Yahoo Finance

Yahoo Finance Is Renaissance Oil (CVE:ROE) Weighed On By Its Debt Load?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Renaissance Oil Corp. (CVE:ROE) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Renaissance Oil

What Is Renaissance Oil's Debt?

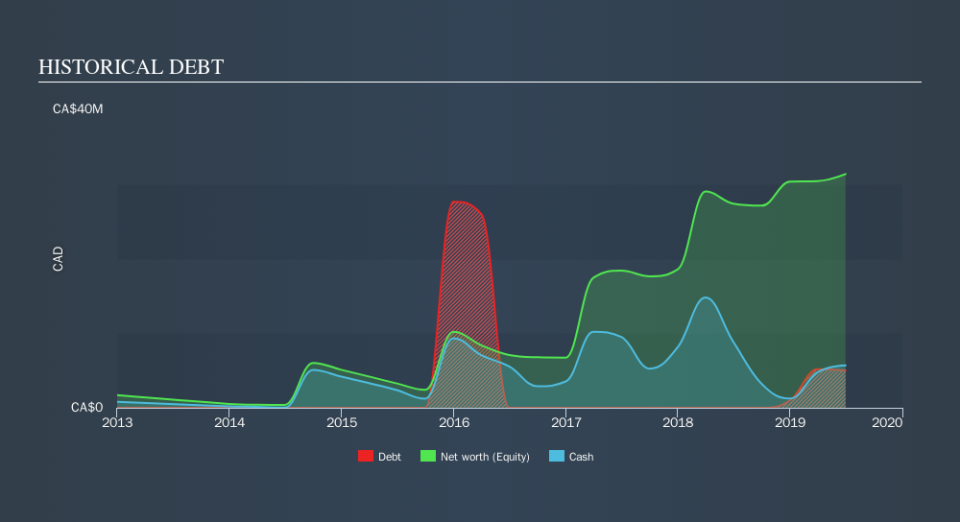

As you can see below, at the end of June 2019, Renaissance Oil had CA$4.98m of debt, up from none a year ago. Click the image for more detail. But on the other hand it also has CA$5.68m in cash, leading to a CA$701.5k net cash position.

A Look At Renaissance Oil's Liabilities

Zooming in on the latest balance sheet data, we can see that Renaissance Oil had liabilities of CA$4.20m due within 12 months and liabilities of CA$5.04m due beyond that. Offsetting these obligations, it had cash of CA$5.68m as well as receivables valued at CA$2.41m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CA$1.15m.

Since publicly traded Renaissance Oil shares are worth a total of CA$43.9m, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, Renaissance Oil also has more cash than debt, so we're pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Renaissance Oil can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Renaissance Oil saw its revenue drop to CA$4.1m, which is a fall of 18%. That's not what we would hope to see.

So How Risky Is Renaissance Oil?

Although Renaissance Oil had negative earnings before interest and tax (EBIT) over the last twelve months, it made a statutory profit of CA$915k. So when you consider it has net cash, along with the statutory profit, the stock probably isn't as risky as it might seem, at least in the short term. With revenue growth uninspiring, we'd really need to see some positive EBIT before mustering much enthusiasm for this business. For riskier companies like Renaissance Oil I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.