Yahoo Finance

Yahoo Finance Can Weekend Unlimited (CNSX:POT) Afford To Invest In Growth?

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So, the natural question for Weekend Unlimited (CNSX:POT) shareholders is whether they should be concerned by its rate of cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

See our latest analysis for Weekend Unlimited

How Long Is Weekend Unlimited's Cash Runway?

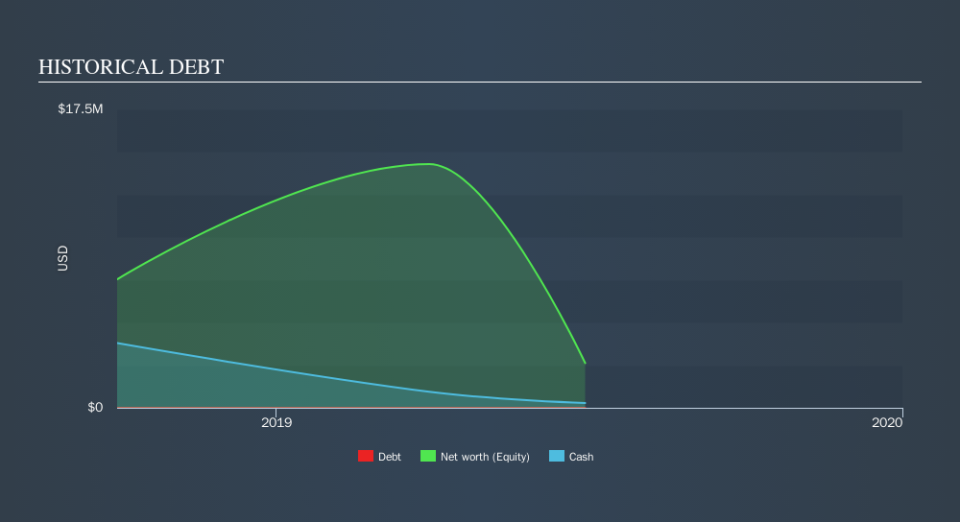

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. When Weekend Unlimited last reported its balance sheet in June 2019, it had zero debt and cash worth US$283k. Looking at the last year, the company burnt through US$7.3m. That means it had a cash runway of under two months as of June 2019. To be frank we are alarmed by how short that cash runway is! You can see how its cash balance has changed over time in the image below.

How Hard Would It Be For Weekend Unlimited To Raise More Cash For Growth?

Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Commonly, a business will sell new shares in itself to raise cash to drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of CA$26m, Weekend Unlimited's US$7.3m in cash burn equates to about 37% of its market value. That's fairly notable cash burn, so if the company had to sell shares to cover the cost of another year's operations, shareholders would suffer some costly dilution.

How Risky Is Weekend Unlimited's Cash Burn Situation?

Given it's an early stage company, we don't have a lot of data with which to judge Weekend Unlimited's cash burn. However, it is fair to say that its cash runway made us nervous. Overall, we're left with the impression that it may have trouble maintaining its cash burn and with uncertainty around the pay off, we'd probably try to avoid the stock. While we always like to monitor cash burn for early stage companies, qualitative factors such as the CEO pay can also shed light on the situation. Click here to see free what the Weekend Unlimited CEO is paid..

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.