Yahoo Finance

Yahoo Finance Is Truist Financial (TFC) Worth a Watch on 6.3% Dividend Yield?

Amid the ongoing regional banking crisis and probable recession in the near term, investors must keep an eye on high dividend-yielding stocks. One such stock is Truist Financial TFC.

This Charlotte, NC-based bank offers a range of consumer banking and wealth services through retail community banking, national consumer finance and payments, wealth, mortgage banking and dealer retail services.

Truist Financial has been increasing its quarterly dividend on a regular basis, with the last hike of 8.3% to 52 cents per share announced in July 2022. Over the past five years, the company increased the dividend four times, with an annualized dividend growth rate of 5.98%.

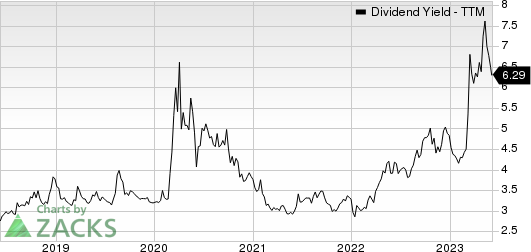

Considering the last day’s closing price of $33.05, Truist Financial’s dividend yield currently stands at 6.29%. This is impressive compared with the industry average of 4.40% and attractive for income investors as it represents a steady income stream.

Truist Financial Corporation Dividend Yield (TTM)

Truist Financial Corporation dividend-yield-ttm | Truist Financial Corporation Quote

Should you keep an eye on Truist Financial’s stock to earn a high dividend yield? Let’s check out the company fundamentals to understand risk and rewards. This will help us make a proper investment decision.

Truist Financial has been repurchasing its common stock periodically. It anticipates continuing share repurchases at regular intervals going forward. In July 2022, it authorized the buyback of up to an aggregate of $4.1 billion of its common stock through Sep 30, 2023.

TFC has recorded a constant rise in revenues. Its total revenues witnessed a compound annual growth rate (CAGR) of 22.4% over the last three years (2019-2022). The upward momentum continued in the first quarter of 2023. Our estimate for the same suggests a CAGR of 3.8%. Management expects adjusted revenues to rise 5-7% this year.

The company has been focusing on its net loans and leases as well. The metric has witnessed a CAGR of 2% over the last three years (ended 2022). Though management expects loan growth to be moderate in the near term on the economic slowdown, our estimates for total loans suggest a CAGR of 5.2% over the next three years.

Additionally, Truist Financial is expected to keep benefiting from higher rates. With the Federal Reserve expected to keep the rates higher in the near term to control inflation, the company’s net interest margin (NIM) will likely improve further. However, the pace of expansion is likely to slow down somewhat as funding costs rise. We project NIM to be 3.07%, 2.80% and 2.95% in 2023, 2024 and 2025, respectively.

Truist Financial remains focused on the growth of non-interest revenue sources. While the metric declined in 2022, the same witnessed a four-year (2019-2022) CAGR of 18.4%. The trend continued in the first quarter of 2023. We expect non-interest revenues to rise 1.8% this year.

Management is open to strategic business restructuring initiatives to further improve fee income growth. In sync with this, the company divested a 20% stake in its subsidiary — Truist Insurance Holdings — for $1.95 billion. Additionally, the bank has acquired BankDirect Capital Finance, BenefitMall, Kensington Vanguard National Land Services and Constellation Affiliated Partners in the past few years. These initiatives are likely to bolster its insurance business.

Hence, despite near-term headwinds like rising expenses and worsening asset quality, TFC stock is fundamentally solid. So far this year, shares of TFC have declined 23.2% compared with the industry’s fall of 8%.

Image Source: Zacks Investment Research

Therefore, income investors should keep this Zacks Rank #3 (Hold) stock on their radar as it will help generate robust returns over time.

Other Bank Stocks Worth a Look

A couple of other bank stocks, such as Associated Banc-Corp ASB and Huntington Bancshares HBAN, are worth a look as these have robust dividend yields.

Considering the last day’s closing price, Associated Banc-Corp’s dividend yield currently stands at 5.08%. ASB carries a Zacks Rank of 3. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Based on the last day’s closing price, Huntington Bancshares’ dividend yield currently stands at 5.50%. HBAN also carries a Zacks Rank of 3.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Huntington Bancshares Incorporated (HBAN) : Free Stock Analysis Report

Associated Banc-Corp (ASB) : Free Stock Analysis Report

Truist Financial Corporation (TFC) : Free Stock Analysis Report