Yahoo Finance

Yahoo Finance Why We Think Tractor Supply Company (NASDAQ:TSCO) Could Be Worth Looking At

As an investor, I look for investments which do not compromise one fundamental factor for another. By this I mean, I look at stocks holistically, from their financial health to their future outlook. In the case of Tractor Supply Company (NASDAQ:TSCO), it is a financially-sound , dividend-paying company with an impressive history of performance. Below is a brief commentary on these key aspects. For those interested in digging a bit deeper into my commentary, read the full report on Tractor Supply here.

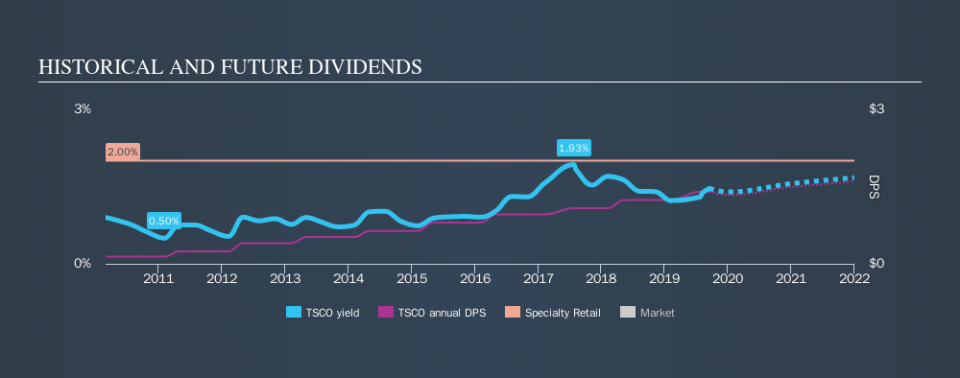

Solid track record established dividend payer

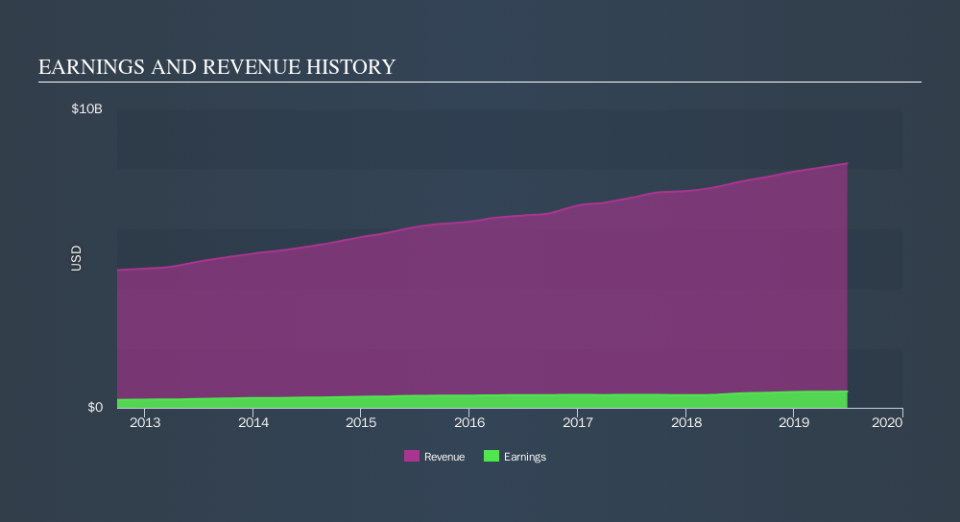

Over the past year, TSCO has grown its earnings by 15%, with its most recent figure exceeding its annual average over the past five years. The strong earnings growth is reflected in impressive double-digit 36% return to shareholders, which paints a buoyant picture for the company. TSCO is financially robust, with ample cash on hand and short-term investments to meet upcoming liabilities. This suggests prudent control over cash and cost by management, which is a key determinant of the company’s health. TSCO appears to have made good use of debt, producing operating cash levels of 1.57x total debt in the prior year. This is a strong indication that debt is reasonably met with cash generated.

For those seeking income streams from their portfolio, TSCO is a robust dividend payer as well. Over the past decade, the company has consistently increased its dividend payout, reaching a yield of 1.5%.

Next Steps:

For Tractor Supply, there are three pertinent factors you should further examine:

Future Outlook: What are well-informed industry analysts predicting for TSCO’s future growth? Take a look at our free research report of analyst consensus for TSCO’s outlook.

Valuation: What is TSCO worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether TSCO is currently mispriced by the market.

Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of TSCO? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.