it announced cost overruns for its Coastal GasLink Pipeline project. As Reuters published, “Coastal’s costs are now up 30% to $14.5 billion, from the project’s previous estimate of $11.2 billion, which was already raised by 70% in July from the initial budget.”

TC Energy listed reasons for the increased cost, including higher cost of material, shortage of skilled labour, contract worker underperformance, and adverse weather. The company said the project could cost an additional $1.2 billion if construction were extended into 2024.

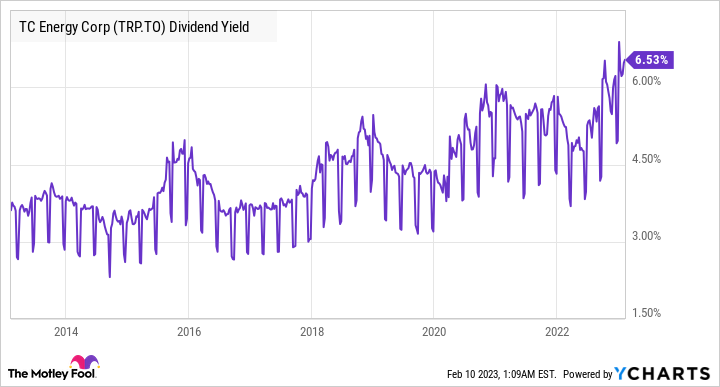

These all weigh on the stock in the near term. Analysts have accordingly reduced TRP’s consensus 12-month price target, which implies a discount of about 11% from the recent quotation of about $55 per share. Because of all the bad news, here we have a Canadian Dividend Aristocrat that yields 6.5% — the highest yield in 10 years.

TRP Dividend Yield data by YCharts

As time passes and when things improve for TC Energy, the stock price will rise, and analysts will raise their price targets. Interested investors could buy half a position now, and potentially add more shares should the dividend stock experiences further weakness.

Bank of Nova Scotia stock lost to peers in the past year

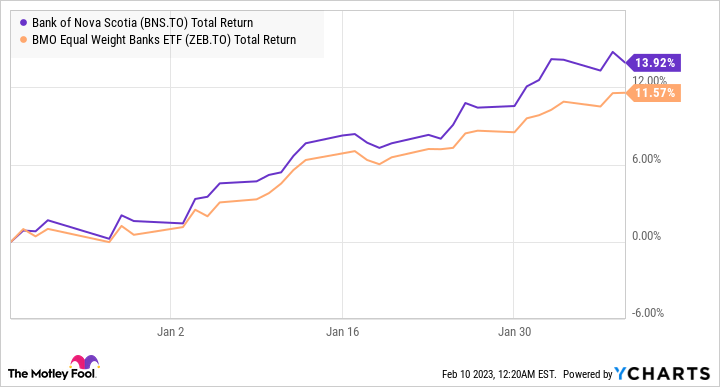

In the past 12 months, Bank of Nova Scotia (TSX:BNS) returned about -17.7%, while BMO Equal Weight Banks Index ETF returned -9.3%. Although no investor wants negative returns, there’s no argument that the exchange-traded fund was a better hold, as it gave more diversification in the Canadian banking industry, including providing exposure to the best bank stocks.

BNS and ZEB Total Return Level data by YCharts

However, if you were able to pick up BNS shares when they were an absolute bargain, you could have beat the industry. This is why value investing is a popular investing strategy.

BNS and ZEB Total Return Level data by YCharts

The bank stock underperforms at times, as it is more exposed to the commodity cycle than its peers due to its international exposure. Additionally, this month, a new chief executive officer, Scott Thomson, stepped up to the role. It could take time for him to prove himself.

BNS stock trades at a meaningful discount of about 23% from its long-term normal valuation. If things turn for the better for the bank, it could deliver outperforming returns over the next five years.

Investing takeaway

Stocks are meant for long-term investing of five years or longer. By buying and sitting on a diversified basket of solid stocks that appear to be undervalued, investors have a chance of getting outsized returns.

The post 2 Undervalued Canadian Stocks Worth a Buy Right Now appeared first on The Motley Fool Canada.

Free Dividend Stock Pick: 7.9% Yield and Monthly Payments

Canada’s inflation rate has skyrocketed to 6.9%, meaning you’re effectively losing money by investing in a GIC, or worse, leaving your money in a so-called “high interest” savings account.

That’s why we’re alerting investors to a high-yield Canadian dividend stock that looks ridiculously cheap right now. Not only does it yield a whopping 7.9%, but it pays monthly!

Here’s the best part: We’re giving this dividend pick away for FREE today.

Claim your free dividend stock pick * Percentages as of 11/29/22

More reading

Brookfield Asset Management Spin-Off: What Investors Need to Know

Passive Income: 4 Safe Dividend Stocks to Own for the Next 10 Years

Fool contributor Kay Ng has positions in Bank Of Nova Scotia and TC Energy. The Motley Fool recommends Bank Of Nova Scotia. The Motley Fool has a disclosure policy.

2023