Yahoo Finance

Yahoo Finance Is ServiceSource International (NASDAQ:SREV) A Risky Investment?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that ServiceSource International, Inc. (NASDAQ:SREV) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for ServiceSource International

What Is ServiceSource International's Net Debt?

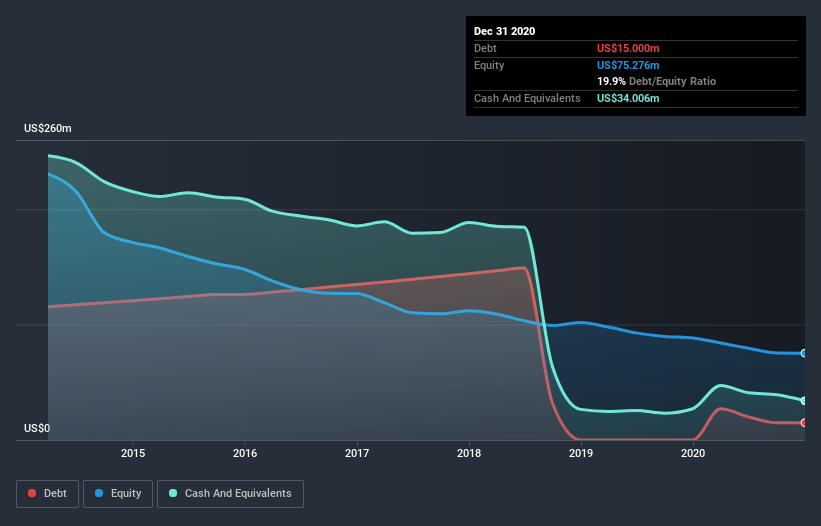

You can click the graphic below for the historical numbers, but it shows that as of December 2020 ServiceSource International had US$15.0m of debt, an increase on none, over one year. However, its balance sheet shows it holds US$34.0m in cash, so it actually has US$19.0m net cash.

How Strong Is ServiceSource International's Balance Sheet?

We can see from the most recent balance sheet that ServiceSource International had liabilities of US$49.8m falling due within a year, and liabilities of US$27.6m due beyond that. Offsetting these obligations, it had cash of US$34.0m as well as receivables valued at US$38.9m due within 12 months. So it has liabilities totalling US$4.44m more than its cash and near-term receivables, combined.

Since publicly traded ServiceSource International shares are worth a total of US$152.6m, it seems unlikely that this level of liabilities would be a major threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, ServiceSource International also has more cash than debt, so we're pretty confident it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But it is ServiceSource International's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year ServiceSource International had a loss before interest and tax, and actually shrunk its revenue by 9.9%, to US$195m. That's not what we would hope to see.

So How Risky Is ServiceSource International?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that ServiceSource International had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through US$7.5m of cash and made a loss of US$19m. But the saving grace is the US$19.0m on the balance sheet. That means it could keep spending at its current rate for more than two years. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 1 warning sign for ServiceSource International that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.