Yahoo Finance

Yahoo Finance Save cash and reward shareholders: The case for stock dividends

Dividends. To cut, or not to cut. That is the question confronting companies throughout the globe as they struggle to conserve enough cash to keep themselves going during a deepening economic downturn.

Many household names-- Marriott, Ford, Boeing--have already eliminated dividends. Total cuts this year are estimated to be as high as $493 billion worldwide, representing a one-third drop from last year’s payouts. This is in stock owners’ long-term interests as dividend cuts will preserve scarce cash necessary to keep their companies afloat and operational. Importantly, most families will feel none of the pain as about half have any exposure to the stock market, and wealthy investors can presumably weather several quarters of skipped dividends.

Read more: What are stocks and how do they work?

Yet there are retirees and other middle class families who do depend on those dividend checks to cover living expenses. For them, dividend cuts can create hardship, so it is worth asking whether there is an alternative.

Paying dividends in shares, instead of cash, is one way to address the needs of this group.

When a company declares a stock dividend, shares are awarded as a percentage of total share ownership. For instance, a 5% stock dividend would result in an award of 50 shares to a shareholder with 1,000 shares. There are two key benefits to stock dividends: they do not drain precious cash from the company, and they give shareholders optionality. Shareholders can keep the shares, along with any upside potential, or they can sell the shares in the secondary market if they need cash. Share dividends also have tax advantages. In general, while taxes are due on cash dividends, they only apply to share dividends if and when the shares are sold.

The disadvantage of share dividends is dilution. It increases the number of shares outstanding so all other things being equal, the stock price will fall. However, the overall value of the company will remain the same, and stock holders themselves are not diluted. Their proportionate ownership of the company is unaffected.

To be sure, dilution is an issue for corporate executives whose variable compensation may be reduced with a drop in earnings per share (EPS), though that is hardly a reason to deny shareholders the benefit of a stock dividend. Over the past several years, many corporate executives saw their pay skyrocket from increased EPS, driven not by value creation, but simple math. Their companies issued debt, used the proceeds to buy back shares, and increased EPS simply by shrinking the number of shares outstanding. Many of those executives now have egg on their faces as their shares trade at significant discounts to the prices they paid when executing buybacks. In a sense, stock dividends can be seen as the anti-buyback, returning stock to shareholders who stuck with the company, even when it was repurchasing shares at rosy valuations.

The other argument against stock dividends is that companies should not be issuing stock when shares are undervalued. This argument might makes sense if the shares were being issued to new investors, to the detriment of current holders. But they are being awarded only to investors who already own the company’s stock. The entire benefit- including the potential that the dividends shares will substantially appreciate once the crisis passes– will appeal to them.

Moreover, given the complete disconnect between the stock market and real economy right now, it is far from clear that valuations are low. Indeed, a recent analysis shows that Monday’s stock market rally has brought prospective price/earnings multiples to highs not seen since December 2000 in the midst of the tech bubble. We can all thank the Fed for keeping corporate America propped up for now, but that can only last for so long. By the end of the year, it is possible that we will look back at stock prices and realize they were, in fact, unjustifiably high.

