Yahoo Finance

Yahoo Finance Why It Might Not Make Sense To Buy Whitecap Resources Inc. (TSE:WCP) For Its Upcoming Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Whitecap Resources Inc. (TSE:WCP) is about to go ex-dividend in just 4 days. If you purchase the stock on or after the 27th of February, you won't be eligible to receive this dividend, when it is paid on the 16th of March.

Whitecap Resources's next dividend payment will be CA$0.029 per share. Last year, in total, the company distributed CA$0.34 to shareholders. Calculating the last year's worth of payments shows that Whitecap Resources has a trailing yield of 7.1% on the current share price of CA$4.81. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to investigate whether Whitecap Resources can afford its dividend, and if the dividend could grow.

See our latest analysis for Whitecap Resources

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. An unusually high payout ratio of 246% of its profit suggests something is happening other than the usual distribution of profits to shareholders. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. Over the last year it paid out 57% of its free cash flow as dividends, within the usual range for most companies.

It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and Whitecap Resources fortunately did generate enough cash to fund its dividend. Still, if the company repeatedly paid a dividend greater than its profits, we'd be concerned. Very few companies are able to sustainably pay dividends larger than their reported earnings.

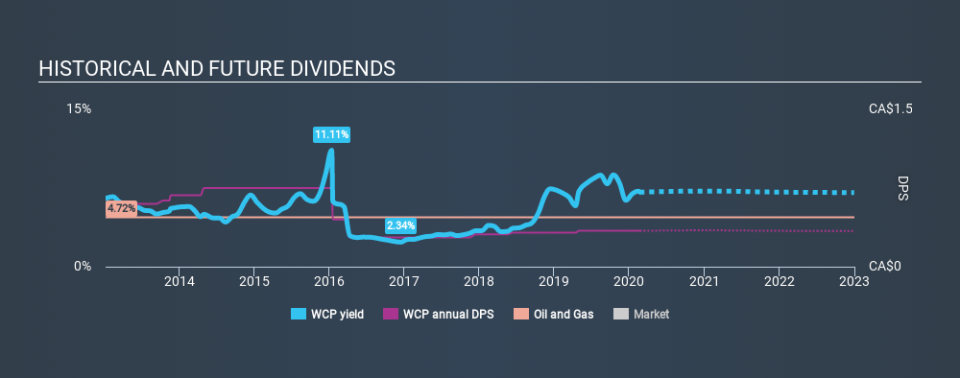

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. Whitecap Resources's earnings per share have fallen at approximately 13% a year over the previous five years. Such a sharp decline casts doubt on the future sustainability of the dividend.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Whitecap Resources has seen its dividend decline 7.7% per annum on average over the past seven years, which is not great to see. While it's not great that earnings and dividends per share have fallen in recent years, we're encouraged by the fact that management has trimmed the dividend rather than risk over-committing the company in a risky attempt to maintain yields to shareholders.

Final Takeaway

Should investors buy Whitecap Resources for the upcoming dividend? It's never fun to see a company's earnings per share in retreat. What's more, Whitecap Resources is paying out a majority of its earnings and over half its free cash flow. It's hard to say if the business has the financial resources and time to turn things around without cutting the dividend. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

Ever wonder what the future holds for Whitecap Resources? See what the four analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.