Yahoo Finance

Yahoo Finance Here's Why You Should Buy Align Technology (ALGN) Stock Now

Align Technologies ALGN is well-poised to grow in the coming quarters, backed by the significant opportunity for Invisalign's expansion into the vast, untapped global malocclusion market. The increased adoption of the Invisalign IPE system buoys optimism, with the company launching the device in several geographies. However, substantial dependence on the Invisalign system and stiff competition are a concern.

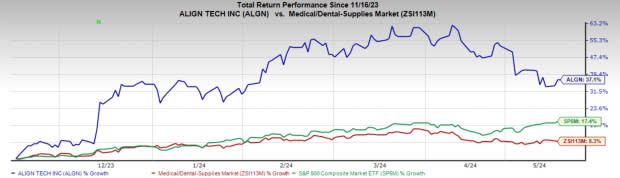

In the past six months, this Zacks Rank #3 (Hold) stock has increased 37.1% compared with the 8.3% rise of the industry and 17.4% growth of the S&P 500 composite.

The renowned medical device company has a market capitalization of $20.93 billion. ALGN’s earnings surpassed estimates in three of the trailing four quarters and missed in one, the average surprise being 5.92%.

Let’s delve deeper.

Upsides

Invisalign’s Untapped Potential: Align Technology is strategically capturing the growing malocclusion market, one of the most prevalent clinical dental conditions in the world.

In first-quarter 2024, Align Technology acquired Cubicure, a leader in direct 3D printing solutions, among major milestones. This acquisition is the foundation for the company’s next-generation aligner manufacturing. The company also launched the iTero Lumina intraoral scanner, its next generation of digital scanning technology and the Invisalign Palatal Expander (IPE) system in the United States and Canada. It also received regulatory approval for the Invisalign Palatal Expander in Australia and New Zealand.

Geographic Expansion Continues: Align Technology is expanding its sales and marketing by reaching new countries and regions, including new areas within Africa and Latin America.

The company also performs digital treatment planning and interpretation for restorative cases worldwide, including in Costa Rica, China, Germany, Spain, Poland and Japan, among others. Align Technology continues to expand its business through investments in resources, infrastructure and initiatives that help drive growth in Invisalign treatment, intraoral scanners and Exocad CAD/CAM software in existing and new international markets.

Upbeat Guidance: For 2024, ALGN anticipates revenues to be up 6-8% year over year (up from the previous guidance of up mid-single digits in 2023). The Zacks Consensus Estimate for the company’s 2024 revenues is pegged at $4.04 billion.

Image Source: Zacks Investment Research

GAAP and adjusted operating margins for the full year are anticipated to be slightly above the 2023 GAAP and adjusted operating margins, respectively.

For the second quarter of 2024, ALGN anticipates worldwide revenues in the range of $1.03-$1.05 billion. The Zacks Consensus Estimate is pegged at $1.03 billion.

Downsides

Competitive Landscape: Align Technology faces significant competition from traditional orthodontic appliance (or wires and brackets) players such as 3M’s Unitek, Danaher Corporation’s Sybron Dental Specialties and Dentsply International. The company also competes with products similar to Invisalign Technology, such as products from Ormco Orthodontics, a division of Sybron Dental Specialties.

Overdependence on Invisalign Technology System: The bulk of Align Technology's net revenues largely depends on the sale of its Invisalign Technology System, primarily Invisalign Technology Full and Invisalign Technology Teen. Continued and widespread market acceptance of Invisalign Technology by orthodontists, GPs and consumers is critical to Align Technology’s future success. Management fears that if consumers start preferring a competitive product over Invisalign, the company’s operating results will suffer.

Estimate Trend

The Zacks Consensus Estimate for Align Technologies’ 2024 earnings per share (EPS) has moved up to $9.65 from $9.46 in the past 90 days.

The Zacks Consensus Estimate for the company’s 2024 revenues is pegged at 4.11 billion. The metric suggests a 6.5% rise from the year-ago reported number.

Key Picks

Some better-ranked stocks from the broader medical space are Medpace MEDP, ResMed RMD and Encompass Health Corporation EHC.

Medpace, sporting a Zacks Rank #1 (Strong Buy), reported first-quarter 2024 EPS of $3.20, which beat the Zacks Consensus Estimate by 30.6%. Revenues of $511 million appreciated 17.7% from last year’s comparable figure. You can see the complete list of today’s Zacks #1 Rank stocks here.

Medpace has an estimated 2024 earnings growth rate of 26.5% compared with the industry’s 12.3%. The company’s earnings surpassed estimates in each of the trailing four quarters, the average being 12.8%.

ResMed, sporting a Zacks Rank #2 (Buy), reported a first-quarter 2024 EPS of $2.13, which topped the Zacks Consensus Estimate by 10.9%. Revenues of $1.20 billion surpassed the Zacks Consensus Estimate by 1.9%.

RMD has an estimated fiscal 2024 earnings growth rate of 17.9% compared to the industry’s 15.7%. In each of the trailing four quarters, the company delivered an average earnings surprise of 2.8%.

Encompass Health, carrying a Zacks Rank #2, reported a first-quarter 2024 adjusted EPS of $1.12, which surpassed the Zacks Consensus Estimate by 20.4%. Net operating revenues of $1.3 billion topped the Zacks Consensus Estimate by 3.6%.

EHC has an estimated long-term earnings growth rate of 15.6% compared with the industry’s 11.7% growth. The company’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 18.7%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Align Technology, Inc. (ALGN) : Free Stock Analysis Report

ResMed Inc. (RMD) : Free Stock Analysis Report

Medpace Holdings, Inc. (MEDP) : Free Stock Analysis Report

Encompass Health Corporation (EHC) : Free Stock Analysis Report