Yahoo Finance

Yahoo Finance Understanding Spiking VIX ETFs

Fear levels are rising on Wall Street, prompting exchange-traded products tied to the Cboe Volatility Index (VIX) to spike in October.

In the month-to-date period ending Oct. 29, the S&P 500 plummeted 9.3%, pushing the VIX to around 25, the loftiest level since April. In turn, the $1.1 billion iPath S&P 500 VIX Short-Term Futures ETN (VXX), the largest volatility ETP on the market, surged more than 50%.

VXX isn’t the only ETP tied to the VIX that is soaring this month. The $817 million VelocityShares Daily 2x VIX Short-Term ETN (TVIX) more than doubled, returning 113.5% in the month-to-date period.

(Note: VXX will expire in January 2019 and will be replaced by the iPath Series B S&P 500 VIX Short Term Futures ETN (VXXB).

What Is The VIX?

The VIX measures implied volatility, a figure based on the price of near-term S&P 500 Index options. When stocks gyrate wildly, options contracts, which allow investors to buy or sell at predetermined prices, tend to cost more.

The VIX usually rises when stocks fall, and vice versa. That’s why it has a reputation as Wall Street’s “fear gauge.”

In addition to being a thermometer of investor sentiment, the VIX is used by investors and traders as a tool for hedging and speculation. There are no products that precisely track movements in the VIX itself (spot VIX) because the portfolio of options that the index tracks is constantly changing.

Cboe Volatility Index (VIX)

VIX Futures

While the VIX itself is uninvestable, VIX futures contracts that allow traders to bet on what value the index will be at some date in the future are readily available.

Cboe Global Markets, parent company of ETF.com, lists a number of weekly and monthly VIX futures contracts whose values fluctuate based on where traders believe the level of the VIX will be at the contract’s expiration date.

The value of VIX futures tends to converge with spot VIX as a contract’s expiration nears, though they can deviate significantly from spot for contracts where expiration is far in the future.

VIX ETPs

The aforementioned VXX and TVIX are both products that have packaged VIX futures into ETPs that can be bought and sold in a standard brokerage account.

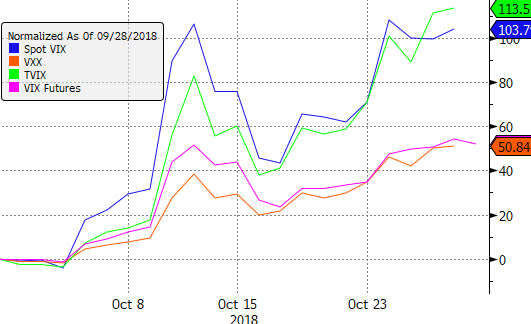

These ETPs track VIX futures closely. As of this writing, front-month VIX futures had risen 53.1% month-to-date, compared with the 50.8% return for VXX.

Meanwhile, spot VIX rose 103.8% in the same period, much greater than the jump in VIX futures or VXX—but in line with the 113.5% return for TVIX, which provides two times the return of VIX futures.

MTD Performance Through Oct. 29

Roll Costs

Anyone who delves into the world of VIX ETPs should know that these are short-term tactical tools, not buy-and-hold investments.

That’s largely because of contango, a situation when near-month futures contracts trade at a discount to later-month futures contracts. When VIX ETPs roll their positions from one futures contract to the next, they often have to sell at a lower price and buy at a higher price, resulting in a roll cost that adds up over time.

Long term, the losses can be dramatic. A $10,000 investment in VXX more than nine years ago when it first launched would be worth less than $4 today.

VXX Return Since Inception

t

When the spot VIX is low, VIX futures typically cost more along the futures curve (contango). When spot VIX is high—like now—futures tend to cost less along the curve, as traders anticipate an eventual reversion to the mean (the VIX has averaged 19.4 since its inception).

Because markets are usually stable or rising, VIX futures tend to trade in contango most of the time, which explains the dismal long-term performance of VIX ETPs.

More Than A Dozen Options

VXX is one of more than a dozen exchange-traded volatility products on the market. There are others offering nearly the same exposure, like the $148 million ProShares VIX Short-Term Futures ETF (VIXY) or the $146 million iPath Series B S&P 500 VIX Short-Term Futures ETN (VXXB)—the latter of which is the replacement for the expiring VXX.

Then there are products that add leverage to the mix. The aforementioned TVIX and the $421 million ProShares Ultra VIX Short-Term Futures ETF (UVXY) offer 2x and 1.5x leveraged exposure, respectively, to VIX futures with a weighted average maturity of one month.

Additionally, there are ETPs that offer inverse exposure to VIX futures. One of those products, the VelocityShares Daily Inverse VIX Short-Term ETN (XIV), famously shut down earlier this year after the VIX had its largest one-day increase in history in February.

But a few competing inverse VIX products, like the $348 million ProShares Short VIX Short-Term Futures ETF (SVXY), lived to a fight another day. Like the now-defunct XIV, SVXY lost more than 80% of its value in a single day on Feb. 6.

Though SVXY acted as it was designed to do, its issuer modified the product so it now offers only -0.5x exposure to the VIX as opposed to -1x before the change. Returns for SVXY should be much less volatile than they were before the adjustment.

YTD Returns For SVXY

Tools For Sophisticated Investors

VIX ETPs aren't for everyone. They're certainly good products for speculators who can stomach the huge swings in the underlying VIX futures. Both short and long VIX products can be lucrative for anyone who can time the movements in the VIX accurately.

Anyone smart or brave enough to buy an outright position in VXX or TVIX at the start of the month has made out like a bandit.

At the same time, even though the evidence is clear that VIX ETPs aren’t fit to be buy-and-hold products, they can still serve as good tools for sophisticated investors and traders. Anyone who wants exposure to stock market volatility, whether it be for hedging, a pair trade or what have you, VIX ETPs can serve that role.

Some of these products, like VXX, are among the most liquid exchange-traded products in the entire market. They are extensively used and do exactly what they are designed to do. Investors just need to clearly understand how they work before using them.

Email Sumit Roy at sroy@etf.com or follow him on Twitter sumitroy2

Research All ETFs Related to This Story