Yahoo Finance

Yahoo Finance Webster Financial (WBS) Hurt by High Debt Despite Loan Growth

High debt levels, and low cash and due from banks make Webster Financial Corporation WBS vulnerable to defaulting interest and debt repayments. Moreover, the company’s capital deployment activities seem unsustainable. Also, the risk associated with a concentrated loan portfolio poses a notable concern. Nonetheless, its impressive revenue growth and healthy balance-sheet positions are tailwinds.

As of the first quarter of 2023, Webster Financial had total long-term debt of $1.07 billion, whereas cash and due from banks were $201.7 million, witnessing a volatile trend over the past few years. Additionally, the times interest earned ratio of 7 declined sequentially. Hence, we believe that the company carries a higher likelihood of defaulting interest and debt repayments if the economic situation worsens.

The sustainability of Webster Financial’s capital-deployment activities keeps us apprehensive. Although the company has a history of increasing its quarterly common stock dividend every year since 2010, the last increase was in April 2019 of 21%.

Additionally, share repurchases were suspended in 2020 due to the pandemic and in April 2021 due to the merger with Sterling Bancorp. In April 2022, Webster Financial authorized the repurchase of an additional $600 million worth of shares under its existing share repurchase program. In 2022, the company bought back shares worth $320 million. However, no outstanding shares were repurchased in the first quarter of 2023, and the company expects minimal share buyback activity in the second quarter as well.

The loan portfolio of Webster Financial mostly comprises commercial and commercial real estate loans (81% as of Mar 31, 2023). Such high exposure can be risky for the company if, besides the competitive market, the economy presents unprecedented challenges.

Further, the company's debt/equity ratio stands at 1.20 compared with the industry average of 0.34. This reflects that it has a higher debt burden relative to its peers and will unlikely be able to fare well in a dynamic business environment.

Additionally, analysts seem to be bearish on the company’s prospects. Over the past month, the Zacks Consensus Estimate for earnings has been revised 1.6% and 1.2% lower for 2023 and 2024, respectively. WBS currently carries a Zacks Rank #4 (Sell).

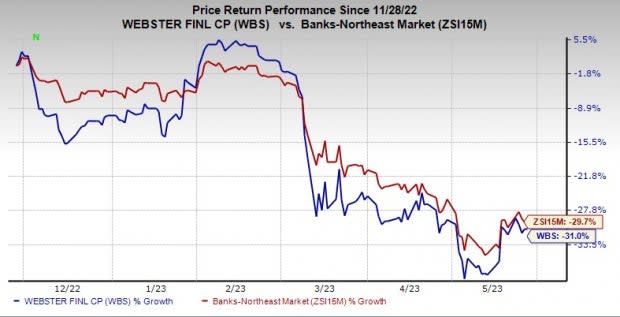

Shares of the company have lost 31% in the past six months compared with the industry’s decline of 29.7%.

Image Source: Zacks Investment Research

Nonetheless, Webster Financial’s deposits and loans recorded a three-year (2020-2022) compound annual growth rate of 40.6% and 52%, respectively, and the rising trend continued in the first quarter of 2023. Also, total quarterly revenues were $990 million, up 41.4% year over year. Hence, with high rates and robust loan growth in the upcoming quarter, the company is expected to witness revenue growth in the upcoming quarters as well.

Banks Worth a Look

A couple of better-ranked stocks from the banking space are Mitsubishi UFJ Financial Group, Inc. MUFG and Pathward Financial Inc. CASH, each currently carrying a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Earnings estimates for MUFG have been revised 1.3% upward for fiscal 2023 over the past 60 days. The company’s shares have gained 21.6% over the past six months.

The consensus estimate for CASH’s fiscal 2023 earnings has been revised 1.8% upward over the past 30 days. Over the past six months, the company’s share price has increased 6.1%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Webster Financial Corporation (WBS) : Free Stock Analysis Report

Pathward Financial, Inc. (CASH) : Free Stock Analysis Report

Mitsubishi UFJ Financial Group, Inc. (MUFG) : Free Stock Analysis Report