Yahoo Finance

Yahoo Finance Pembina Pipeline Completes Mega-Projects and Acquistion in Q3. Now What?

The third quarter of 2017 was a memorable quarter for pipeline company Pembina Pipeline (NYSE: PBA). Back in 2013, management put together a monstrous spending plan that would make most companies the size of Pembina blush, but the company is on the precipice of completing that ambitious plan. The company may not show much change in its earnings for the quarter, but it will soon.

Let's review Pembina's most recent quarter, what the company accomplished with this growth plan, and where the company can go from here.

Image source: Getty Images.

By the numbers

Metric | Q3 2017 | Q2 2017 | Q3 2016 |

Revenue | CA$1.05 billion | CA$1.17 billion | CA$970 million |

Operating margin | CA$403 million | CA$355 million | CA$317 million |

Net income | CA$107 million | CA$124 million | CA$120 million |

EPS | CA$0.22 | CA$0.26 | CA$0.25 |

Source: Pembina Pipeline earnings release. EPS= earnings per share.

The third quarter and the days leading up to Pembina's third-quarter earnings release were the finishing touches on the company's incredible five-year transformation into one of North America's largest pipeline and processing companies. Ever since the end of June, the company has brought CA$4.4 billion worth of assets into service as well as closed its deal to purchase midstream company Veresen for CA$9.7 billion.

The reason Pembina's earnings don't look that much different from the prior quarter despite all of these new assets is either its more significant projects are still ramping up to full capacity, or that they were brought into service after the quarter ended. The Veresen deal closed just after the end of the quarter, but management did note that Veresen produced CA$164 million in EBITDA for the third quarter.

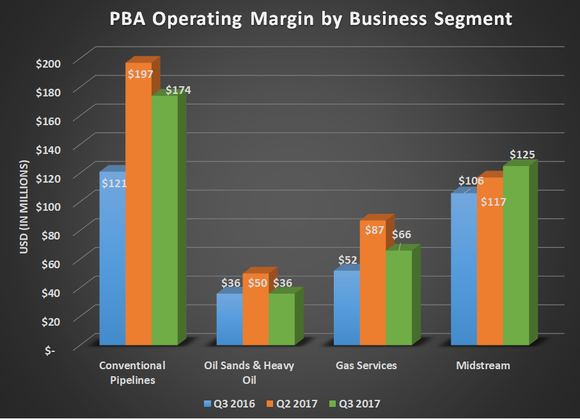

Source: Pembina Pipeline earnings release. Chart by author.

When it comes to announcing new projects, though, the company was much quieter than it has been recently. It expanded the scope of its phase V conventional pipeline expansion project by CA$135 million, and after releasing quarterly results, it announced a CA$290 million infrastructure project in the Durvernay shale region. The Duvernay development is part of a 20-year development agreement with Chevron where Pembina will be the exclusive infrastructure provider to Chevron's Kaybob shale acreage.

What management had to say

The third quarter was a bit of a victory lap for CEO Mick Dilger and his team for actually pulling off this incredibly ambitious growth plan over the past several years. According to Dilger's press release statement, the company is now formulating plans for the next wave of growth.

On Oct. 2, 2017, we closed the acquisition of Veresen -- marking a transformational moment for our company. With increased size and scale, greater diversification and a broader service offering, the future is bright for Pembina. Going forward, we are capable of pursuing expanded growth opportunities in support of continued value creation for our shareholders. Given the strong financial position of the combined company, we were also proud to have increased the dividend for a second time this year.

Looking ahead, we will stay focused on successfully completing the remaining growth portfolio, further progressing our large-scale potential project roster as well as working to integrate Veresen and to achieve the near-term expected synergies of $75 to $100 million on a run-rate basis. We are now positioned as a leading North American infrastructure company able to continue delivering top-tier performance and I am excited to realize our expected transformational results.

What a Fool believes

Pembina's management has done a commendable job of integrating this massive growth plan and making a multi-billion dollar acquisition without completely blowing up its balance sheet. When combined with Veresen, the company will still have a debt to EBITDA ratio of four times, an investment grade credit rating, and more than 86% of its revenue coming from fee-based contracts. That's the kind of conservative metrics you want in a high yield midstream company.

The next question for Pembina is this: What now? With all of these projects currently in service, the company has less than CA$2 billion in projects actively under construction. So the thing that investors should be watching for is new project announcements soon. Management has already given the green light for its CA$2 billion petrochemical manufacturing facility, but it now has the Jordan Cove LNG export terminal as a potential asset and about CA$20 billion in unsecured projects for beyond 2018. It may mean slightly slower dividend growth for 2018 and 2019, but Pembina looks well positioned to deliver prodigious returns for investors.

More From The Motley Fool

6 Years Later, 6 Charts That Show How Far Apple, Inc. Has Come Since Steve Jobs' Passing

Why You're Smart to Buy Shopify Inc. (US) -- Despite Citron's Report

Tyler Crowe has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.