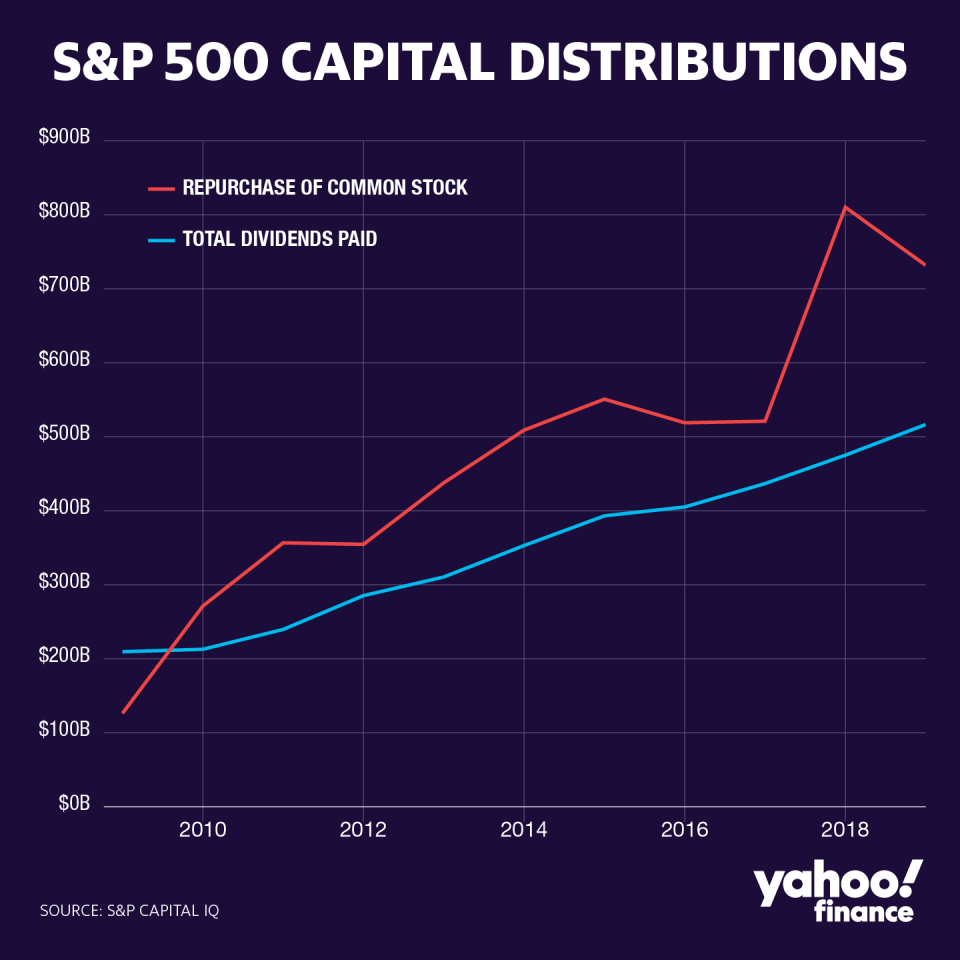

Over the past 10 years, buybacks by S&P 500 companies have grown from $126 billion in 2009 to $732 billion last year. Over the same period, dividends grew from $210 billion to $516 billion.

These represent trillions of dollars that were not reinvested in companies to grow and innovate, to create more good-paying jobs, and to better meet customer needs. Some of the best performing companies in history have never paid dividends (think Amazon, Berkshire Hathaway), preferring instead to invest more in their businesses while keeping cash on hand for a rainy day, the best time to make strategic acquisitions. To be sure, there is a place for cash dividend stocks and a limited role for buybacks. But once we get past this crisis, investors and corporate leaders should rethink shareholder payout levels, and hopefully make these outsized cash drains a thing of the past.

For now, this terrible pandemic is forcing tough choices by both businesses and households. With regard to dividend cuts, there are no perfect answers. The most important thing is for hard-hit companies to suspend dividends and deploy their cash into payroll and operations. Keeping them afloat at some level is our economy’s best hope for making a quick comeback. Banks in particular, as I have previously written, should stop all cash shareholder payouts until this crisis passes, so that they can remain solvent and continue to lend.

For them and other companies who can no longer afford a cash dividend, the question then becomes which option is of greater benefit to shareholders: a stock with no dividend or one that pays dividends in stock?

-

Sheila Bair is the former Chair of the FDIC and has held senior appointments in both Republican and Democrat Administrations. She currently serves as a board member or advisor to several companies and is a founding board member of the Volcker Alliance, a nonprofit established to rebuild trust in government.

Read more:

The mystery behind the Fed’s refusal to suspend bank dividends

Why student loan forgiveness should target graduates who need it the most

The $1.4 trillion student loan market faces a huge issue — transparency

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.