Yahoo Finance

Yahoo Finance Is Power Corporation of Canada (TSE:POW) Overpaying Its CEO?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Paul Desmarais became the CEO of Power Corporation of Canada (TSE:POW) in 1996. First, this article will compare CEO compensation with compensation at other large companies. After that, we will consider the growth in the business. And finally - as a second measure of performance - we will look at the returns shareholders have received over the last few years. This process should give us an idea about how appropriately the CEO is paid.

See our latest analysis for Power of Canada

How Does Paul Desmarais's Compensation Compare With Similar Sized Companies?

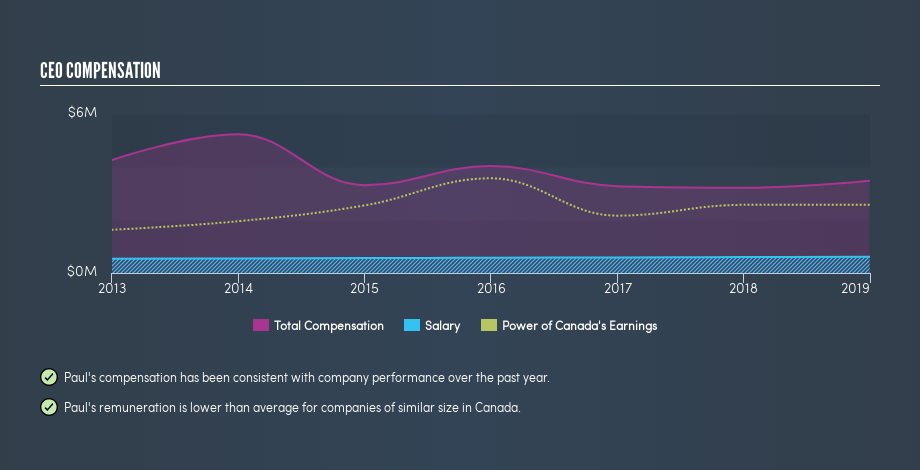

Our data indicates that Power Corporation of Canada is worth CA$13b, and total annual CEO compensation is CA$3.5m. (This number is for the twelve months until December 2018). That's a notable increase of 8.3% on last year. While this analysis focuses on total compensation, it's worth noting the salary is lower, valued at CA$613k. We looked at a group of companies with market capitalizations over CA$11b and the median CEO total compensation was CA$8.8m. (We took a wide range because the CEOs of massive companies tend to be paid similar amounts - even though some are quite a bit bigger than others).

Most shareholders would consider it a positive that Paul Desmarais takes less in total compensation than the CEOs of most other large companies, leaving more for shareholders. Though positive, it's important we delve into the performance of the actual business.

You can see a visual representation of the CEO compensation at Power of Canada, below.

Is Power Corporation of Canada Growing?

Earnings per share at Power Corporation of Canada are much the same as they were three years ago, albeit slightly lower, based on the trend. Its revenue is down -6.4% over last year.

Unfortunately there is a complete lack of earnings per share improvement, over three years. And the impression is worse when you consider revenue is down year-on-year. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Shareholders might be interested in this free visualization of analyst forecasts.

Has Power Corporation of Canada Been A Good Investment?

With a total shareholder return of 21% over three years, Power Corporation of Canada shareholders would, in general, be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

Power Corporation of Canada is currently paying its CEO below what is normal for large companies.

The compensation paid to Paul Desmarais is lower than is usual at larger companies. However, the earnings per share are not moving in the right direction, and the returns to shareholders could have been better. We would like to see EPS growth from the business, although we wouldn't say the CEO pay is high. So you may want to check if insiders are buying Power of Canada shares with their own money (free access).

Important note: Power of Canada may not be the best stock to buy. You might find something better in this list of interesting companies with high ROE and low debt.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.